Just how did BHP get it so wrong?

Sam Dyson

Vertium Asset Management

Mining 101: a good mining company makes money at the low end of a steep cost-curve. This is BHP’s strategy and it is working wonders in iron ore. However, in 2011 BHP forgot this simple rule. Deal hungry and with cash flow burning a hole in the pocket after two failed takeovers, BHP spent US$38 billion on US shale oil. Today, it’s trying to sell the shale for far less. Just how did BHP get it so wrong?

The shale revolution

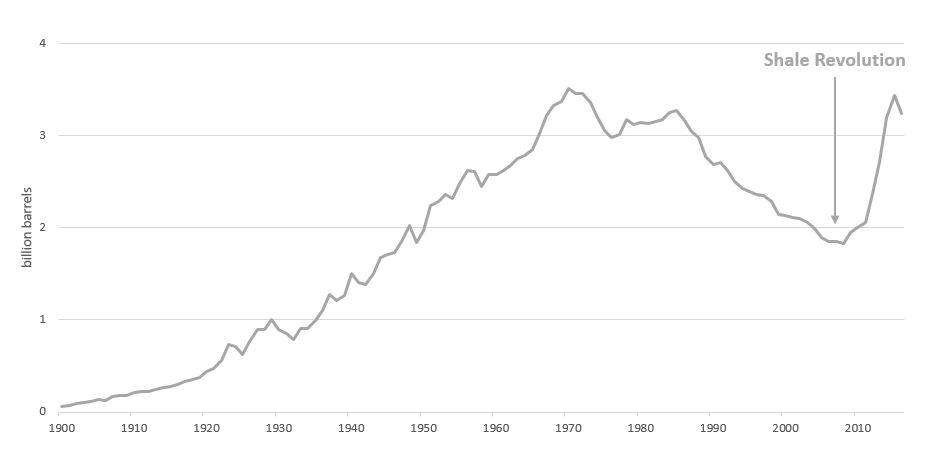

Shale oil and gas has been produced for over a century, but the recent boom dates back to 1998 with the use of ‘fracking’ – pumping water down the well to fracture the oil reservoir. By 2005, a Texas land-grab and ‘shale revolution’ were underway, bringing US production back to peak levels last seen 50 years ago.

Chart 1: US oil production

Source: US Energy Information Administration

The turnaround has been so swift because shale has a fast pay-back. For a mere US$5-10 million, a shale well can be drilled and completed in less than 10 weeks. Within another couple of months, production peaks and within a few years, most of the oil has been extracted and the costs recouped.

A conventional offshore field however, involves around US$1 billion, years of risky exploration and, once discovered, another seven to 10 years to develop and that again to extract. You need a hundred or more shale wells each year to match the production of a conventional field, but each well is a much lower-risk investment.

For BHP, the real attraction of shale is its reserves. BHP’s existing oil business sits awkwardly within the group because it has a reserves problem. At the 2010 rate of production, BHP’s oil reserves would be fully depleted within only nine years versus an average 25-35 years for its other divisions. But, unlike conventional oil, shale is more of a mining business. Large deposits are relatively easy to find, and with scale and a technology ‘learning curve’, it can be extracted at a low enough unit cost. The vast known shale resources are deemed economically viable and thus can be booked as reserves.

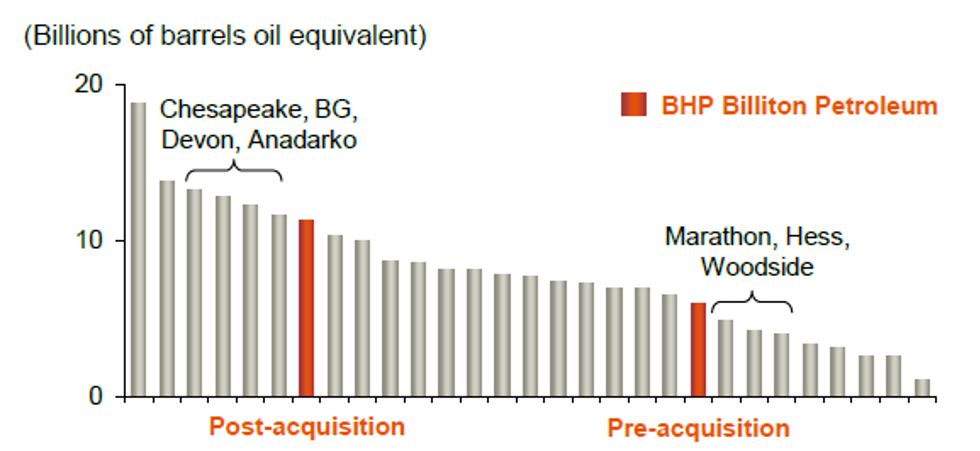

So, in early 2011, BHP paid US$4.75 billion for the Fayetteville Shale, instantly increasing petroleum reserves by 30%. That was closely followed by the takeover of PetroHawk, adding another 40% to reserves. This was a listed company widely considered ‘dressed up for sale’ given the CEO’s history of selling to larger oil companies. BHP paid a whopping US$15.1 billion, a knock-out bid that was 65% above the prevailing share price!

