Developments in Inflation Expectations

Both UK and US central bank comments reveal thinking on policy responses to future rises in inflation.

Over the period between Friday 14 October and Tuesday 18 October, the heads of central banks in the US, UK and Australia made separate but somewhat similar comments regarding inflation. They all suggested that, if inflation were to rise, they may not act quickly to try to dampen it by increasing interest rates.

These comments are interesting in that they reveal some commonality in policy stances across the US, UK and Australia. Furthermore, markets may be gaining further confidence that governments will look to increase fiscal stimulus in light of growing consensus that monetary policy alone can’t do the job around the developed world of increasing inflation. The overall implication is that the perception of future higher levels of fiscal stimulus in the real economy combined with a more relaxed approach by central banks to inflation targeting is causing inflation expectations and volatility to increase.

Irrespective of whether governments are gearing up to increase stimulatory spending on infrastructure, for example, the reaction of markets to news and rumours signals to us that volatility in inflation expectations continues to pose a considerable risk in portfolios. This illustrates the need for explicit inflation hedging strategies and preparatory mandates should inflation expectations take hold and investors need to allocate rapidly to such strategies.

Innocuous Central Bank Comments Continue to Drive Markets

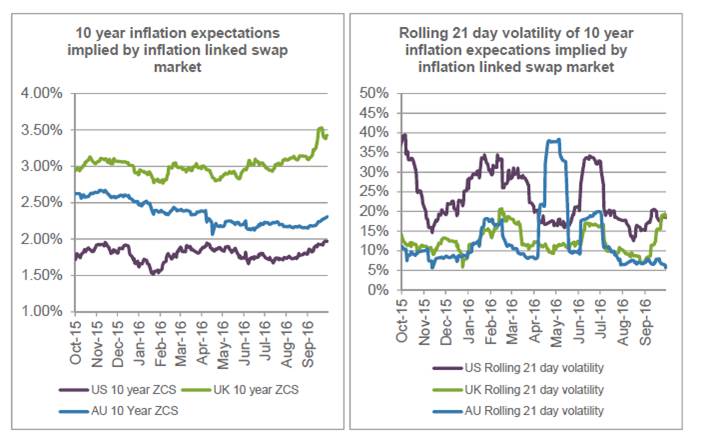

Recent rises in inflation expectations have been driven by very different factors in the UK and US. In the UK, the steep sell-off in the pound after the Brexit vote is almost certainly going to lead to higher prices for imported goods such as food. In the US, higher inflation expectations have been more naturally generated due to labour market tightening and rising wages. In Australia, the RBA’s shift to signalling caution about housing prices stands in contrast to its desire to see higher inflation and a lower Australian dollar.

Janet Yellen made comments on Friday that prolonged periods of low aggregate demand and output gaps in the economy can affect the ability of the supply side to respond when the business cycle turns (for example, the skills of workers who have joined the ranks of the long-term unemployed deteriorate).1 Her comments suggested that allowing inflation to run higher may be desirable if it were to assist with reversing these supply side effects. On the US fiscal policy side, markets have also reacted to pledges from both Clinton and Trump to boost infrastructure spending as well as deliver stimulus through tax cuts.2

Mark Carney, Governor of the Bank of England, also made comments to the effect that food prices will be the first to rise on the back of the fall in the pound, with inflation to “…show up” more broadly across goods and services sectors in coming years and suggested the Bank had to "…weigh increased inflation against supporting the economy3" through low interest rates. This stands in contrast to new Prime Minister Theresa May, who has previously disagreed with low rates and expressed a preference for a fiscal response to boosting the economy.4

Finally, RBA Governor Phillip Lowe made comments to a conference on Tuesday that whilst inflation is currently below target in Australia, domestic demand is expected to strengthen gradually over the medium term. He also spent a large portion of this speech reinforcing earlier policy positioning outlined in the RBA’s most recent statement on monetary policy around the flexibility that the RBA has around its inflation targeting mandate.5

Investment Strategy Implications

Irrespective of the actual or implied meaning behind the recent statements by central bank officials, it is the reaction of markets that is interesting. In the months preceding the comments by Yellen and Carney, both outright inflation expectations and the volatility of the prices implied by those expectations have been rising as the implications of Brexit and rising US labour market tightness as well as rising global oil prices has been incorporated into longer-term inflation expectations. We contine to emphasise the benefits of portfolio protection against inflation, which has a sneaky habit of catching investors off-guard.

Source: Bloomberg, pricing from inflation-linked zero-coupon swap (ZCS) market

As we have been cautioning for some time, correlations are rising across both bond and stock markets and the increasingly sudden market reactions to changes in market expectations of inflation illustrate to us the need for specialist strategies designed to respond in a positive fashion to such moves. This is particularly acute for traditional mandate driven fixed income investors given duration is rising across bond indices globally due to increasing long-dated government bond issuance at lower rates.

Long-dated interest rate options which we believe are structurally cheap at present and continuing to capture the persistent relative value arbitrage opportunities between bond and futures markets are some of the strategies that continue to add alpha in these market conditions.

Ardea Investment Management

1. Federal Reserve: (VIEW LINK)

2. Market Watch: (VIEW LINK)

3. BBC: (VIEW LINK)

4. Morningstar: (VIEW LINK)

5. RBA: (VIEW LINK)

The information in this article has been prepared on the basis that the Client is a wholesale client within the meaning of the Corporations Act 2001 (Cth), is general in nature and is not intended to constitute advice or a securities recommendation. It should be regarded as general information only rather than advice. Because of that, the Client should, before acting on any such information, consider its appropriateness, having regard to the Client’s objectives, financial situation and needs. Any information provided or conclusions made in this article, whether express or implied, including the case studies, do not take into account the investment objectives, financial situation and particular needs of the Client. Past performance is not a guide to future performance. Neither Ardea Investment Management (“Ardea”) (ABN 50 132 902 722, AFSL 329 828), Fidante Partners Limited (“FPL”)(ABN 94 002 835 592, AFSL 234668) nor any other person guarantees the repayment of capital or any particular rate of return of the Client portfolio. Except to the extent prohibited by statute, neither Ardea nor FPL nor any of their directors, officers, employees or agents accepts any liability (whether in negligence or otherwise) for any errors or omissions contained in this article.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Established in 2008, Ardea Investment Management (Ardea IM) is a specialist ‘relative value’ fixed income investment manager. Ardea IM’s differentiated pure relative value investing approach offers a compelling alternative to conventional fixed-income investments because it is independent of the prevailing interest rate environment and how bond markets are performing.

Ardea IM believes the pure relative value opportunity set is a proven reliable source of returns because it is driven by structural market inefficiencies that create new relative value mispricing opportunities to profit from. Ardea IM focuses on delivering consistent volatility-controlled returns in order to strictly limit performance volatility and prioritise capital preservation, irrespective of the market environment.

2 topics

Ardea Investment Management

Established in 2008, Ardea Investment Management (Ardea IM) is a specialist ‘relative value’ fixed income investment manager. Ardea IM’s differentiated pure relative value investing approach offers a compelling alternative to conventional...

Expertise

Ardea Investment Management

Established in 2008, Ardea Investment Management (Ardea IM) is a specialist ‘relative value’ fixed income investment manager. Ardea IM’s differentiated pure relative value investing approach offers a compelling alternative to conventional...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management