Can mega-cap tech stocks continue to outperform?

Matt Peron

Janus Henderson

Investors have flocked to large technology and communications growth companies in 2020, even as macro drivers injected considerable volatility into financial markets. But though the recovery may be slow, the global economy will not be stalled forever, and many firms are adapting to shifting customer behaviours in a post-pandemic world. As this recognition grows, we expect more stocks to participate in market gains.

This year’s substantial market moves – first in response to the spread of the COVID-19 coronavirus, then from efforts to support the global economy – have been unique in that the same small grouping of technology and communications giants have consistently outperformed the broader market. What’s more, these mega cap stocks also powered U.S. indices to record highs in February. Given the strong year-to-date returns and higher valuations relative to the broader market, one could have expected that these stocks would experience the steepest losses in a sell-off. They did not. Instead, their performance reflected the continuation of certain market trends that have built up in recent years. This notable concentration has left investors wondering when attractive equity returns could become more dispersed. We think this will happen sooner than many think.

While the strong fundamentals of leading mega cap companies should keep these stocks in favour, the measured reopening of the economy and significant policy responses are likely to improve business conditions more broadly.

Furthermore, the disruption caused by the pandemic and acceleration in the shift toward a more digital economy could create opportunities for not just the largest technology platforms, but also well-positioned companies across the economy. As these events play out, we expect companies with the greatest ability to adapt their business models and thus gain market share and increase earnings – including some firms in presently out-of-favour sectors and asset categories – will be rewarded. Lastly, as has occurred in recent crises, once an economic recovery proves durable, investors tend to shift from seeking the most resilient companies to looking for other high-quality firms that may benefit from expanding valuation multiples.

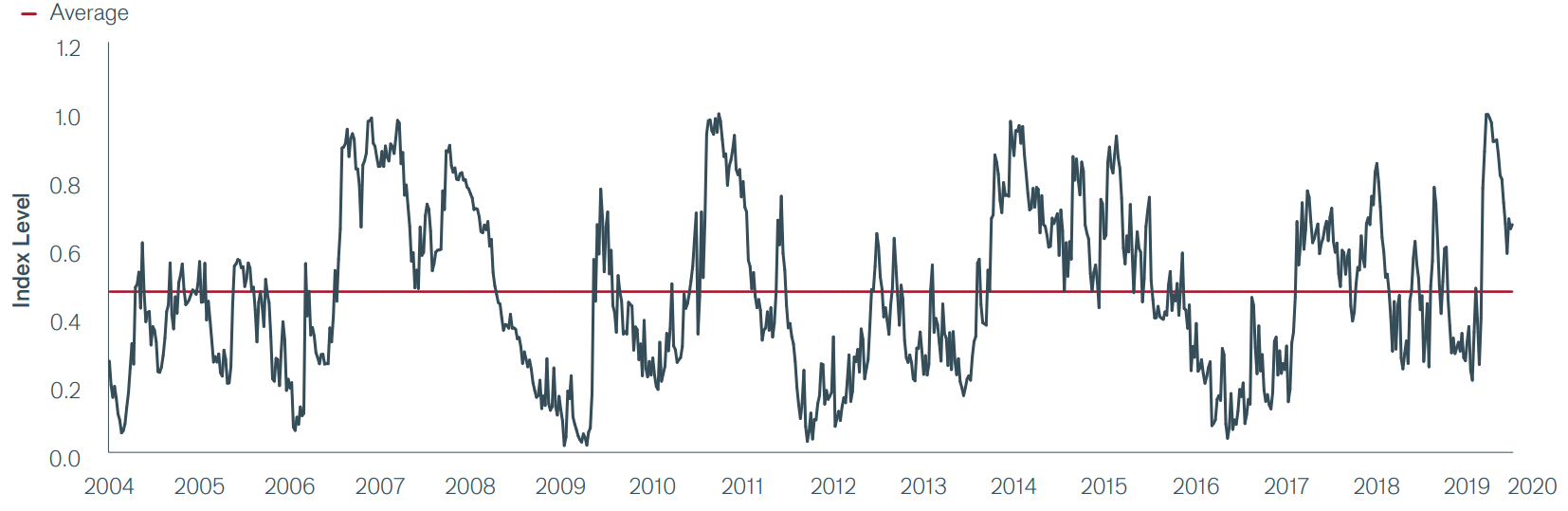

Exhibit 1: Citi Macro Risk Index

Similar to what occurred during the Global Financial Crisis (GFC), European Debt Crisis and the 2014-2015 oil price collapse, macro drivers have heavily influenced the direction of financial markets as investors react to the spread of COVID-19.

