Currency exposure offers diversification benefits for Australian portfolios

Diversification has famously been described as the “only free lunch in finance”1 for its potential to reduce risk without sacrificing returns. It seems that this free lunch may be naturally larger for Australian-based investors who combine equity-heavy portfolios with foreign currency risk. Investors can harvest the strong and historically persistent correlation of the Australian dollar (AUD) to equities – a desirable feature compared with many other currencies. Our research suggests that a typical multi-asset portfolio can benefit from foreign currency exposure, which contributes to diversification and could reduce portfolio risk by up to 20%.

Using the Australian dollar to reduce equity risk

The AUD is considered a “risk-on” currency because the Australian economy is highly dependent on global growth, particularly in China, and commodity prices. The high historical correlation between the AUD and equities can partially be explained by Australia’s current account deficit and the banking sector’s reliance on offshore wholesale funding markets. In contrast, currencies like the U.S. dollar (USD) and Japanese yen are considered “safe-haven” assets that tend to appreciate in adverse environments.

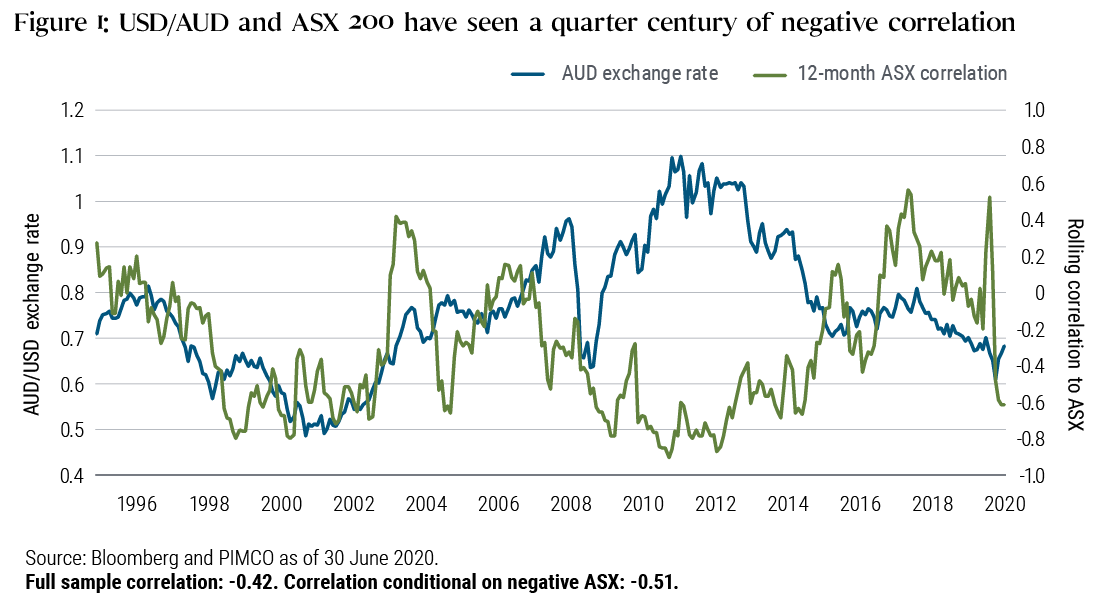

Over the past 25 years, the AUD/USD exchange rate has averaged 12% volatility annually, close to the 13% volatility level experienced by Australian equities. Despite similar levels of volatility, however, the AUD exchange rate (USD/AUD) has been negatively correlated to the ASX 200 over the same time period (see Figure 1).

Click to enlarge

This negative correlation offers diversification for portfolios dominated by equity risk. If a long AUD position demonstrates risk-on characteristics, then a short to the AUD indicates a “risk off” position. Holding a long position in USD and a short position in the AUD would partially offset a portfolio’s equity risk due to the negative correlation.

This relationship becomes even more pronounced in stock market downturns. An example is the March 2020 sell-off, which saw Australian stocks plunge by 21% while the USD appreciated 7% against the AUD. Portfolios that held a long USD/short AUD currency pair during the March volatility would, to some extent, have been able to hedge their equity drawdown.