Despite the big price, there was logic behind it. BHP’s risked resource base had just tripled at a cost of US$2.3 per barrel compared to US$3.4 per barrel for its existing business. And BHP was now a big player.

Chart 2: BHP is the 7th biggest independent oil and gas company by resources

Source: BHP Billiton, November 2011

Big hat, no cattle

There was just one problem: shale has never made a positive return. The gas and liquids are real, but the profits, and thus the reserves, are conjecture.

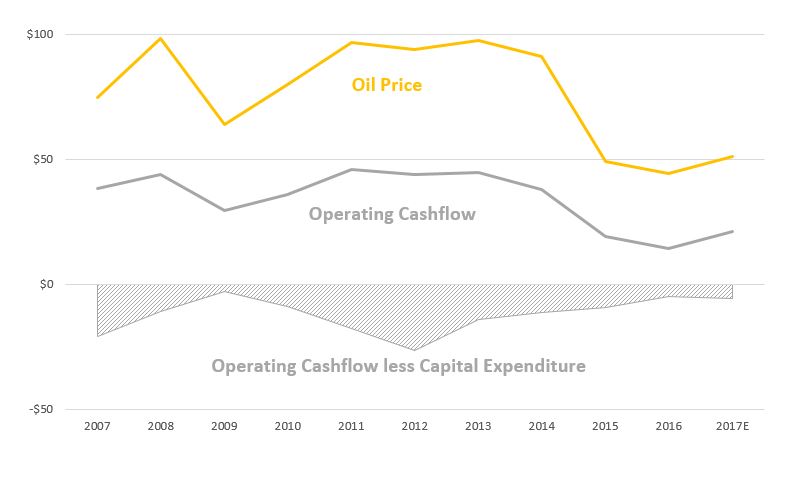

We can look at the 36 largest pure shale companies still listed in the US, ignoring the scores of bankruptcies since the oil price collapse of 2014. Over the past 10 years, they earned an aggregate US$296 billion of operating cash-flow, but they spent US$403 billion of capital. They have been drained of cash every single year, as seen in chart 3 which shows the average oil price, the equivalent operating cash-flow per barrel of oil produced and the cash-flow after capital expenditure.

Remarkably, at oil prices above US$100 per barrel the net cash-flow was still negative, which is still the case despite a drop in capital spend and production.

Chart 3: US shale economics per barrel produced

Source: Factset, Vertium

But, how can this be?

The economics of shale are so promising, yet the shale industry is so uneconomic.

1. Shale is lower ‘grade’

While shale typically has lower unit costs than conventional oil, it also has a lower price. This is because oil wells are a mix of oil, natural gas liquids and gas, and the mix from shale is typically unfavourable (higher in gas, lower in liquids). For example, in FY15 and FY16, BHP focused on its liquids-rich Eagle Ford and Permian shales. Even so, it received only US$27 per barrel versus US$48 per barrel from its (conventional) Gulf of Mexico fields, resulting in EBITDA of US$11 per barrel versus US$27 per barrel from the Gulf of Mexico.

2. There is lots of marginal supply

Nevertheless, shale is still the best, lowest-risk and quickest field to develop when the oil price is high enough. It should also be the first to turn off when the oil price falls because the oil is extracted so quickly. Shale is thus the ‘marginal’ new source of supply, and there is a lot of it. Shale responds to the prevailing oil price which, like most commodities, is just enough to keep the marginal supplier alive.

3. The shale cost-curve is flat

The real reason why no company makes money from shale is because none has much of a cost advantage. The shale resource is known. The drilling technology is owned by oil services companies like Halliburton and Schlumberger, which will gladly rent it out to all and sundry. The workforce, equipment and processes have been standardised given the thousands of small wells involved. Working faster and smarter has resulted in dramatic unit cost reduction, but it has been available to all.

There is a lot of whooping and swagger about US shale and it is indeed a ‘game-changer’ in many respects. There are benefits to the US economy from improved energy self-sufficiency and large-scale job creation. The banking system extracts massive fees from large and frequent asset-backed lending transactions. State governments and land-owners receive large royalties.

For the investors though, there is no return. BHP bought the 10-gallon hat, but shareholders were duffed.