Source: Citi, Bloomberg. Data are weekly from December 31, 2004, through June 26, 2020. The Citi Macro Risk Index uses metrics such as credit spreads and equity volatility to gauge risk aversion in global financial markets.

The Year of the Macro

COVID-19 has been a jarring exogenous shock to the global economy. As such, macro factors – not just company fundamentals – have been a driving force behind financial markets in 2020. Once investors decided that mega cap tech and communications stocks were the place to be, market-cap weighted passive and algorithm-based momentum strategies did what they were structured to do: follow prevailing sentiment. The rise of market-cap weighted passive strategies means more investment dollars follow established market leaders. Similarly, algorithmic strategies based on momentum and minimum volatility factors – which have come to make up a significant portion of trading volumes – likely further strengthened the prowess of the mega caps. A similar setup has occurred in recent years as the market took cues from tax reform, monetary policy and trade wars.

The COVID-19 pandemic and ensuing monetary and fiscal responses have taken it to the next level. As Exhibit 1 shows, in 2020, macro risk across financial markets reached its highest level by certain measures since the waning days of the GFC. With macro risk rife, investors have doubled down on what they perceive as the most durable parts of the market. Given the magnitude of the pandemic, it is not surprising that secular growth has been rewarded and leverage and value have thus far been punished. As other companies have seen sales drop by 50% or more in recent months, many tech leaders have increased revenues, thanks to rising demand for cloud infrastructure, streaming media, virtual communication and other digital solutions.

This demand is only likely to grow as the pandemic stretches on, further entrenching recent changes to consumer and enterprise behaviours.

The search for durability has also led to dividend-paying stocks falling out of favour. While run-of-the-mill downturns would typically push investors toward companies committed to maintaining dividends, the magnitude of this shock has instead placed greater importance on preserving cash and shoring up balance sheets in order to weather additional tumult.

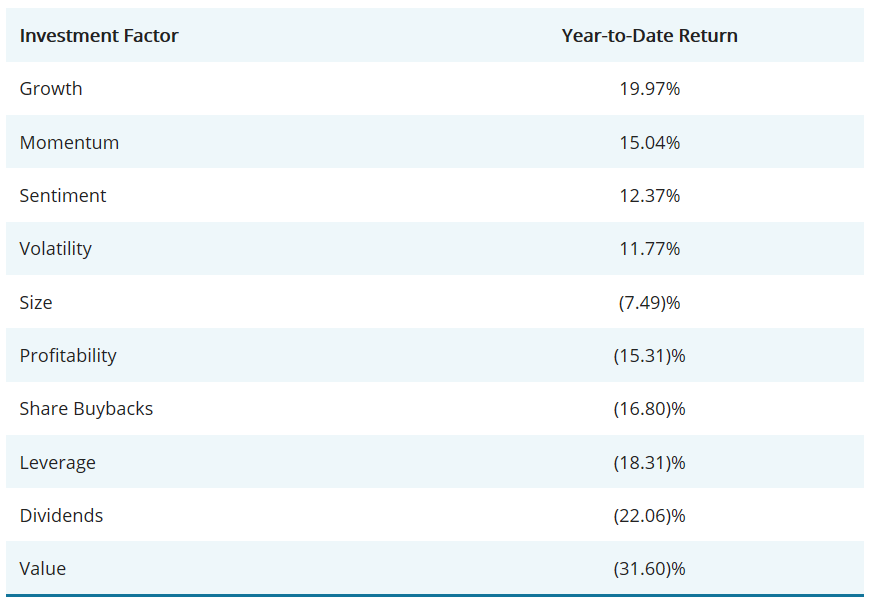

Exhibit 2: Year-to-Date Factor Returns

Difference in year-to-date returns between highest and lowest quintile of each investment factor.

Source: Bloomberg, as of July 1, 2020. An investment factor is a specific driver of return for an asset class. Factors can be macroeconomic in nature or a “style.” In this case, growth represents companies with above-average earnings growth; momentum is stocks with upward price trends; sentiment reflects investor attitude toward a stock; volatility measures the degree of change in stock prices; size reflects smaller high-growth companies; profitability refers to a company’s return on equity; share buybacks represent companies with significant share repurchases; leverage reflects firms with high debt ratios; dividends refers to dividend-paying stocks; and value reflects firms whose stock prices are discounted to a company’s intrinsic value. Return represents the difference between the year-to-date returns of the equally weighted highest and lowest quintiles of widely monitored all-cap, U.S. equity market factors.

