Catching the credit reset

While the ongoing COVID-19 pandemic is tragic and has been incredibly disruptive to billions of people around the globe, it has provided credit investors with a speedy reset to valuations. As is common in all major risk off events, potholes and new opportunities have appeared for active managers to access higher risk-adjusted returns.

Throughout this period, we’ve continued to

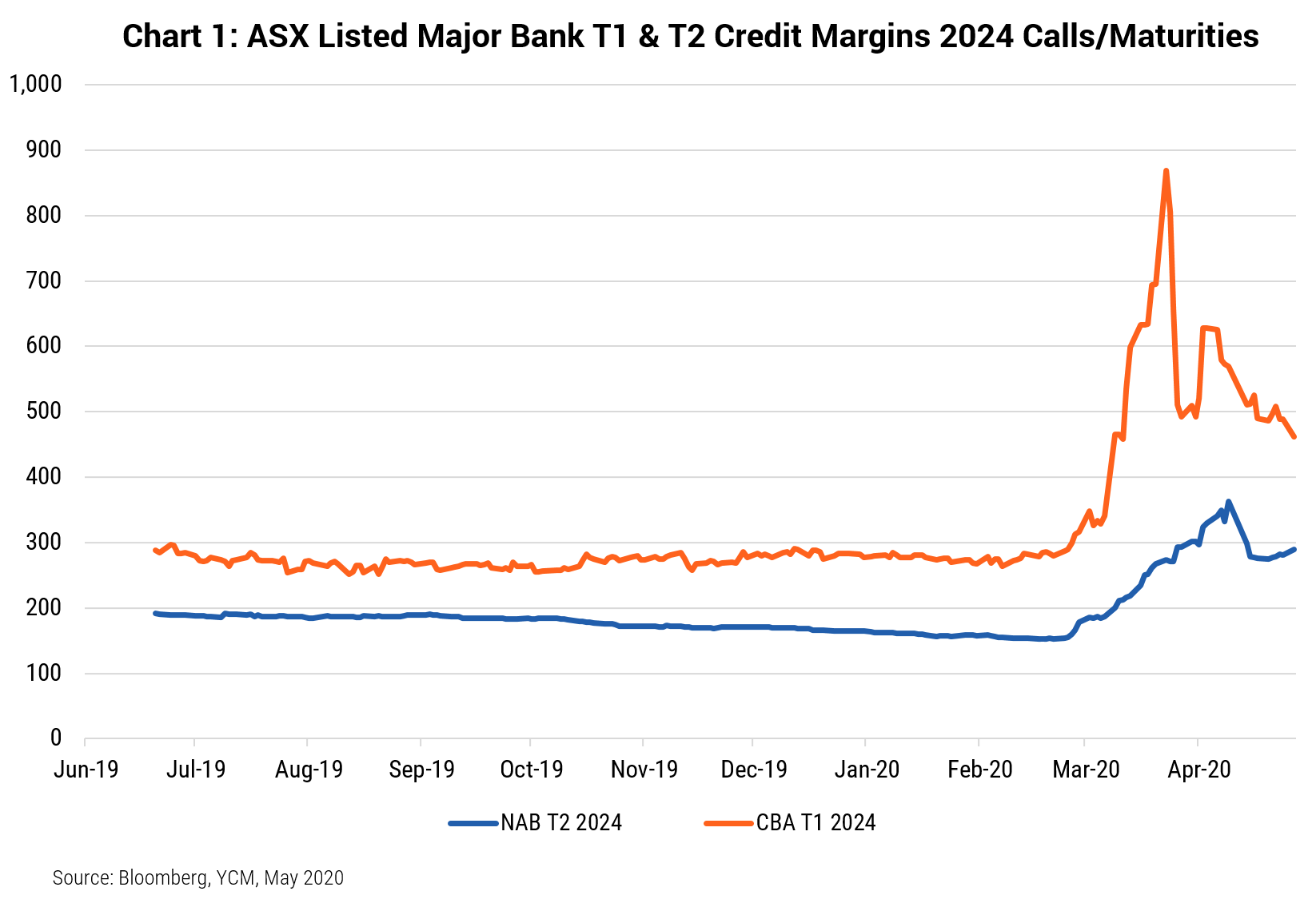

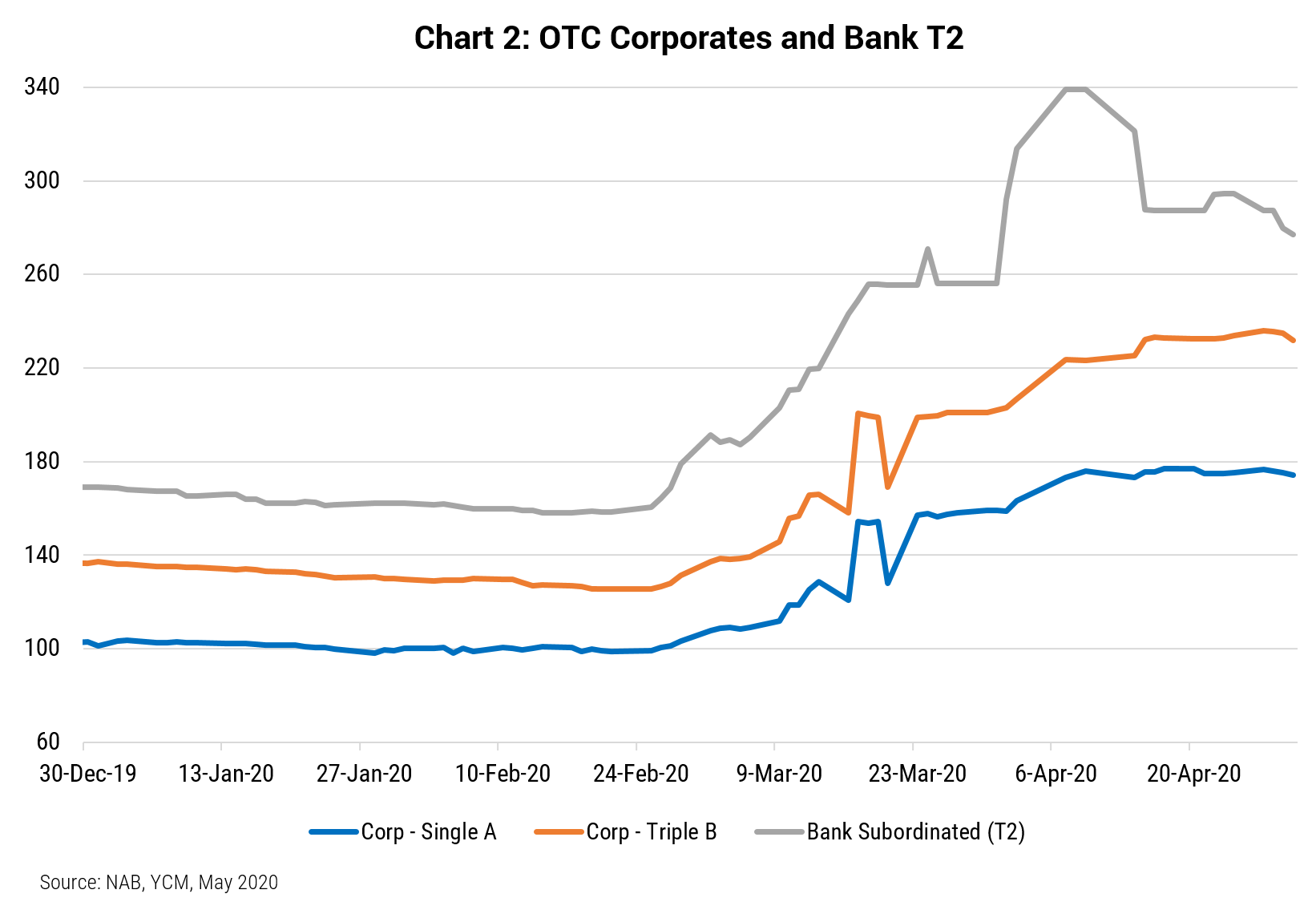

deploy capital, selectively buying financials and corporates in both the ASX-listed

and over the counter (OTC) markets at credit margins on average 2-3 times

pre-pandemic levels (refer Charts 1&2). Moreover, we’ve also more recently participated

in new primary deals with similar mark-ups. The BB+ rated Macquarie Bank Capital

Notes 2 (Tier 1) offered particularly exceptional value: the new issue credit

margin of +470 bps was 180 bps wider than the postponed transaction in March.

In the OTC space, credit margins for BBB+ rated major bank Tier 2s (T2) more than doubled in March and have outperformed since. We purchased the NAB 2026 T2 securities close to their peak credit margin of +400 bps in late March. They are currently trading 130 bps tighter at approximately +270 bps, still significantly above their mid-100s bps level in mid-February and with further room to perform.

Away from financials, we are finding compelling opportunities in corporates. Despite seemingly being inoculated from the pandemic, data centre operator NEXTDC recently undertook a substantial (and somewhat opportunistic!) equity raise to fund growth capital expenditures. With its BB+ rated (internal) notes trading at quasi-distressed levels at the time, we purchased the 2022 notes in late March at a double digit yield. At a current yield of 5.75% (credit margin +550 bps), we see scope for significant outperformance.

