Cashing in on a crisis: Understanding, Overcoming and Profiting from 2020 and Beyond

While fully aware that very few commentators offering their opinion on the health and financial implications of COVID-19 are actually epidemiologists, GP’s and/or economists, it seems that people are nonetheless compelled to offer their views and opinions as if they were.

We don’t pretend to be any of those. But we have been closely following the experts and making every effort not to get caught up by the media hysteria. That is not to say that we don’t think that the coronavirus isn't serious. We do in fact think it’s the most serious threat that has faced this generation and has thus far impacted the global economy more than most recent wars have. However, we do believe that much of the coverage has been split along political party lines - a terrible indictment on our culture.

Our view for some time is that there simply remain too many unknowns to establish any serious point of reference as to the severity of the virus. For instance, while in China the data would suggest that the virus is very manageable and has a relatively low mortality rate, the statistics from Italy paint a very different picture.

While many news sources focus on identified infections, and the proportion of patient deaths, both measures are an unreliable indicator of the threat of the virus and are determined more by the number of tests being undertaken rather than providing real insight.

The only true indication of the seriousness of the coronavirus and its mortality rate can be identified once the rate of testing has radically improved - in terms of speed, accuracy, and availability.

Animal spirits and innovation: Creativity born out of crisis

Promisingly, as the bureaucrats begin to get out of the way of private industry, the management of this pandemic begins to look like it’s something that can be achieved. In the last week (early April), two US companies have developed testing kits that take between two and five minutes to generate a result. This compares to early efforts by government agencies that sometimes took days to assess.

Similarly, private companies all over the world have stepped up and adjusted their production lines to provide protective personal equipment. Textile companies that until last month were creating pillows are suddenly creating N95 face masks. Breweries too have found that with some small adjustments, their machinery can provide hand sanitiser.

The outlook is certainly uncertain, but as more data becomes available, and as global governments and industry works together, we have no doubt that a solution - cure, treatment and/or vaccine - will be developed.

Once that occurs, we have enough faith in the resilience of mankind to suggest that the world will implement some changes, and broadly move forward once again.

Economic and Social Impact

While the long term implications of the pandemic is something beyond the scope of this article and will be determined to some degree by the reaction of global governments and the stubbornness of the coronavirus, we do anticipate some economic and social change.

First and foremost, we imagine that many companies that will be forced to lay off workers will discover that they can achieve far more than they realised with a skeleton crew. Necessity may be the mother of invention, but it’s also closely related to efficiency. Where a company formally employed five staff to complete a job, they may discover that it can be achieved with just three or four.

We expect that many workers who have become accustomed to making themselves busy looking busy will be found to have been superfluous to a company’s needs. Afterall, when suddenly working from home, looking busy won’t suffice when achieving outcomes is required.

For many years, companies have been seeking to find ways to better balance work and life. One of the more popular endeavours was to enable staff to work from home. Historically, that transition has not been smooth. However, in the face of forced social isolation, many roadblocks that were previously thought to be insurmountable were suddenly resolved. When quarantine and social isolation comes to an end, we wonder if businesses won’t encourage their staff to work from home more regularly.

However, the most impactful change moving forward might be our attitude towards debt. For a generation, debt has fueled large parts of global GDP growth. Governments have borrowed money at near zero interest rates, and the average Australian consumer has approximately $1.25 in debt for every dollar in earnings.

This situation was always unsustainable, but in the face of a sudden loss of cash inflows, many people and businesses are discovering that they are unable to fund their lifestyle and debt. Government and banks may be able to delay the inevitable for 6 months or so, but eventually businesses who are not yet back in operation, or at the very least not back to full capacity, will find themselves uncomfortably at the mercy of lenders.

With all that said, it’s important to recognise that the stock market is correlated with economic activity but tends to be a leading indicator. As such, it is possible to be experiencing difficult economic periods while share prices increase.

Impact on Equity Markets

As far back as 2017, we identified the market as expensive. Our expectation at the time was that the high level of household debt (particularly home ownership) would begin to unwind causing a correction to both the property market and the stock exchange.

Instead, Central Bank and Government intervention saw a relaxing of lending laws and a significant fall in interest rates, the confluence of which saw all asset values increase.