A One-Sided Recovery

With large chunks of the global economy shuttering, equity markets entered their fastest bear market on record. Overall, stocks of large, cash-rich tech companies and Internet platforms outperformed during the sell-off, especially as some of these services were considered important tools for consumers and businesses to navigate the world of social distancing. Even as policy makers unleashed massive programs aimed at supporting markets and the economy, the mega caps continued to outperform as the virus spread and future growth turned increasingly uncertain.

As a result, the largest of these stocks, represented by the NYSE FANG+ Index, have returned 32.3% year to date, compared to -3.1% for the broader S&P 500 Index.

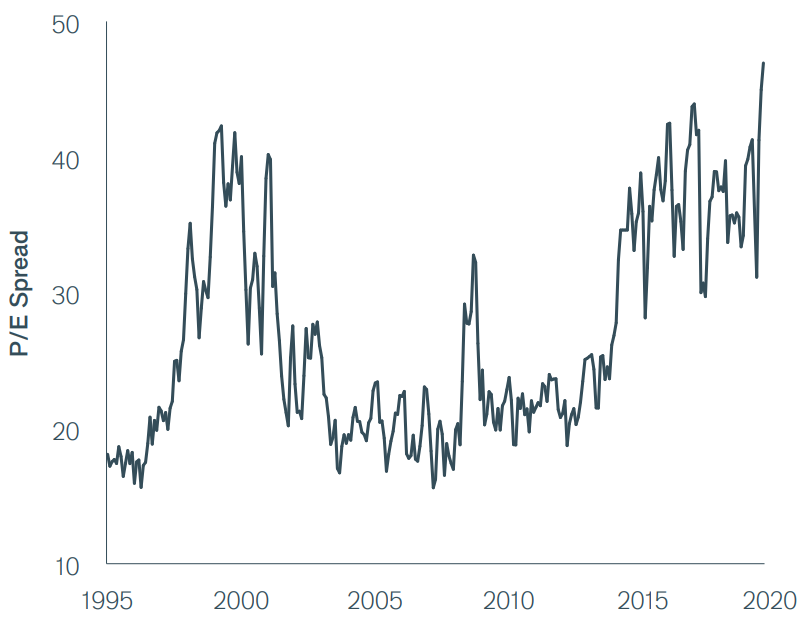

These diverging fortunes are also evidenced in valuations. The 2-year forward price-to-earnings (P/E) ratio for the five largest stocks in the S&P 500 is 39. Excluding those companies, the broader index has a P/E of 24, elevated by historical measures but comparatively lower than the market heavyweights. This has led to a record dispersion between the top and bottom deciles of companies based on forward P/E ratios. While investors’ logic may be sound in favouring cash-rich secular growers, we believe it is likely that other companies will also adapt and thrive, and that at some point conditions will allow undervalued segments of the market to recover.

Exhibit 3: S&P 500 2-Year Forward P/E Valuation Spread

Spread between the 2-year forward P/E of the most highly valued decile of stocks vs. the lowest.

Source: Janus Henderson Investors, Bloomberg. Data are monthly from December 31, 1995, through June 29, 2020.

