Chinese monetary policy: Does ignoring the established norms signal the way to create higher inflation?

While the conduct of monetary policy in China is converging on what are established norms in advanced countries, in many ways it is still quite different. It is these differences which may provide the Chinese authorities with greater flexibility to avoid the consistent undershooting of inflation targets now bedevilling many countries.

The consensus in advanced economies : An independent and accountable central bank equals low inflation

After the high inflation of the 1970s a clear social consensus emerged that not only was price stability a common good under all circumstances, but also that its achievement depended on the ‘right institutional framework’. What constituted the ‘right institutional framework’ rested on three elements :

- central banks needed a clear mandate to achieve price stability;

- they needed independence over the instruments they could use to achieve their mandate;

- and monetary policy had to be embedded in a strong accountability framework requiring the central banks to explain how its decision contributed to its goals.

Belief in these elements saw societies gradually converged on a framework whereby monetary policy was removed from the pressures of short-term political agendas and delegated to independent central banks. The low inflation witnessed since the 1980s reaffirmed the broad consensus that granting independence to central banks had been successful in bringing inflation under control. Moreover, central bank independence came to be viewed as a, if not the, key factor in the lower volatility of output and inflation observed over this period – the phenomenon identified as the ‘great moderation’.

The evolution of monetary policy in China

The conduct of monetary policy in China has evolved over the years with policies tending to move more in line with those applied within advanced countries. Pre 1998 the implementation of monetary policy by the People’s Bank of China (‘PBOC’) was primarily through the credit plan, which involved the aggregation of industry and local financing needs compiled from the bottom up. Policy evolved post 1998 to the PBOC targeting the quantity of money; initially M2 and then from 2011 a new indicator called the ‘social financing scale’. Finally, after mixed results from targeting the quantity of money, in 2015 the PBOC introduced an interest rate corridor to assist in guiding its operations. The transition to utilising an interest rate target was reinforced in 2018 when the central government stopped declaring a quantity target for monetary policy. Like the US Federal Reserve rather than targeting a set interest rate the PBOC aims to keep the target interest rate within a corridor.

How does the PBOC stack up against the consensus in advanced economies?

But while the PBOC’s targeting of an interest rate target is in line with the approach followed by other central banks in many ways China’s implementation of monetary policy falls short of the consensus view advocated in advanced countries. To see why the PBOC’s decision making framework can be considered in the context of the three elements which constitute the ‘right institutional framework’.

- Clear mandate to achieve price stability

Unlike some other central banks in advanced countries the PBOC does not have a mandate to achieve price stability. The PBOC Law sets out that ‘the aim of monetary policies shall be to maintain the stability of the value of the currency and thereby promote economic growth’. Against this overarching objective the PBOC will also be set other objectives which may vary over time according to central government objectives. Examples of such additional objectives include supporting certain government activities such as banking recapitalisations and low-income housing.

- Independence and accountability to achieve their mandate

PBOC has an absence of full instrument independence and related accountability. This reflects China’s political and institutional arrangements, among them the single-party state system and the highly coordinated nature of economic policymaking. Within this coordinated policy making structure the PBOC comprises just one of 35 members on China’s foremost decision making body, the State Council. Effectively, the operational autonomy of the PBOC is restricted to the more technical aspects of monetary policy implementation such as open market operations and the corridor system for interest rates.

A further issue adversely impacting on accountability is that, given its range of objectives, the PBOC has a correspondingly broad range of policy tools which it can utilise. The range of policy tools include open market operations, reserve requirement ratios, benchmark interest rates, rediscounting, standing lending facilities, medium term lending facilities, window guidance etc. Though counting the tools is complicated some estimates put the number at greater than 20 (compared to around 5 tools, depending on definitions, available to the US Federal Reserve). The issues that arise from this are evident with respect to the interest rate target. Not only does the PBOC have a range of interest rates which it can utilise to implement policies but which has greater priority can also change over time. The issue that such a broad range of tools can create for accountability is that it becomes less clear what the aims of the PBOC are when a change in one or more of the tools is announced.