Currencies can be a useful portfolio diversifier

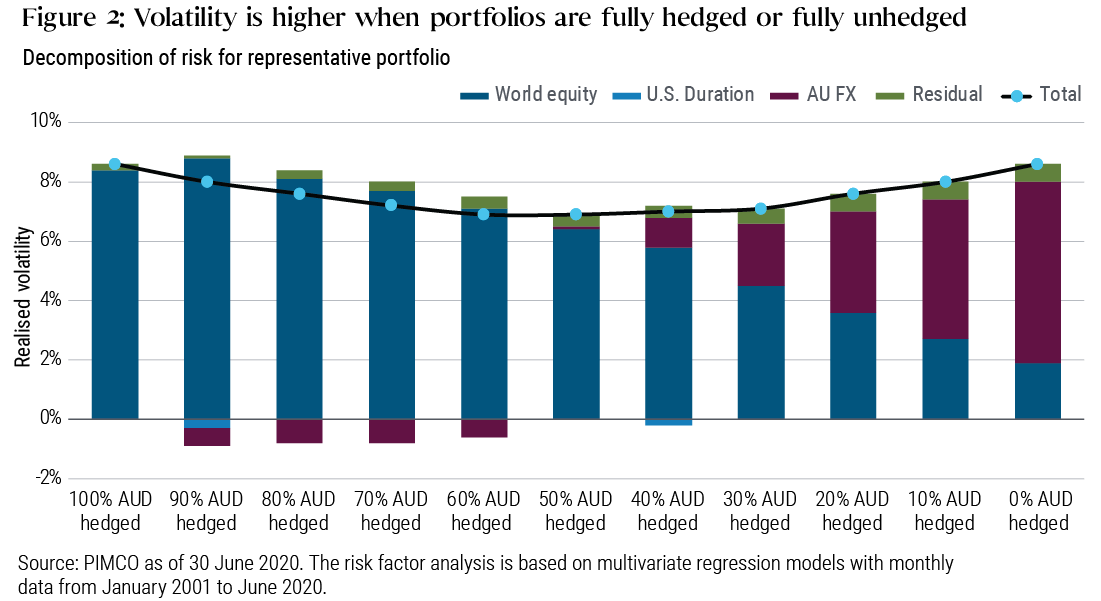

Using historical returns from January 2001 to June 2020, we analysed a typical 60% equity and 40% bond portfolio2 (the representative portfolio) to assess the risk profile under different currency hedge ratios.

Our analysis showed that introducing currency risk reduced a portfolio’s overall risk compared with having no currency exposure at all. Investors face high risk both when fully hedged and when fully unhedged.

As Figure 2 shows, we found that the lowest volatility position in the representative multi-asset portfolio held around 40%-50% foreign currency exposure (equivalent to a 50%-60% hedge ratio). A foreign currency exposure of 40% reduced the portfolio’s overall volatility from 8.6% to 6.9%, corresponding to a 20% reduction in volatility compared with the fully hedged portfolio. However, there was a tipping point where the currency exposure becomes large enough that foreign exchange (FX) becomes a dominant force of portfolio returns. At this stage (right side of Figure 2), adding marginal currency risk to the portfolio would increase overall volatility.

Click to enlarge

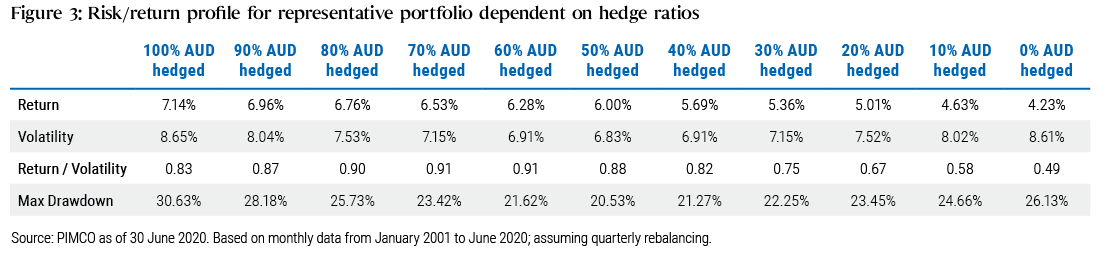

The maximum drawdowns in Figure 3 show that the left tail risk (chance of a loss occurring due to a rare event) was reduced by 40% for portfolios with a 40% currency exposure compared with the fully hedged portfolio. The portfolio with 40% FX exposure achieves the highest risk-adjusted return in our analysis.

Click to enlarge

It is worth noting that currency exposure interacts with other risk factors. Based on our analysis, to achieve the lowest risk in a portfolio, an Australian-based investor should take more currency risk as the allocation to equities increases and less currency risk as the allocation to bonds increases. The fact that core bonds have lower volatility than exchange rates and tend to be positively correlated with foreign exchange exposure (e.g., long USD/short AUD) explains why most bond investors hedge their currency risk. Of course, the optimal level of hedging in any portfolio will depend on an investor’s risk/return objectives and their appetite to include currency exposure as a key source of risk in their portfolio.

Optimal currency hedging

The above analysis shows how investors can improve the risk/return trade-off in their portfolio by adjusting a static currency hedge ratio. In a perfect world, without any operational limitations, investors would be even better off treating currencies as a distinct asset class in their broader portfolio construction.

In a 2019 paper, we demonstrated that a dynamic currency strategy that takes into account valuations and real carry differentials consistently outperformed a static hedging strategy. Currency overlays can be optimised to increase return and/or reduce risk, which may meaningfully improve portfolio outcomes in today’s low yield environment. And our analysis suggests that these strategies can perform particularly well for Australian investors.

How do other asset classes compare as portfolio diversifiers?