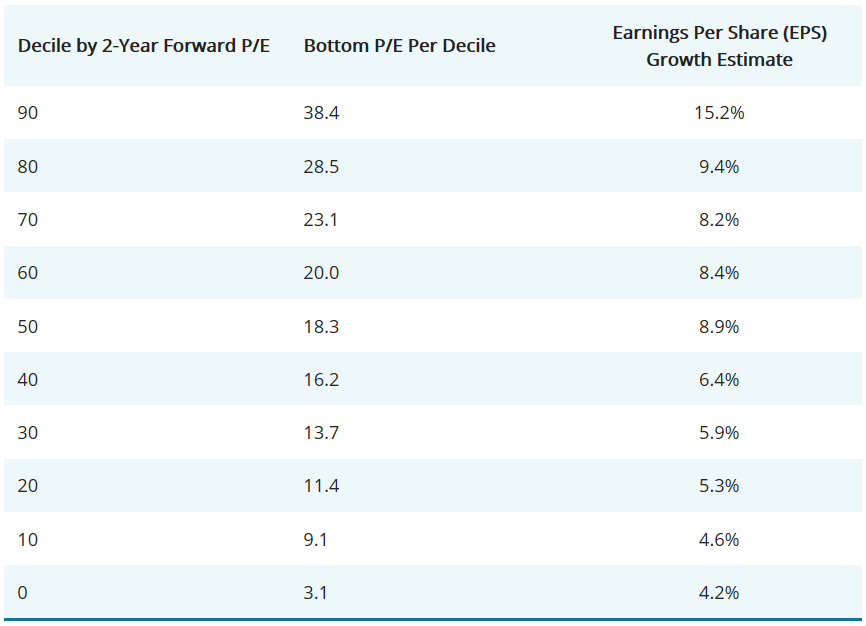

The concentration of both performance and high valuations within the largest companies poses a challenge for investors. In one respect – illustrated in Exhibit 4 – these richly valued companies offer the highest potential future growth rates. While their appeal can seem logical in an uncertain growth environment, their valuations may limit additional price appreciation on account of multiple expansion. Concentration within these mega cap tech names, whether driven by fundamentals or following a passive strategy, also lessens the diversification benefits of a broad equity portfolio.

Exhibit 4: Long-term Earnings Estimates Based on Forward P/E Decile

High valuations appear supported by strong growth rates, while stocks with the lowest valuations may reflect companies at risk of being disrupted. Middle-decile companies with attractive growth rates tend to be overlooked as all eyes remain on mega caps.

Source: Janus Henderson Investors, Bloomberg. Data as of June 30, 2020.

Source: Janus Henderson Investors, Bloomberg. Data as of June 30, 2020.Casting a Wider Net

For reasons discussed earlier, it is understandable if investors favour mega cap tech and communications companies. Yet, by focusing too much on these categories, investors risk ignoring other potential sources of excess returns, as improving economic conditions create an environment in which a broader range of companies can thrive. For that, we think investors will need to identify companies with attractive business models but whose prospects have been underappreciated by markets. This is what has been shown to happen in recoveries over the past several decades:

Investors’ preference for the allure of the high-growth first mover is replaced by the more deliberate fast follower. What’s more, many of the latter can carry valuations considerably lower than those of their higher profile peers.

Navigating the Digital Divide

In both cases, these companies have recognised that a digital strategy is paramount to future success. While digital storefronts and communications apps have garnered much of the attention during this era of social distancing, digital transformation creates opportunity in all facets of a company’s business model. Artificial intelligence coupled with the computational power of big data and the cloud has the potential to increase customer engagement and thus drive revenue growth. These same tools can also be deployed to streamline supply chains and administrative expenses, which can lead to the cost advantages necessary to capture market share or increase margins. Other companies either unwilling – or unable – to invest in the technology necessary to transform their business models risk falling behind.

This battle, which has been occurring over the past decade, has only intensified as COVID-19 upends the global economy.

For some laggard companies, recent events have jolted them into action. For others, it may be too late as their business models get disintermediated by digital-first alternatives. This presents an opportunity for active investors with a long-term view. It is our opinion that the companies with the most promising business models and steadiest fundamentals will be rewarded over time. Paradoxically, the same trend-following strategies that have caused such companies to escape investors’ attention may allow them to become tomorrow’s winners as the recognition of their attractive business models eventually ignites multiple expansion. Additionally, as the acute source of macro risk dissipates, correlations within equity indices tend to disperse and room is created for valuations across a broader universe of stocks – including many presently trading at deep discounts – to mean revert.

What Lies Ahead

As seen in recent recoveries from bear markets, opportunities for identifying attractively valued stocks relative to their future growth expectations tend to exist. It is too early to identify a clear path out of the coronavirus-impacted slowdown.

While we understand the appeal of mega cap tech stocks due to their growth prospects and cash positions, we believe that highly concentrated markets have let other promising companies fall through the valuation cracks.

Some of these – like the mega caps – have the business models that will enable them to add value in a post-COVID-19 world. Others may simply see a rebound in demand for their products as lockdowns continue to ease. Another category of businesses will see their end markets wither away as consumer demand shifts or dries up. In each of these cases, we expect that a company’s underlying merits will drive its stock performance over the long term rather than which investment style or sector it fits into. Accordingly, while recognising that passive and momentum-based strategies are not going away, they ultimately will follow company fundamentals rather than leading the charge as they recently have.