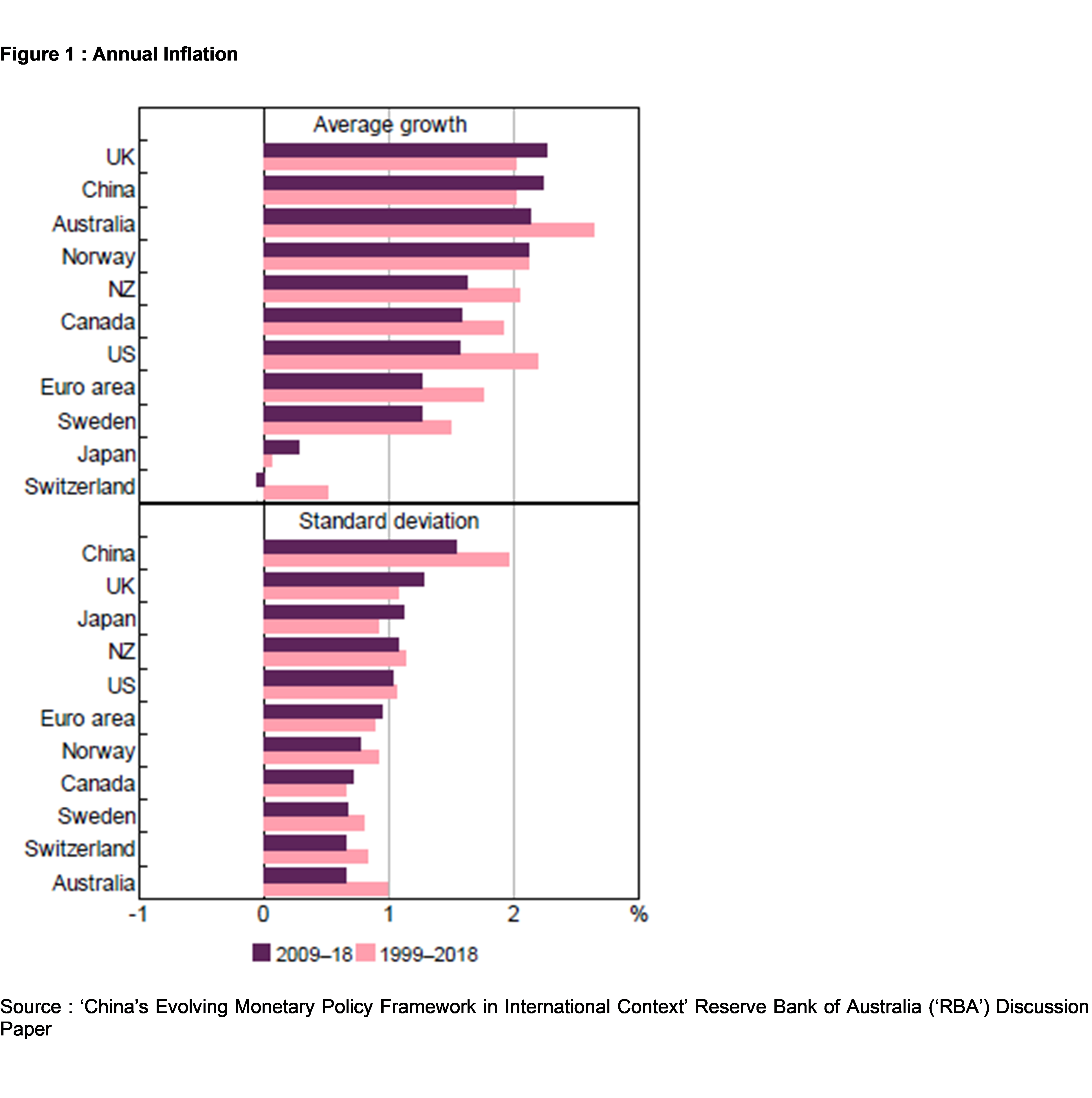

What is China’s inflation experience?

On the face of it then China lacks an institutional framework consistent with achieving a low inflation outcome. While acknowledging that inflation will be impacted by a broad range of factors, lacking ‘the right institutional framework’ the PBOC should have been less successful, all else being equal, in maintaining a low inflation environment than their more independent counterparts.

Yet as data for China (see Figure 1) highlights the experience with respect to inflation has not varied materially from other advanced countries which possess the ‘right institutional framework’ for maintaining low inflation. While much of the improved inflation and growth performance recorded in advanced economies since the early 1990s has been attributed to instrument independence and the adoption of inflation targeting as a clear and ultimately effective nominal anchor, it is interesting to observe that while average inflation outcomes in China have been similar to a number of advanced economies these outcomes have been generated in very different institutional contexts.

Lack of central bank independence may not be as bad as some suggest

The similar experience of countries with quite different institutional structures suggests that this lack of central bank independence may not be as big an issue as some make out. Indeed, a reason for the success of China in keeping inflation low may relate to the coordination of the whole-of government response that can effectively mobilise in response to concerns over high inflation or deflation. Conducted largely through the State Council, the formulation of aggregate supply and demand management policies is more tightly coordinated compared to other economies. The various arms of policy such as fiscal, monetary, macroprudential, exchange rate, sectoral and national development policies can each be adjusted in a timely, reinforcing manner in support of desired inflation outcomes. If the prospect of high inflation and deflation is viewed by the authorities as sufficiently grave to warrant a swift countercyclical mobilisation, all arms of government can be utilised to bring about the desired outcome. It follows that the institutional structure is less important than the overall social/political commitment to maintain a low inflation environment. To date the Chinese authorities appear to have displayed both the willingness and the ability to deliver on the objective of low and stable inflation, albeit through different means than observed in advanced economies. As noted by the RBA ‘It may be that standard incentive misalignment and commitment problems regarding central bank independence and inflation targeting may be less pressing in China’s unique institutional setting given that the prospect of high inflation and deflation is viewed by the authorities as sufficiently politically worrisome’.

China’s approach to managing monetary policy differs from the traditional wisdom of what is required to maintain low inflation rates. Despite this the commitment shown by the State Council to maintaining low inflation has allowed China to coordinate all arms of policy to achieve its aim of low and stable inflation. Indeed, as central banks around the world now grapple with the question of how to increase inflation their very independence may prove a hindrance where more than one arm of policy needs to be coordinated to achieve an inflation outcome. It is against this backdrop that the more coordinated structure of policy setting within China may give the authorities an advantage in preventing the type of consistent undershooting of inflation targets now bedevilling many countries. Ironically by going against the consensus and not having an independent central bank China may be in a better position, if warranted, to push inflation higher.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

3 topics

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management