Conventional wisdom is wrong. Rate rises are good for property trusts

April was a month of streaks. The Prime Minister’s 30th straight loss in the polls dominated headlines, the Reserve Bank’s 89th consecutive month without a rate increase less so. But we’re now into the beginning of May and the RBA’s streak without a change in policy rate has stretched to 90.

This shouldn’t be a surprise. The cash rate remains at a record low 1.5% and the last change was down, 21 months ago. But, as RBA governor Philip Lowe has said, the next change is likely to be up.

The market appears to be pricing in the prospect of future rate increases. Year-to-date total returns of the S&P/ASX 200 AREIT index have been -1.2%, wiping out last calendar year’s modest gains and confirming what many dividend-focused investors already suspect – that interest rate rises, or even the prospect of them, are bad news for AREIT investors.

We beg to differ.

It’s true that as interest rates rise, all else being equal, the value of an asset’s future income stream falls. But it’s a little more complicated than that.

Interest rates are more than numbers on an analyst’s spreadsheet. When rising, they’re usually an indicator of buoyant economic conditions, a mark of low unemployment and inflation and high business and consumer confidence.

In such environments businesses expand, leading to increasing demand for office and retail space and logistics facilities. Low unemployment also results in improving consumer confidence, pushing up wages growth. This subsequently increases an individual’s ability and willingness to spend.

Higher demand for commercial office, industrial and retail space is a by-product of elevated economic activity. Eventually, rental receipts rise – driving long-term value for commercial real estate investors.

It may challenge conventional wisdom but this explains the mechanisms by which rate rises can be goodfor AREIT returns.

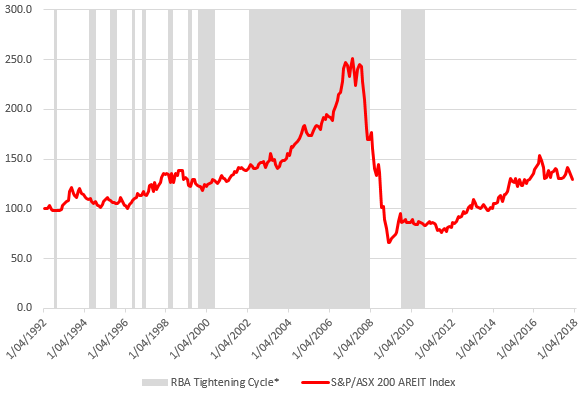

And the data supports the argument. This chart shows AREIT returns since 1992, highlighting periods when the RBA has progressively increased the cash rate:

S&P/ASX 200 AREIT Index Performance vs. RBA Tightening Cycles*

Source: RBA, IRESS, APN FM

*Tightening cycle defined as a period of consecutive rate increases or where multiple rate increases have been punctuated by a period of no change.

In the last five interest rate tightening cycles highlighted above – an aggregate 100 months – the S&P/ASX 200 AREIT Accumulation Index achieved an average annualised total return of 7.5%. Even after excluding the longest RBA tightening cycle from 2002 to 2008 (preceding and including the GFC) the AREIT sector returned 7.0%.

Of course, property trusts use debt to finance the ownership of their assets, thus exposing them to rising interest rates. Whilst higher debt servicing costs can be more than offset by rent increases, it’s also important to acknowledge that today’s environment is very different to that in the period prior to the Global Financial Crisis.

AREITs generally are now managing debt with more prudence. Gearing levels are lower and a greater percentage of debt is fixed-cost. Gearing across our AREIT coverage universe is now a low 29.6% and over 60% of that is fixed cost debt. If and when rates were to increase, they won’t hit a property trust’s cost base in the way they did a decade ago.

Moreover, further rate increases still seem a way off. GDP growth remains at below-trend levels, there’s little evidence of wages growth and inflation remains below the 2-3% range targeted by the RBA. The concern over an imminent rate rise seems misplaced and overdone.

But even if that changes and the RBA does raise rates there’s a strong historical precedent for it being a good thing for property trust investors. Because behind the case for higher rates are economic conditions that deliver increases in commercial property rents.

In our view there is no cloud hanging over the sector. There is however a silver lining, courtesy of those investors unduly worried by the prospect of higher rates.

For investors seeking sustainable, low risk income returns, with the prospect of higher rents if and when rates do rise, that seems pretty attractive.

Looking for more real estate insights and analysis?

Visit the blog to access the latest analysis and insights from a specialist real estate investment manager.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Mark is part of the Investment Team tasked with analysing and investing in global real estate-sector equities. He is an Associate of the Australian Property Institute, a Certified Practicing Valuer and a CFA charterholder.

4 topics

Mark is part of the Investment Team tasked with analysing and investing in global real estate-sector equities. He is an Associate of the Australian Property Institute, a Certified Practicing Valuer and a CFA charterholder.

Expertise

Mark is part of the Investment Team tasked with analysing and investing in global real estate-sector equities. He is an Associate of the Australian Property Institute, a Certified Practicing Valuer and a CFA charterholder.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management