Bonds amplify equities' losses

Today I bust a bunch of big myths relevant to the current price action: specifically, I show why bonds are, contrary to popular belief, a terrible equities hedge (the oft-mooted negative correlation is incredibly unreliable and often positive); why the popular low-rates-for-long meme is completely bogus; why you should not have interest rate risk in your portfolio despite the fact most super funds are lumbered with massive amounts of this value-destructive beta; and why BB+ high yield debt can have lower investment risk than AAA rated government bonds---it all depends on your interest rate bets (click on that link to read or AFR subs can click here)! See excerpts below:

Supposedly smart investors argue there is a long-term negative correlation between fixed-rate bonds and equities that means you should allocate to the former to protect against losses in the latter. As the experiences in February, September and October demonstrate, this presumption is totally wrong.

Equities have been smoked while the Composite Bond Index, which tracks “fixed-rate”—as opposed to “floating-rate”—bonds, has been concurrently hammered. Rather than mitigating equity losses, fixed-rate bonds amplified them, as we’ve warned was a risk for years.

Vested interests often market the mythical inverse correlation between bonds and equities with several other equally fallacious fables. The most prominent since the global financial crisis has been that interest rates will remain low forever because wage and inflation growth was dead. This rationalised allocations to stocks given that the long-term “risk-free rate”, which investors use to revalue companies’ future cash-flows back to the present, would be smaller than it has been previously, lifting prices.

The bonds-as-an-equities-hedge and faddish “low-rates-for-long” meme were also relentlessly advocated by fixed-income funds trying to convince folks to give them money at a time when government bond yields were at their lowest levels in 5,000 years, implying these assets were in the mother-of-all-bubbles. (This should be distinguished from financial credit spreads, or the risk premia above government bond yields that banks and insurers borrow at, which remain orders-of-magnitude wider today than they were in 2007.)

The much-mooted “new normal” has been devastated by the US Federal Reserve’s aggressive interest rate hikes, which should meet our forecast of 7 to 8 standard 25 basis point increases between 2017 and 2018, and the corresponding jump in the US 10 year government bond yield from 1.6 per cent in 2016 to over 3.2 per cent. This variable is crucial because it is the best proxy for the global price of money and the benchmark upon which other developed country risk-free rates, including Australia’s 10 year government bond yield, are predicated.

The driver has been the validation of our hypothesis that surprisingly strong US economic growth would push the unemployment rate below even the most sanguine projections a few years ago (the current 3.7 per cent jobless rate is a touch above our 3.5 per cent forecast for end 2018), which would in turn shunt US wages and core inflation higher.

Notwithstanding the claims of equity and bond bulls, who love to proselytize about the inflation-killing influences of technology and debt burdens, time has proven that escalating consumer prices are a much bigger worry for markets than disinflation. Annual hourly earnings have lifted from below 2 per cent towards 3 per cent while core inflation will soon breach the Fed’s 2 per cent target.

On technology and debt we counter that the Internet actually encourages winner-take-all monopolies (Amazon, Google, Seek, Facebook) that could ultimately intensify price pressures while governments have always preferred to spend and inflate their way out of their fixed nominal debts rather than tightening their belts. Who talks about “austerity” these days?

A final shibboleth is the widely-held notion—promulgated by banks and investors in residential mortgage-backed securities (RMBS)—that house prices can only fall if the unemployment rate rises That’s BS.

After hitting 6.4 per cent in 2014, Australia’s jobless rate has shrunk to 5.3 per cent (and would be below 4 per cent were it not for a record surge in job seekers). While employment has soared, house prices have slumped more than 6 per cent in Sydney and 4 per cent nationally over the last year. In April 2017 we were a lonely voice declaring the boom over and predicting a 10 per cent drop in prices on the back of higher mortgage rates even though we expected the economy to grow briskly. Following a year of price declines, ANZ, UBS, PIMCO, NAB, and others have embraced this perspective.