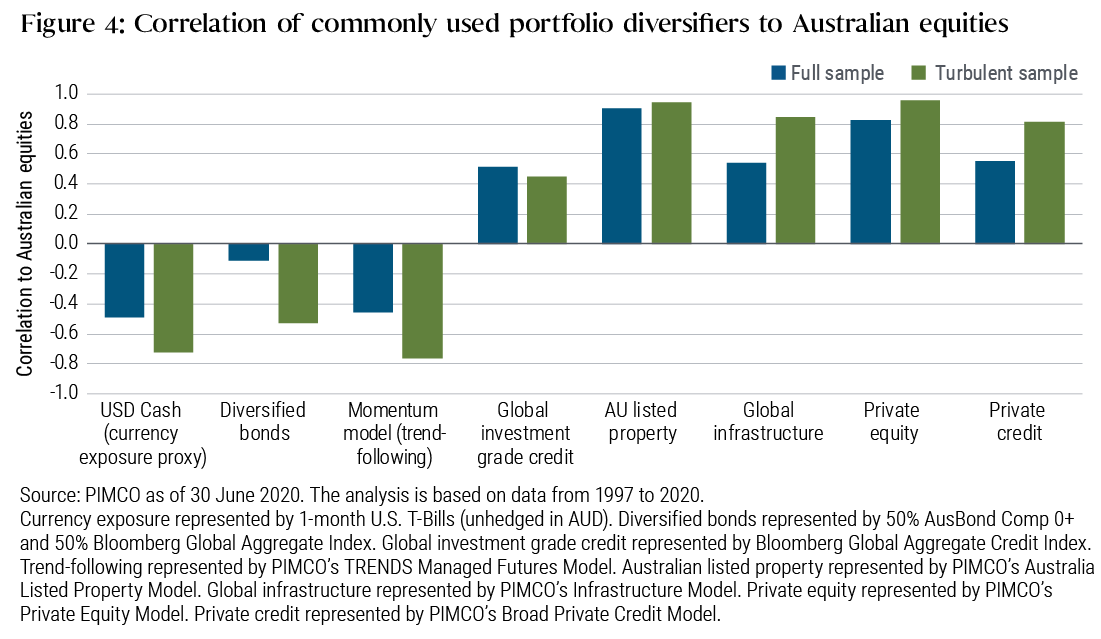

To fully understand and compare the benefit of currency exposure as a diversifier from equities, we analysed the diversification benefits of other asset classes popularly used by Australian investors. The below analysis relies on PIMCO’s risk analytics platform, which uses econometric modelling techniques to simulate risk factor performance and correlations. Since diversification is required most in times of market stress, we looked not only at full sample correlations that take all time periods into account, but also conditional correlations based on turbulent periods in financial markets. The most efficient diversifiers would have a low or negative correlation to Australian equities, particularly during equity market sell-offs.

As Figure 4 shows, currency exposure, core bonds and trend-following strategies are the only assets that consistently provide a negative correlation to Australian equities not only on average, but particularly when it matters the most in turbulent times.

Based on our modelling, it is also clear that Australian listed property, global infrastructure, and private equity demonstrate a high correlation to equities overall and close to zero diversification in times when it is most needed.

Click to enlarge

Diversify your diversifiers

As our analysis shows, foreign currency exposure acts as a compelling diversifier to equity markets, particularly in risk-off environments. While some domestic investors may be uncomfortable with a 40% exposure to foreign currency, the main takeaway for equity-dominated portfolios is that having some currency risk has historically been safer than having no currency risk at all. Bonds and trend-following strategies are examples of other historically effective diversifiers, whereas private equity and property tend to become more positively correlated to equities when volatility in financial markets rises.

Investors face a trade-off: Invest in assets with higher expected returns, but low diversification benefits, higher volatility and higher drawdown risk, or invest in assets with modestly lower expected returns, but higher diversification benefits, lower volatility and lower expected drawdowns in more turbulent markets. In our view, the most efficient portfolios should not rely on a single asset class for defence, but instead look to diversify the diversifiers.

Stay protected in times of volatility

We seek to provide all the benefits investors have come to expect from a core bond holding, including consistent income and low volatility, which can help stabilise portfolio returns. Find out more by click 'contact' below, or hit 'follow' to stay up to date with our latest Livewire insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Aaditya is a senior vice president and portfolio manager focusing on Australian dollar and global portfolios. He has 19 years of investment experience and holds a master's degree in commerce (finance) from the UNSW. He is also a CFA charterholder.

1 topic

Aaditya is a senior vice president and portfolio manager focusing on Australian dollar and global portfolios. He has 19 years of investment experience and holds a master's degree in commerce (finance) from the UNSW. He is also a CFA...

Expertise

Aaditya is a senior vice president and portfolio manager focusing on Australian dollar and global portfolios. He has 19 years of investment experience and holds a master's degree in commerce (finance) from the UNSW. He is also a CFA...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management