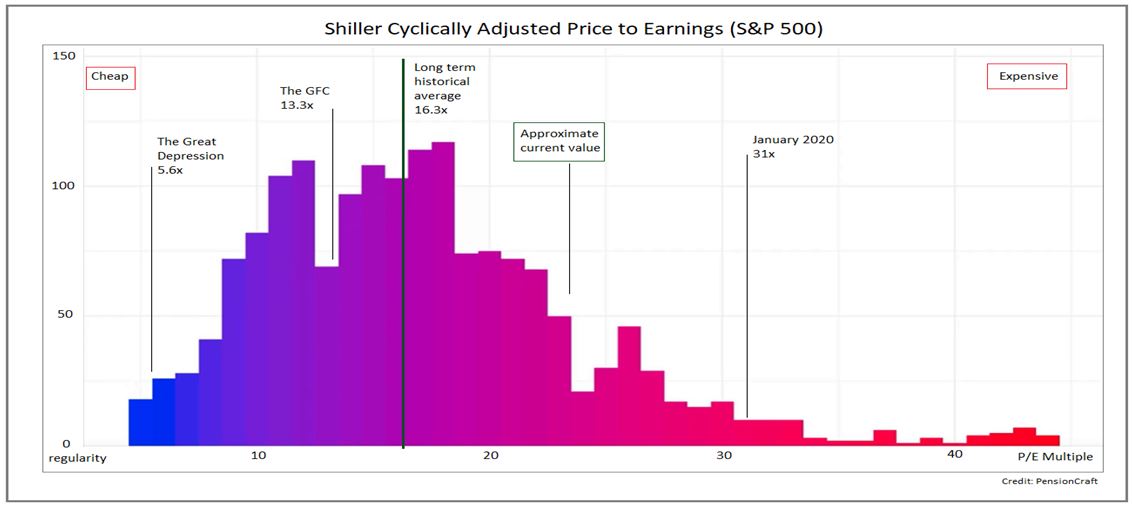

Nevertheless, no amount of intervention can be sustained indefinitely, and we remained confident that some sort of slowdown was on the horizon. The following graph identifies just how expensive US markets had become as they reached their peak in January. This chart is based on data going back over 100 years. As such it will be impacted by the type of companies that make up the index. However, it is abundantly clear that at 31x earnings, US equities were enjoying a period of optimism that was unlikely to be maintained.

In Australia, the data is similar. In the run up to our recent correction the markets unadjusted P/E (based on Morningstar data) reached as high as 18x - significantly above the historical average of around 14x-15x, with the recent correction seeing the market multiple down to approximately 13.5x.

This puts the market in Australia at cheaper than average, but quite some distance from the <10 times earnings we saw during the GFC. To put it in context, the S&P ASX200 would have to fall to just 4000 to return to GFC levels, and that’s assuming that earnings don’t fall as a result of the current pandemic.

Where we see the market headed

The market in early 2020 was objectively expensive, and though it seems that multiples are more reasonable, we maintain concerns that there may be an additional leg down as earnings downgrades impact share prices.

Additionally, an unwinding of debt could see a reduction in cheap borrowed money searching out a home, and see a protracted period where the index continues to meander around current levels.

That said, we believe that we have seen ‘peak panic’ play out in mid March as markets fell faster than ever before on the back of general concerns about the pandemic, and a rapidly increasing death rate, before plateauing as the cities of Los Angeles and New York shut down. At the point that it seemed that the world couldn't see the light at the end of the tunnel, that’s the point where it is safe to assume an over-reaction by the market.

This is not to say that we don’t think there will be challenges moving forward. In fact, between the cultural changes we expect to see from consumers, the impact of long term shut downs of major economies, and the unwinding of consumer debt, we think there could be a protracted bear market.

But uncertainty provides opportunity, and this is precisely the type of market that value investors thrive in.

We anticipate that for the foreseeable future, investors will abandon the idea of investing in index funds. Afterall, in a time where there will be clear winners and losers, who wants to invest in the losers (other than the index funds by mandate). But before that occurs, we expect cheaper prices.

And in terms of identifying the turning point for the markets, historically there have been a number of reliable indicators. These include:

- Capital raisings (that struggle to get filled);

- Business failures;

- Opportunistic takeovers of companies with no other options;

- Revised earnings (downgrades, not removal of guidance);

- Objectively low multiples; and

- Commentary suggesting the death of equity markets.

While the market is not quite cheap enough for us, there are a number of individual companies that are getting close.

Businesses raising capital via institutional placements are a perfect starting point for us. Once establishing that the business itself is sound, a heavily discounted capital raising will often resolve the issues that the company previously had - thereby providing us with the opportunity to invest in a good quality company, with no near term concerns, at a price significantly lower than where it was just 4 weeks (or even 4 days) ago.

What we are doing

Underscored by a 35% cash weighting and positive flows the Collins St Value Fund approaches the situation from a position of strength.

Indeed, whilst the broader macro environment could be challenging for some time, and present substantial challenges for people buying market like returns, our unconstrained investment mandate gives us enormous flexibility to deploy capital opportunistically in the pursuit of superior medium to long term returns – be it into a heavily discounted capital raise, an independently originated convertible note or a niche sector / stock that has flown under the radar of the larger institutional investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is the MD and one of the founding partners of the Collins St Value Fund.

The Collins St Value Fund is one of the best performing Funds in Australia - having ranked among the top 10 performing funds across all Australian Equity mandates by Mercer in 2019 & 2020.

With no fixed management fee, the investment team only benefit when our investors do.

4 topics

Michael is the MD and one of the founding partners of the Collins St Value Fund. The Collins St Value Fund is one of the best performing Funds in Australia - having ranked among the top 10 performing funds across all Australian Equity mandates by...

Expertise

Michael is the MD and one of the founding partners of the Collins St Value Fund. The Collins St Value Fund is one of the best performing Funds in Australia - having ranked among the top 10 performing funds across all Australian Equity mandates by...

Expertise

Comments

Comments

Sign In or Join Free to comment