Australian Housing: Bubble or Not?

The debate is well and truly on over whether Australian housing is getting bubbly. The media sees its job as to create a conflict so those trying to form a view from reading general commentary could be left thinking that everyone is either a full bubble proponent (see LF Economics, Roger Montgomery or Zero Hedge) or of the balanced market view (see your local real estate agent or property developer). Out of all this I found two graphs very helpful – one that aligns with either side of the debate. Both graphs go back to basic demand and supply mechanics.

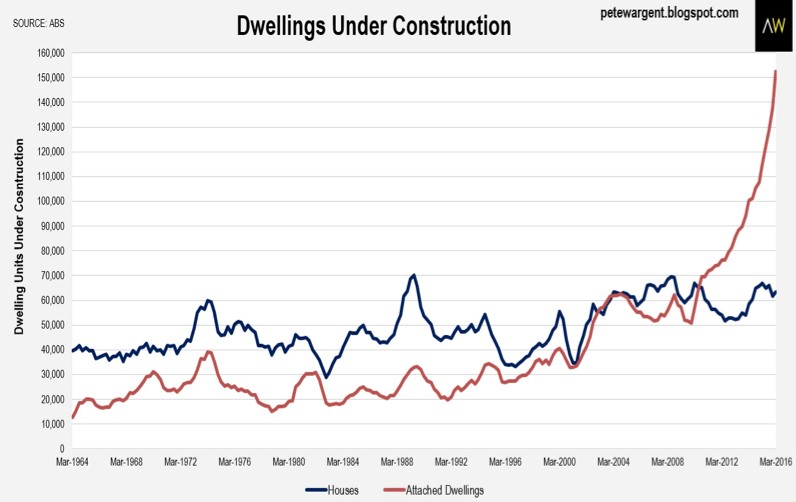

Firstly the bear case, which focuses on a looming oversupply of housing. Morgan Stanley says that there might be an oversupply of 100,000 units in the next two years, others think it is far more. The graph below from Pete Wargent shows that the number of units under construction has shot up in the last two years. This should remain elevated for some time yet as there is a record number of cranes at work with 81% used for residential projects. The most recent update of the RLB crane index had Sydney still increasing, with falls in Melbourne and Brisbane.

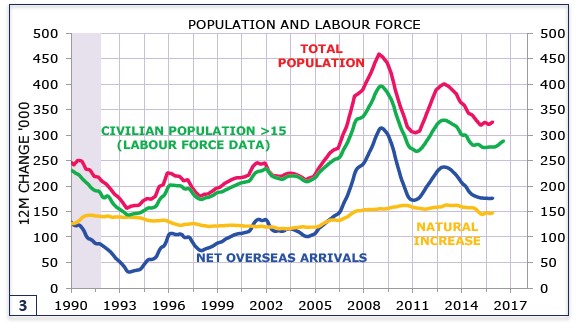

Now the bullish case, which focuses on the demand for housing. The graph below shows Australian population growth remains high with both natural growth (births minus deaths) and migration well above levels seen in other developed economies. To give the numbers some context, Germany took 1.1 million migrants last year. This boosted their population by about the same percentage that Australia has for each of the last ten years. Demand for Australian housing has generally seen rent rise faster than inflation, with vacancy rates still low in most capital cities.

Source: Minack Advisors

The basic demand and supply factors say that Australia has underbuilt over the last decade but now looks to be overbuilding. Before anyone gets too bearish though, the new supply is skewed towards studio and one bedroom apartments which obviously won’t accommodate as many people as new houses. What that means is if construction slows dramatically for two or three years population growth might absorb excess capacity. There will be bumps for some apartment types and some locations, which will spill over somewhat to all housing, but it doesn’t look the same as the widespread overcapacity that US subprime lending helped create. Perhaps more of a UK style post-crisis pullback could playout where outright falls of around 10% are seen, with inflation adjusted prices down around 20%.

The caveat to this view is that Australia hasn’t had a recession for 25 years, dulling the general populations sense of risk. If a recession happens, selling by people who have lost their jobs and cannot make their mortgage payments will move prices down further and faster than basic demand and supply indicators would imply. Credit is still too easily available; a UBS survey found that 28% of borrowers admitted to fudging their home loan applications. The example of a 28-year-old pizza store manager who owns 13 properties shows that banks are all too willing to lend more against the “equity” created by rising property prices. The surge in what are effectively second mortgages from “the bank of mum and dad” shows how stretched many first time buyers are. Interest rates can’t fall much further so there’s limited potential offset there.

Turning to the policy side of this debate there’s two things that stand out. Firstly, governments bear almost all of the blame for housing being unaffordable. Federal taxes benefit housing over other investment sectors, notably high income tax rates combined with negative gearing and capital gains tax exemptions. State governments are earning enormous amounts from stamp duty, when land tax is a much better way to raise revenue. The recent ACT election result showed that an appropriately implemented land tax isn’t a government killer. Local governments control zoning restrictions, many are ignoring the need to increase density particularly near public transport hotspots.

The second policy area is migration. The huge population growth of the last ten years has created enormous strains on housing, transport and government services, particularly in Sydney and Melbourne. The winners from this growth are developers, construction companies and big businesses, who all see higher demand for their services. Existing land owners have received windfall gains. The losers are average citizens who see their quality of life decrease and cost of living increase.

I think the there’s votes available for the first major party that calls out the impact of migration and argues that improving quality of life takes priority over top line GDP growth. The argument needs to be clear that it is not about where migrants come from; it is that there’s simply too much population growth to be accommodated. I won’t hold my breath on that, politicians are disproportionate owners of property and are unlikely to want to reduce a major factor that increases their wealth.

Written by Jonathan Rochford for Narrow Road Capital on November 1, 2016. Comments and criticisms are welcomed and can be sent to info@narrowroadcapital.com

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

4 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment