Do you trust this market?

The ASX200 fell roughly 10% in the financial year just finished, which included a terrifying 35% plunge and euphoric 30% rally in a 16-week period. This loss-making white-knuckle ride is not what investors seek, and has left many on the sidelines feeling cautious and confused.

Investors have a clear choice to make. You can choose to trust this market, however, a market that depends solely on government largesse to go up is not a reliable market. Alternatively, you can choose not to trust this market, and use strategies designed to create their own good fortune - rather than rely on the benevolence of central banks and unsustainable fiscal support to drive a return.

So, ask yourself: Do you have complete trust that this market is behaving fairly and rationally? Or do you think it now more closely resembles a casino? If it’s the latter, you may want to reconsider the options available to you and rethink your strategy for the financial year ahead. We share our perspective here.

The greatest bubble the world has ever seen

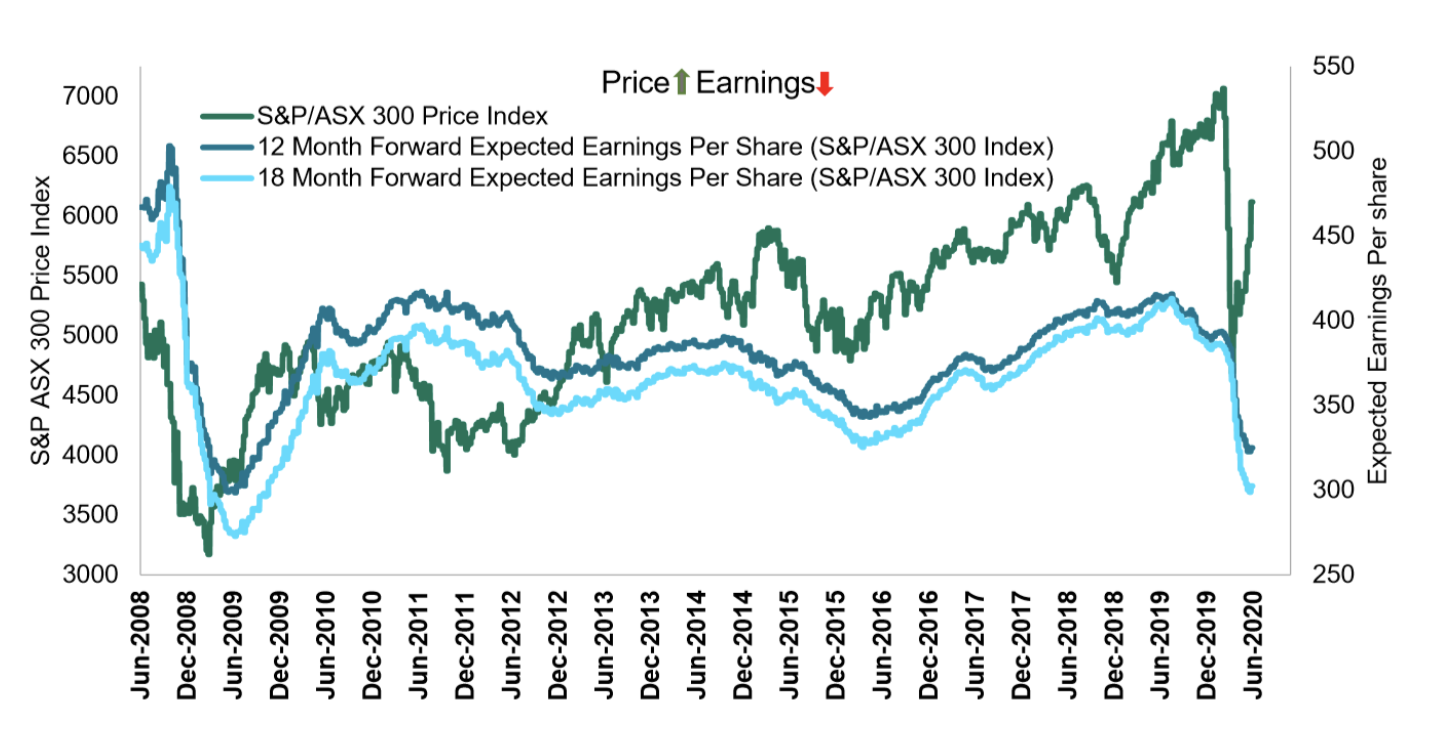

Company earnings projections have fallen off a cliff, with many companies completely unable to predict their future earnings and prospects. Yet share prices have completely ignored these fundamentals and marched ever higher. Considering the severity of the unfolding economic backdrop, what we are witnessing today could quite possibly be the greatest bubble the world has ever seen.

This bifurcation of price and earnings has occurred due to the rather extraordinary and persistent fiscal and monetary stimulus applied by central banks, and the US Federal Reserve in particular.

Source: Refinitiv Datastream, via State Street Global Advisors

No matter what you hear elsewhere or what your superannuation fund wants to tell you, the strongest bull case for equities generally rests on the assumption that through massive money printing and unaffordable fiscal stimulus, governments can hold asset prices at high levels or further inflate them, and that investors will continue to gamble by extrapolating this.

This is highly unlikely to be the case in the long-term as economic reality has always served as an anchor on prices over time historically. Furthermore, unsustainable policies are by definition unsustainable, and will ultimately create great instability in economies and currencies and further wealth dispersion and populist backlash. This could occur unpredictably and much sooner than anyone thinks.

It is important to note that prices are already detached from reality. Volatility is also extremely high, with the VIX index, which is a real-time market index representing the market's expectations for volatility over the coming 30 days, remaining stubbornly elevated. So prices could even break further from fundamentals yet before they start to approximate reality again. In other words, this crazy market could get crazier yet.

In other words, the range of investment outcomes is very high and the nearer-term path uncertain, something which investors should recognise in their chosen approach to investing. Avoiding binary bets is generally essential for good portfolio management and risk management over time

Bigger problems than COVID-19 lay ahead

In an interview with Livewire published at the start of May, Why the bulls are wrong, I argued that the market was overly optimistic on the outlook for COVID-19, saying that:

"I think firstly the bulls are pretending this virus is solved, and that the problem's gone away. The problem hasn't been solved. We still haven't got an effective treatment or an effective vaccine for the virus.”