Among investment grade corporates, the 5-7 year BBB rated Incitec Pivot (IPL) and Downer (DOW) bonds also offered attractive entry levels (>400 bps), with current credit margins holding above 300 bps. Both companies are less impacted by the pandemic and, in IPL’s case, a $600mn equity raise has added additional strength to its balance sheet.

Despite finding pockets of opportunity amidst the calamity, we continue to take a highly selective approach. We remain cautious in the REIT credit space, holding a much higher allocation hurdle due to the likely decline in commercial and residential property valuations over the next 6-12 months.

Overall, credit margins across the board are ~double those observed in February, and while we can expect some additional volatility as we navigate our way out of the pandemic, the reset in credit valuations offers investors an attractive entry point.

We are optimistic that our credit funds today

are well placed for a significant period of outperformance, backed by a

relatively high yield (4-5%) and improved quality from an opportunistic

rotation into higher rated issuers.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Phil is the lead portfolio manager for Yarra Capital Management’s Higher Income Strategy. A credit specialist, Phil has more than 20 years experience in financial markets across asset management and institutional banking.

5 topics

Phil is the lead portfolio manager for Yarra Capital Management’s Higher Income Strategy. A credit specialist, Phil has more than 20 years experience in financial markets across asset management and institutional banking.

Expertise

Phil is the lead portfolio manager for Yarra Capital Management’s Higher Income Strategy. A credit specialist, Phil has more than 20 years experience in financial markets across asset management and institutional banking.

Expertise

Comments

Comments

Sign In or Join Free to comment