China’s Debt Bonfire is a Disaster in the Making

China’s debt bonfire has been building for decades, but recent news and data points to it growing faster than ever with a greater risk of becoming an economy scorching inferno. There’s three key components to this analogy, the wood, the accelerant and the matches.

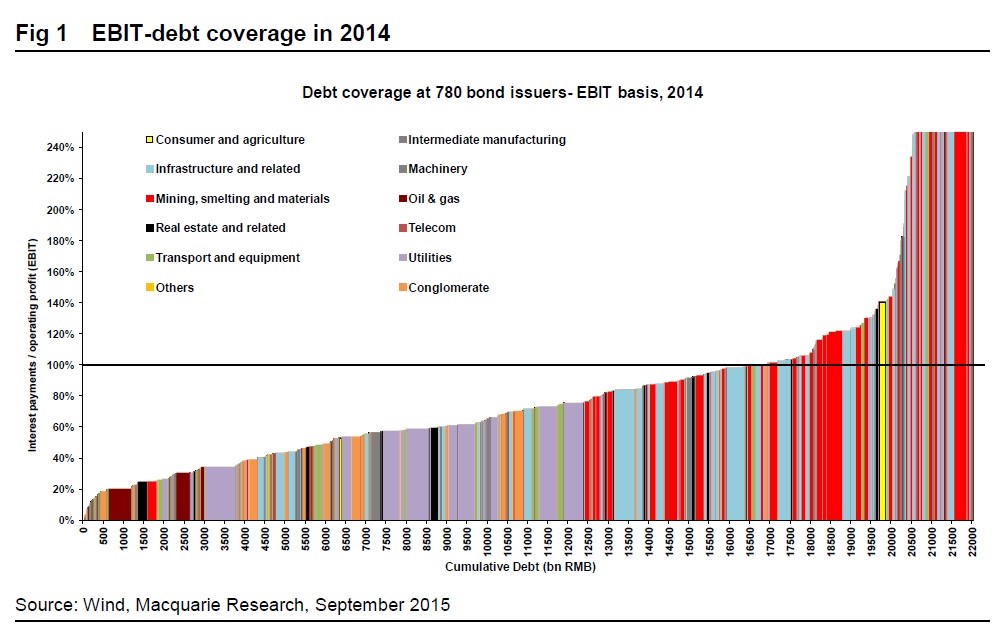

Firstly the wood, which is an ever growing stockpile of debt that cannot be serviced from profits. As shown below, Macquarie Research found that 23% of bonds issued were by companies that don’t generate enough operating profit to cover their interest. This aligns with a Bloomberg report that the median Chinese listed company generates enough operating profit to cover their interest two times, down from a ratio of six times in 2010. Another report found that 45% of new company debt is raised to pay interest on existing debt. In a developed economy Ponzi lending of such an enormous scale would lead to widespread bankruptcies, unemployment and massive losses for investors and lenders.

This hasn’t happened yet because Chinese debt has been expanding at an ever faster rate. China’s total debt levels grew at almost 50% of GDP last year and set a new record for a single month in January growing at roughly 5% of the size of the economy. Problems have also been covered over as the Chinese banking regulator is forcing banks to lend to companies that can’t pay their interest and would otherwise default. We know that the bonfire is big and the wood is dry, the next step is to figure how quickly a fire could spread once it begins.

The second key component is the accelerant, which is the relatively high proportion of debt borrowed for short periods. Chinese wealth management products are typically sold by banks as an alternative to term deposits that pay much higher interest rates. Borrowers are almost always promised their money back within six months. The underlying investments are typically loans to companies that banks are unwilling to lend to. These borrowers have little prospect of repaying the debt at maturity unless someone else is willing to provide more debt.

Another source of short term funding is peer to peer platforms, however 28% of these are thought to be fraudulent. In the institutional funding market there’s commercial paper, which is composed of corporate debts of 270 days or less. Outstanding Chinese commercial paper was US$1.61 trillion at the end of 2015, far larger than the US equivalent at $1.05 trillion.

As shown by the financial crisis in 2008, short term debt is an accelerant to fires in credit systems. Within a week of the collapse of Lehman Brothers 26% of US commercial paper disappeared. Investors were no longer willing to lend without asking questions and borrowers were sent scurrying for other sources of capital. A run on short term funding sources quickly spreads the fire from one bankrupt borrower to many other borrowers.

Thirdly, there’s the matches, which in China’s case is the increasing number and size of defaults. The February collapse of the US$7.6 billion Ezuabo online lending platform is thought to have ensnared up to 900,000 Chinese “investors”. It was followed by the US$3.9 billion collapse of Zhongjin Capital Management earlier this month. This week the state-owned China Railway Materials Co Ltd has halted trading on US$2.6 billion of debt, including commercial paper, as it investigates options for restructuring its debt. At some point the increasing size and frequency of defaults will cause investors to lose confidence in debt investments and switch to bank deposits, physical cash or gold.

The ever growing bonfire of debt in China is unsustainable, particularly as many sectors and companies are unable to generate enough profit to service their interest. The need to borrow more to pay interest on the existing debt is reminiscent of the negative amortisation loans given to US subprime borrowers prior to 2008. The relatively high usage of short term debt means that once a fire is established it will quickly spread. Many borrowers will find themselves unable to rollover their debts with investors and lenders scorched in an inferno of bankruptcies.

The matches to start such a fire could be the increasing number and size of defaults this year. If lenders and investors lose their nerve, the Chinese government will be faced with a lose-lose decision to either backstop the credit system or allow investors to take substantial losses. The bonfire has been built, it is now only a matter of time before it burns.

Written by Jonathan Rochford for Narrow Road Capital on April 13, 2016. Comments and criticisms are welcomed and can be sent to info@narrowroadcapital.com

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

5 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management