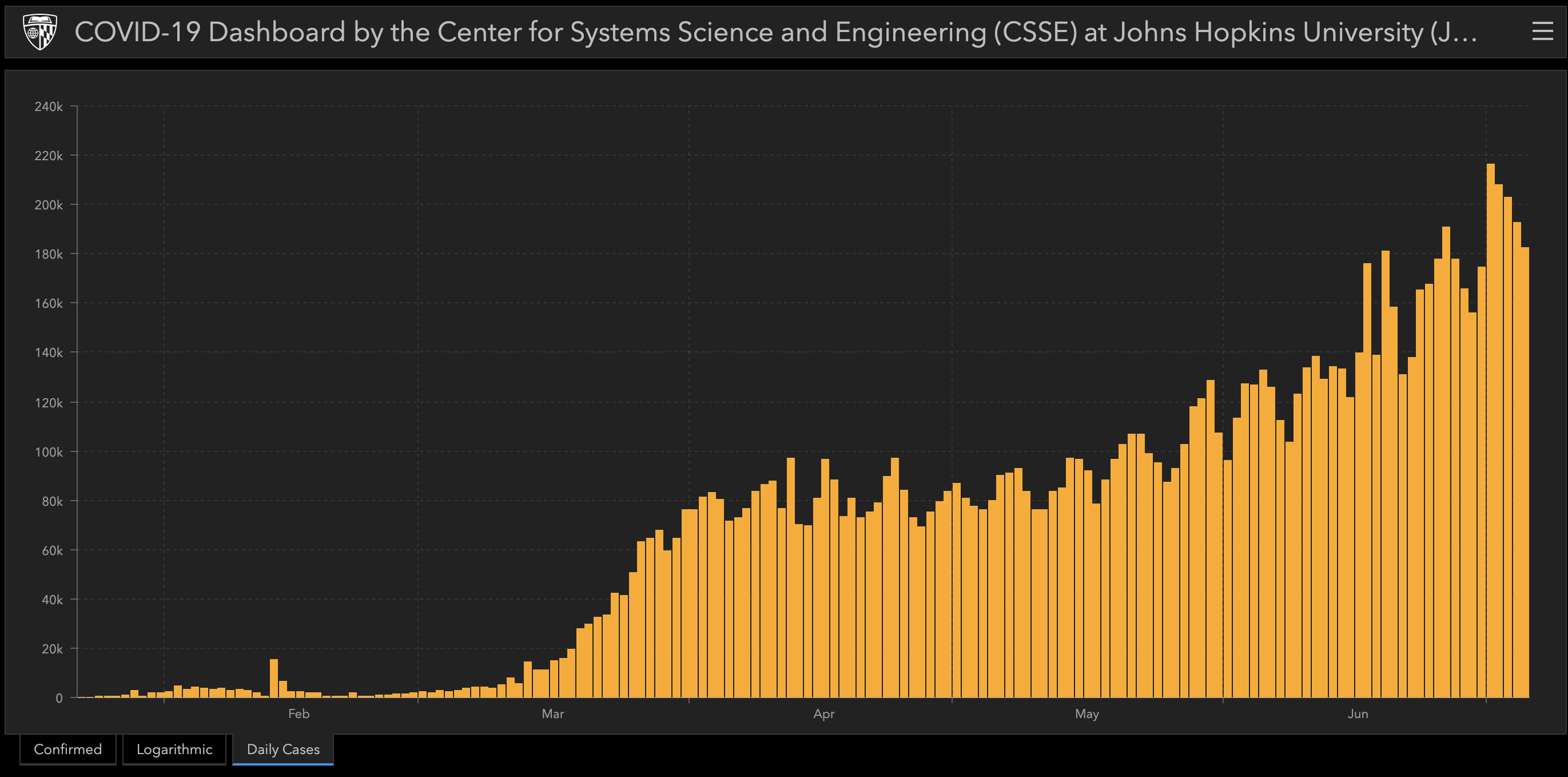

Globally, new cases have been accelerating, and recently set an all-time high of 218,000, led by the US where the virus is completely out of control, causing the return of lockdowns in some States.