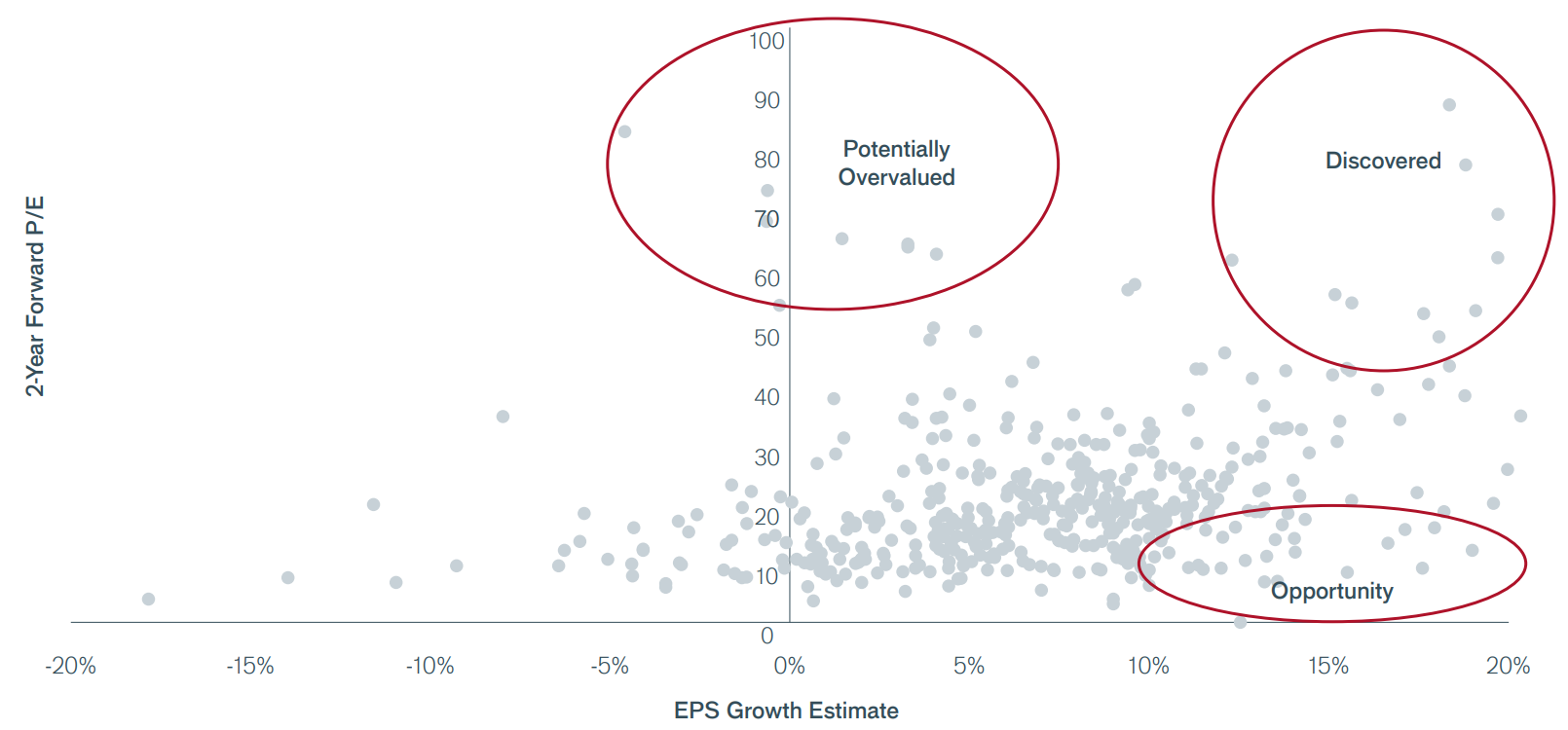

Exhibit 5: S&P 500 Stocks’ 2-Year Forward P/Es to Growth Estimates

A select number of stocks have both high P/E ratios and high growth estimates. Other stocks may appear overvalued, while some likely offer attractive growth rates but have been overlooked by concentrated markets.

Source: Bloomberg. EPS growth estimates are for the forward 2-year period. Data as of June 30, 2020.

Learn more

To access Janus Henderson's latest research from around the world, please visit our website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Featuring

........

This information is issued by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

Whilst Janus Henderson Investors (Australia) Institutional Funds Management Limited believe that the information is correct at the date of this document, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited to any end users for any action taken on the basis of this information. All opinions and estimates in this information are subject to change without notice. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect.

3 topics

Matt Peron

Janus Henderson

Expertise

Comments

Comments

Sign In or Join Free to comment