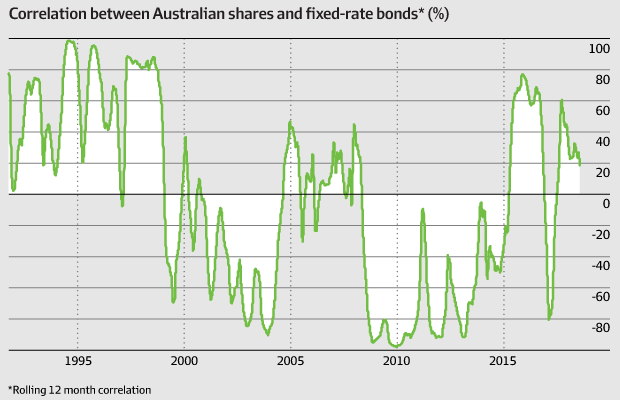

Returning to the point that it’s silly to hedge equities with bonds, we quantified the correlation in rolling 12 month returns between Australian shares and the Composite Bond Index, which tracks the performance of fixed-rate bonds, over the last 30 years (see chart). The data shows that the typical correlation between equities and bonds is, in fact, a big fat zero. More significantly, there have been periods when the correlation has been extremely positive (during the 1990s and just before the GFC) and times when it has been very negative (in the early 2000s and after the GFC). Latterly the correlation has moved back into positive territory, as we cautioned was possible in an inflationary world.

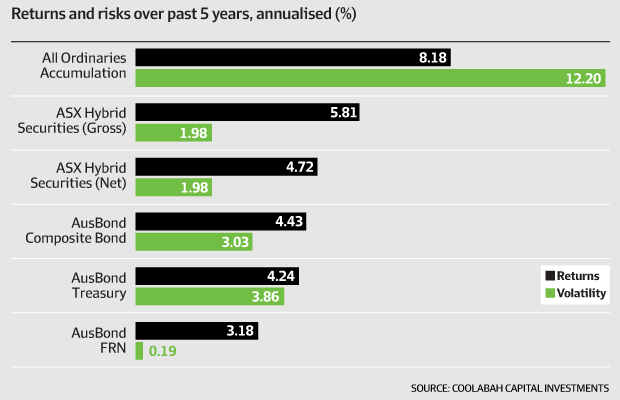

This begets another myth-buster: the belief that a bond portfolio’s credit rating is a guide to its investment risk. It is, in fact, easy to illustrate how a portfolio of BB rated ASX hybrids has materially lower investment risk than holding AAA rated government bonds on a mark-to-market basis. The table summarises the risk and returns of several asset-classes, including fixed-rate bonds (Composite Bond Index), floating-rate notes (AusBond FRN Index), AAA rated government bonds (AusBond Treasury Index), and ASX hybrids without (net) and with (gross) franking.

Over the topsy-turvy last 5 years, ASX hybrids with (without) franking have returned 4.7 per cent (5.8 per cent) annually with very low return volatility of 1.98 per cent compared to: a AA rated fixed-rate bond portfolio, which returned an inferior 4.4 per cent annually with much higher 3 per cent volatility; AA rated FRNs, which offered 3.2 per cent with only 0.19 per cent volatility; and AAA rated government bonds, which delivered 4.2 per cent with stonking 3.9 per cent volatility.

Hybrids have had lower volatility than more highly rated fixed-rate and government bonds over this period because of interest rate, rather than credit, risk. Almost all hybrids are floating-rate rather than fixed-rate. Observe how the FRN index only displayed tiny 0.19 per cent annual return volatility, which is 16 times less risky than the fixed-rate bond index with the same average AA rating.

That’s like comparing the difference between a variable-rate savings account that moves up and down with the RBA cash rate, to a 5 year term deposit, in which you’re making a huge bet on where rates are heading. If rates fall, you win big in the TD, but if they rise, you can lose badly. This is why the FRN index has appreciated 0.3 per cent since the start of September while the fixed-rate Composite Bond Index has lost 0.7 per cent.

Government bonds are fixed-rate and long-term in their maturities, which explains their relatively high volatility. Investors who care about mark-to-market risk and think they’re being conservative allocating to AAA rated government bonds because of their safety or negative correlation with shares might want, therefore, to revisit their assumptions. If you really want AAA rated exposure, you have to hedge out the long-term interest rate risk by turning this into a floating-rate security.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management