Global daily new cases of COVID-19

Source: Johns Hopkins

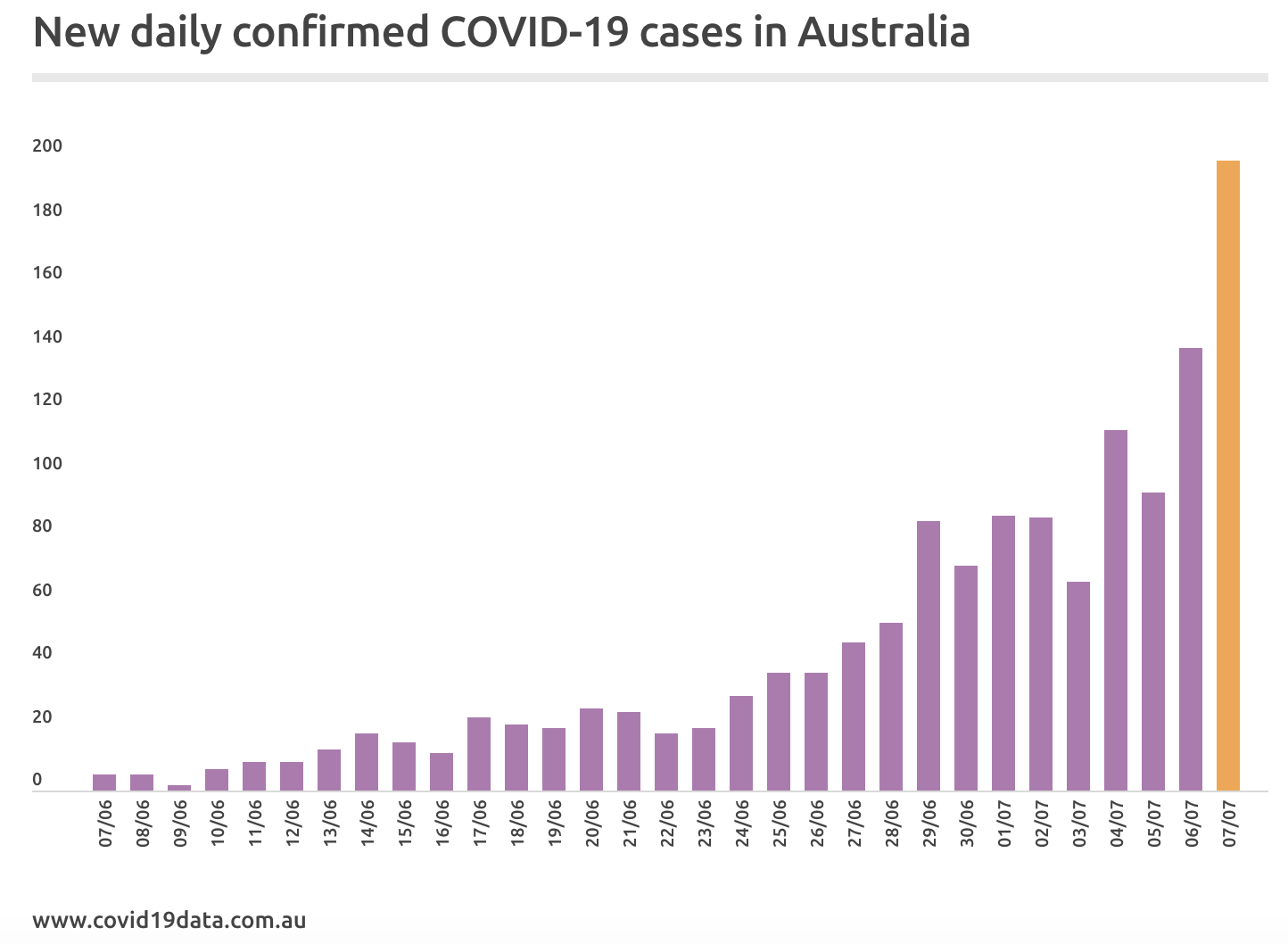

This problem is clearly still very far from solved in the world’s largest economy, just as it is still a challenge here in Australia, with new case numbers climbing rapidly again, the borders between NSW and Victoria closing for the first time in a century and Melbourne heading back into lockdown.

While the market is well aware that COVID-19 will continue to present major challenges, what is less factored in is how the massive and rapidly-growing burden of government debt will weigh on an already fragile economy.

This saddling of future citizens with debilitating debt could be an enduring problem long after the virus is ‘solved’ or mitigated, assuming that occurs. Economies will remain weak as the real reforms necessary to build stronger and sustainable economies simply have not been put in place, and are unlikely to be put in place due to the weak leadership in most Western countries.

Governments are pretending they are the answer, while they continue to dig a bigger hole to bury our economies. We haven’t reformed our economies, and are simply attempting to kick the can down the road yet again. As such, don’t expect to go back to a normal economy any time soon.

These conditions pose a fundamental and ongoing challenge to most investors who are largely invested on the basis that asset prices will go up and that the economy and earnings will grow favourably forever. However, you can’t avoid a hangover forever using extra drinks. Neither can you solve a debt problem with extra debt.

Complex problems need creative solutions

These problems, and others, will greatly challenge index and market-based investment approaches. Crises can be expected to become more frequent and impactful. Investors should be able to sleep well knowing that they’re positioned to perform strongly in all conditions and that they won’t be surprised by renewed selling from this crisis, or when the next market crisis commences. However, complex problems need creative solutions, so what are the options?

Option 1: Continue investing in the ‘traditional’ way

This is the “hope I’m lucky and prices go up” approach taken by most investors. It weights the portfolio heavily to equity risks such as long equities, property, and private equity. A smaller portion of the portfolio is in cash and bonds, which given the low yields and hence lower protection now available will be of little consequence to the overall portfolio result.

The result in the short-term may be binary; either it will be good if equities continue to go up on speculation and prodigious liquidity, or poor if equities fall as fundamental risks reassert themselves.

Medium-term returns could indeed be incredibly poor if inflation returns as the entire portfolio is effectively a gamble on disinflation or low inflation, which is an extrapolation of the economic circumstances we have had in recent years. Furthermore, risk is likely to be higher compared with history as bonds may fail to diversify the equity risks and could instead accentuate them.

Most likely long-term returns will be very low as they become heavily influenced by unfavourable starting valuations, poor economic and earnings outlooks, and are hit by more frequent risk events and market crashes, given the unstable market foundation and fundamentals.

This approach is now entirely dependent on the continuing success of governments at inflating asset prices. Taken alone and in a forward-looking way, this would appear to be imprudent. We can consider using this approach alone to be tantamount to gambling, which means that right now your average super fund and investor is simply gambling on one factor working to produce positive results, perhaps overly confident in the likely success of central banks and governments to keep asset prices inflated.

Option 2: De-risk the portfolio in the ‘traditional’ way

Traditionally de-risking the portfolio means moving more of it to cash and bonds. Many investors have already chosen to do this in response to market conditions. The problem of course is that the long-term return will be negligible and likely negative in real terms due to the financially repressive policies governments have instituted to discourage investors from investing defensively and in order to attempt to keep asset prices elevated.

