Could the governments lending restrictions backfire?

The law of unintended consequences states that actions – particularly by government – can have adverse effects that are unanticipated or unintended. This law could soon play out as a result of lending restrictions placed on the major banks by the Australian Prudential Regulation Authority (APRA).

Regulators have imposed a number of prudential measures on the banks over the last few years to help protect the economy from systemic financial risk. In the middle of 2015, APRA introduced a 10% cap on investment proportion loan book growth. From 1 July 2016, APRA changed risk weight calculations on mortgages determined by the major banks from accredited risk modelling. This was designed to increase the average risk weighting on mortgages by around 60% for the major banks.

Despite these changes, residential property price appreciation in Sydney and Melbourne has continued unabated, increasing concerns about a property market bubble and the inevitable consequences for the broader economy when the bubble bursts.

This has led to press reports that the Government and regulators are looking at further constraints on property lending through the imposition of even tougher lending restrictions on banks.

From an investment perspective, what does this mean for the banks and the broader Australian economy?

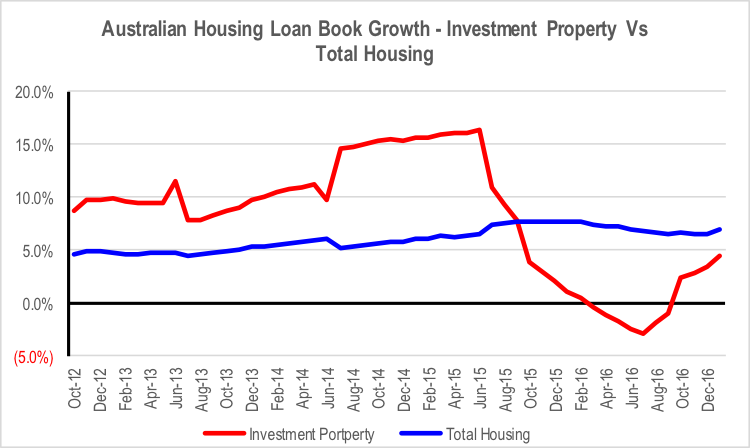

If we look at the impact of the measures taken to date, we note a few things. While it is true that the growth in the size of bank investment loan books slowed in late 2015 and into 2016, the rate of growth in overall bank mortgage books remained largely unaffected. This indicates that the reduction in growth rate of investment property mortgages was largely a function of a reclassification of existing mortgages from investor to owner-occupied. This temporarily hid the true rate of growth in investment property mortgage books. Consequently, once the data started to lap the imposition of the 10% growth cap, investment property mortgage book growth started to reaccelerate back toward previous levels.

Source: RBA.

Source: RBA.

The other impact of regulatory restrictions is being felt through mortgage rates. Any year 11 economics student can tell you that if supply is reduced as a result of an external factor, demand will be rationed in a capitalist economy through the price mechanism. In other words, as bank lending is restricted, the banks will increase the price of loans (ie the mortgage rate) to reduce demand to levels in line with the restricted supply. Hence, we have seen major bank variable and fixed mortgage rates on investment properties increase relative to funding costs and owner occupied mortgage rates.

If the Government and regulators impose further restrictions on mortgage loan book growth, such as the halving of the cap on investment property loan book growth to 5% or additional increases in some mortgage risk weights, expect mortgage interest rates to continue to increase relative to funding costs.

Out of cycle mortgage rate increases provide a positive driver of revenue for the banks through a widening of net interest margins, but this will be offset by a negative impact on loan growth. Higher mortgage rates will also increase the risk of an acceleration in mortgage arrears and defaults. Increased pressure on heavily geared households, combined with continued high levels of residential completions, increase the risk of asset issues for the banks and the broader economy.

But the other problem is that tighter regulatory controls of the banks that are designed to target a specific segment of the market are unlikely to be an effective tool in reducing the risk to the economy from the property bubble. This is because the liquidity from the resulting accommodative monetary policy of RBA does not just disappear because there are restrictions on bank mortgage lending capacity. The demand remains in the market, and in an increasingly innovative world, alternative providers of financing will accommodate the excess demand through non-bank financing solutions.

We have already observed this occurring in the commercial property market over the last couple of years with mezzanine finance tapping capital from high net worth individuals searching for yield. We also note the AFR recently reported comments from Mortgage Choice that there is plenty of non-bank financing capacity available to property investors irrespective of whether APRA further restricts bank level capacity.

The problem with this is that ARPA and the RBA have less control over these non-bank sources of funds. This could create an irony in that by trying to impose restrictions on the banks to prevent a bubble destabilising the broader economy, regulators could lose control over the rate of credit expansion by driving demand to these less regulated sources of financing, leading to an increase in economic risks.

The growth in less regulated non-banks in the 1970s and the resulting reduction in control over the banking system was one of the reasons why the banking system was deregulated in the early 1980s. Macro prudential policies being implemented at the moment run the risk of a repeat performance.

To quote Princess Leia, “The more you tighten your grip.., the more star systems will slip through your fingers.”

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

1 topic

4 stocks mentioned

Senior Analyst and Portfolio Manager

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Expertise

Senior Analyst and Portfolio Manager

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Expertise

Comments

Comments

Sign In or Join Free to comment