Not-so-big dividend

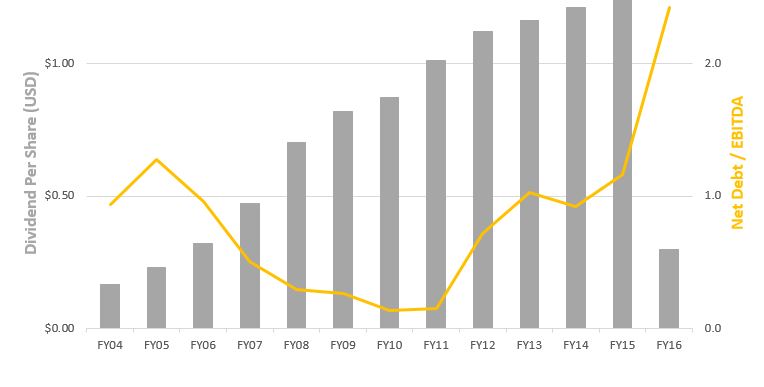

CEO, Marius Kloppers, and the Petroleum president resigned in 2013 following a US$2.8 billion impairment of the first shale acquisition. Nevertheless, the delusion continued for several years under the new CEO, Andrew Mackenzie, with shale capital expenditure rising to US$4.7 billion in FY2013 and US$4.2 billion in FY2014. To maintain low unit costs and viable reserves, BHP had to keep drilling. But then in the last half of 2014, the oil price collapsed from over US$100 to under US$55 per barrel.

The balance sheet weakened at an alarming pace. And yet, the board approved a final dividend in August 2015 of US$0.62 per share despite earning just US$0.20 per share in the six-month period. The phrase, “strong balance sheet” was penned a record number of times in the annual report that followed. Surprisingly, it took another 18 months for reality to set in: the March 2016 dividend was slashed to pre-2005 levels of US$0.16 per share. Shareholders could rightly ask, “Where did my mining boom go?”.

Chart 4: BHP’s dividend per share and balance sheet leverage

Source: Factset, Vertium

Big rethink

BHP admitted this year that the shale investment was a mistake, blaming the low oil price. No, the mistake rather was a flawed understanding of the cost-curve. A mining company should know better, especially one with ‘Think Big’ as its brand campaign. Buying at a high oil price and a big premium certainly made the mistake bigger.

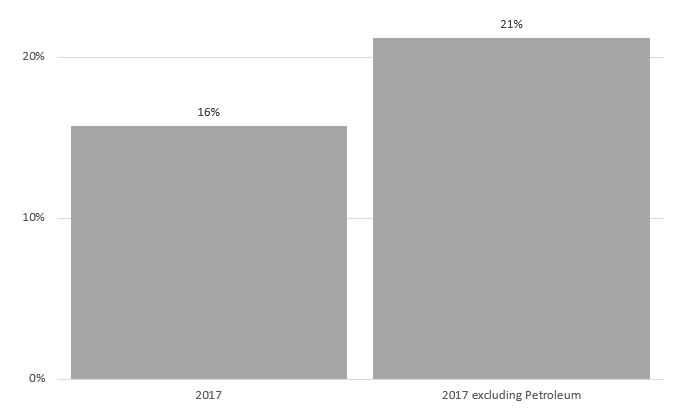

Impairments now total US$13.4 billion from a total investment in shale of US$38 billion. Since April, BHP has borne public criticism from the brash activist investor, Elliott Management, who is demanding the separation of the US petroleum division. Doing so would make sense: the 2017 return on operating assets was 16% but it would have been 21% without petroleum.

Chart 5: Pre-tax return on operating assets

Source: BHP, Vertium

BHP is now hoping to sell the shale assets. And, with Ken Mackenzie as BHP’s new chairman this is an opportunity to think better. He built his stellar reputation as CEO of Amcor by improving productivity, selling non-core assets and using acquisitions to extract capital and margin improvement. His big bets were timed impeccably: the Alcan packaging assets were bought at the trough of the GFC.

This was a crisis of BHP’s own making and it should not be wasted. Many companies that survive a stressed balance sheet tend to operate very soberly thereafter. The very best companies recognise mistakes, learn to cherish shareholder capital and forge a stronger corporate culture as a result. That process, hopefully, is now underway at BHP.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Sam joined Vertium in 2017 as a Portfolio Manager / Equity Analyst. He has over 15 years’ investment management experience across Australian equities and Asian equity markets. At Vertium, Sam assists the CIO and is responsible for researching and analysing Australian companies.

Before joining Vertium, Sam was an Investment Analyst at Cadence Capital and an Equities Analyst / Portfolio Manager at Maple-Brown Abbott where he co-managed the Maple-Brown Abbott Australian large and small-cap portfolios.

11 topics

1 stock mentioned

Sam Dyson

Vertium Asset Management

Sam joined Vertium in 2017 as a Portfolio Manager / Equity Analyst. He has over 15 years’ investment management experience across Australian equities and Asian equity markets. At Vertium, Sam assists the CIO and is responsible for researching and...

Expertise

Sam Dyson

Vertium Asset Management

Sam joined Vertium in 2017 as a Portfolio Manager / Equity Analyst. He has over 15 years’ investment management experience across Australian equities and Asian equity markets. At Vertium, Sam assists the CIO and is responsible for researching and...

Expertise

Comments

Comments

Sign In or Join Free to comment