Cash and bonds are hence now the most unattractive assets available to investors long term as they are almost certain to provide low returns, whereas at least you have a chance with equities to protect your purchasing power!

Bonds themselves have some uncertainty near-term; they may perform exceptionally poorly if inflation rises but could do well short-term if more governments move further into negative interest rate policy, even though it has been ineffective thus far.

The main benefit of these traditional assets is the relative certainty of low rather than negative returns for investors who need their money returned in a short period of time. The other benefit is optionality i.e. the ability to buy something else at a better price later.

Overall, de-risking in the traditional way is very problematic as a long term strategy. It is arguably even more inferior to gambling entirely on equities going up, given central bank policies of financial repression directly impact the future prospects of such a strategy.

Option 3: Invest in genuine diversification with an actively managed multi-strategy approach that’s not heavily market dependent

Investors can choose to look beyond a binary approach of either option 1 above (the fear of missing out on a speculative market rising), or option 2 (the fear of losing money by staying in cash), and ask the real questions here, which should be:

- What are we really trying to achieve?

- What must we avoid?

- How can we think outside the square?

We can then put the investor’s needs first and consider how best to build a portfolio given a realistic assessment of market conditions and all the options available, rather than just the best-known, but least suitable, ones.

Many investors would be happy with relatively consistent high single-digit returns, rather than the ever-present risk of large double-digit losses with their precious capital. A steady 6.5% p.a return quietly doubles your capital in just over a decade, nearly quadruples it over two decades, and does so without giving you insomnia every time a new crisis appears.

In comparison, three years of a more enticing 15% return, that is then followed by a surprise 35% fall like the one we saw in March, actually puts you in the red. In the wise words of Bono, you’re ‘running to stand still’, and are achieving only anxiety and insomnia for your efforts.

A steady solid single-digit return is simply not achievable with options 1 or 2, which is why pension funds globally are now stressing out. The first provides a volatile and uncertain return which could be deeply negative and the second provides an inadequate return and the strong prospect of losses in real terms.

An ideal risk-return outcome can be achieved and directly targeted with a multi-strategy approach that genuinely diversifies a portfolio by combining skilled and complementary active approaches. Such an approach can invest in the best options when they are most likely to work and actively manage market risks to achieve relatively consistent positive results and low drawdowns.

After all, when you think about it, isn’t this the approach that you actually hire a manager to accomplish – to genuinely take away the headaches of large losses, target your actual portfolio goals, manage market risks, achieve diversification and add tangible value?

Over the first full year with our new portfolio management team - in what have been incredibly adverse market conditions for active management - this is essentially what Lucerne Alternative Investments Fund has accomplished. Against a market down about 10% for a financial year that included terrifying volatility, we achieved a strong absolute return in line with our target and saw only small drawdowns. Our strategy aims to keep repeating this kind of result - regardless of what the market throws at us next - providing a proven solution for investors to put their cash to work effectively and prudently, for both today and tomorrow.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's more challenging investment environment. Jerome has achieved net returns for clients of around 20% in both the challenging 2020 year and in 2021, with much lower drawdowns and volatility than Australian equities and hence much superior risk adjusted returns. His Wealthlander Diversified Alternative fund targets double digit returns annually for wholesale clients, with lower volatility and greater consistency than Australian equities, using a diversified multi-asset portfolio approach.

........

Important Notice

This has been prepared by Lucerne Australia Pty Ltd ACN 609 346 581 a Corporate Authorised Representative of AFSL number 481 217 and issued by The Trust Company (RE Services) Limited ACN 003 278 831 as responsible entity and the issuer of units in the Lucerne Alternative Investments Fund. It is general information only and is not intended to provide you with financial advice and has been prepared without taking into account your objectives, financial situation or needs. You should consider the product disclosure statement, available by calling 03 8560 1440 or visiting our website (VIEW LINK), prior to making any investment decisions. If you require financial advice that takes into account your personal objectives, financial situation or needs, you should consult your licensed or authorised financial adviser. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. No company in the Perpetual Group (Perpetual Limited ABN 86 000 431 827 and its subsidiaries) guarantees the performance of any fund or the return of an investor’s capital.

3 topics

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Comments

Comments

Sign In or Join Free to comment