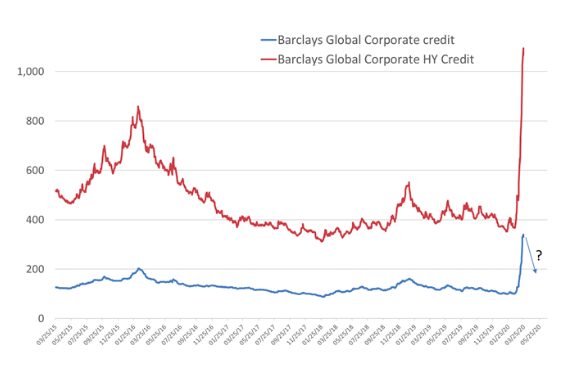

Credit spreads widen sharply

“Consensus is not always good; disagreement not always bad. If you do happen to agree, don’t take that agreement—in itself—as proof that you are right. Never stop doubting...” Philip Tetlock, Superforecasting

We have had a negative view of global credit as an asset class since early March. This has primarily reflected the breakdown in negotiations between OPEC and Russia to support the global oil price. The resulting 30% collapse in the price of oil was likely to immediately stress the highly leveraged cohorts of the US shale gas industry. Some estimates suggest these represent over 10% of US junk bond issuance. Moreover, as the COVID-19 spread globally, and the likely economic consequences grew, the potential for reduced cash flow to pressure corporate defaults grew.

As our chart today reveals, there has been a sharp widening in corporate spreads through March, signalling such stress in the global economy and moving in tandem with the historic risk-off bear market correction in equity markets. Overall, corporate credit spreads (both investment grade and high-yield) have widened from around 100bps mid-January to around 340bps at the start of this week, while the high-yield component has moved out to almost 1,100bps (from around 350bps mid-January 2020) to be above Dot Com bubble levels.

However, this week saw the US Federal Reserve (Fed) dust off its prior GFC crisis tools, confronted with this rising stress in credit markets, to announce it would be buying corporate bonds (and corporate paper) to boost liquidity. The Fed has established several facilities targeting investment grade bonds (not high-yield bonds, which it is prohibited from purchasing). As a consequence, the past couple of days have started to see a peak forming in corporate investment grade spreads, and there is a significant likelihood that, despite a near certain recession ahead in the US, that US investment grade and global investment grade spreads may nonetheless tighten given Fed and other global central bank action. However, high-yield spreads are unlikely to narrow as significantly, if at all, given they are not the target of central bank buying.

Corporate credit spreads

Source: Factset.

Be the first to know

I’ll be sharing Crestone Wealth Management's views as new developments unfold. Click the ‘FOLLOW’ button below to be the first to hear from us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

2 topics

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment