TOL - 8th Jan, 2021

Dogs of the ASX in 2020

The last 12 months have been bruising and emotional for many people, including equity investors. 2020 started with markets rising nicely until late February, based on the assumption of continued strong US economic growth, a second-term Trump presidency (which would be positive for the share market), and robust Chinese demand for Australian exports of minerals, agriculture and services. This benign environment changed sharply when the ASX collapsed -35% in March, as panic selling set in on COVID-19 fears and increasing restrictions from China on Australian exports.

Since the depths of despair in March, the ASX regained its losses (including dividends) as investors stepped in to buy stocks at a fraction of the prices at which they were trading a few months previously. Some were perhaps spurred on by the negative real rate of return now being earned on cash deposits. In addition, high levels of volatility can often create opportunities as the market can be excessively pessimistic as to a company's prospects.

In this week's piece, we will look at the "dogs" of the ASX in 2020, see how 2019 Dogs performed and review how accurate Atlas' predictions were in January 2020.

Dogs of the Dow

Michael O'Higgins popularised a systematic investment strategy of investing in underperforming companies named "Dogs of the Dow" in his 1991 book Beating the Dow.

This approach seeks to invest in the same manner as do deep value and contrarian investors. O'Higgins advocated buying the ten worst-performing stocks over the past 12 months from the Dow Jones Industrial Average (DJIA) at the beginning of the year but restricting the stocks selected to those still paying a dividend. Restricting the investment universe to a large capitalisation index like the DJIA or ASX 100 improves the chance that the unloved company may have the financial strength or understanding of capital providers (such as existing shareholders and banks) that can provide additional capital to allow the company to recover over time.

The thought process behind requiring a company to pay a dividend is that if it is still paying a distribution, its business model is unlikely to be permanently broken. A company's directors are unlikely to authorise a dividend if insolvency is imminent. The strategy then holds these ten stocks over the calendar year and sells them at the end of December. The process then restarts, buying the ten worst performers from the year that has just finished.

Retail investors have an advantage

In Atlas' view, one of the reasons this strategy persists is that institutional fund managers often report their portfolios' contents to asset consultants as part of their annual reviews. This process incentivises fund managers to sell the "dogs" in their portfolio towards the end of the year as part of "window dressing" their portfolio before being evaluated. For example, in early 2019 fund managers with IOOF in their portfolios would have been facing some pretty stern questioning from asset consultants about why they owned the troubled financial services company, as holding IOOF might suggest that the fund manager's investment process or judgement was faulty. However, IOOF's share price recovered by 59% throughout the year to be one of the top-performing stocks on the ASX.

Here retail investors can have an advantage over institutional investors, picking up companies whose share prices have been under pressure late in the year that could see a rebound when the selling pressure stops in January and February. Furthermore, retail investors can afford to take a longer-term view on the investment merits of any particular company that may have hit a speed bump.

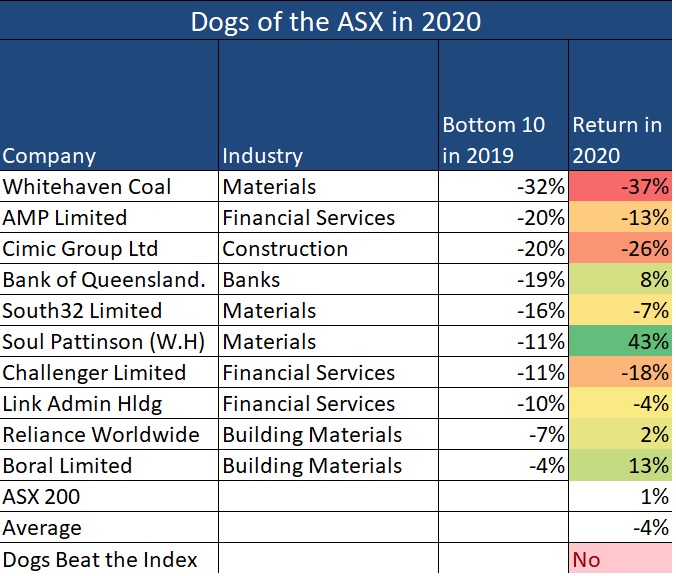

Over the past year, the Dogs from 2019 returned -4%, slightly underperforming the ASX 200 index's return of 1% in what was an extraordinary year. 2020 also marks the first year since 2015 that the Dogs of the ASX have trailed the ASX 200. Global equity markets in 2020 were mostly unreceptive to a company turning around its fortunes.

Continued underperformance from AMP, Whitehaven, Challenger and CIMIC outweighed the recoveries in the share prices of Soul Pattinson, Bank of Queensland, and Boral. The common theme in the reversal of performance in 2019's "Dogs of the ASX" is an improvement in the company-specific issue weighing on the share price. Soul Patts shrugged off the falls in the thermal coal price and focused on gains elsewhere in the company, namely the merger between TPG and Vodafone. Boral rallied on news of a potential takeover by the Seven Group and asset sales in the USA in bricks and plasterboard. Conversely, volatile markets continued to deliver pain for AMP, with CIMIC surprising shareholders with a write-down to exit a largely forgotten business in the Middle East. Whitehaven's troubles continued in 2020 with weakness in coal prices. Similarly, record low-interest rates impact the attractiveness of Challenger's annuity investment products.

Predictions from January 2020

When we went through this exercise in January 2020 looking at which of the Dogs of 2019 would shine in 2020, Atlas considered that the pain would likely continue for both AMP, Whitehaven Coal, Challenger and Boral, mostly correct predictions. In the case of Boral, we underestimated the decisive moves to rationalise the company's diverse US operations and did not account for Kerry Stokes' Seven Group buying 19.9% of the company.

Less successful were our views that both Link and CIMIC would bounce back in 2020. CIMIC's share price weakness in 2019 was caused by a short seller's report that questioned its accounting practices. However, their issues in 2020 were not caused by Covid-19 but rather costs to exit the Leighton’s Al Habtoor joint venture in the Middle East. Link Admin performed roughly in line with the market as significant falls in the company's share price in the first half of the year were offset by a takeover offer in October.

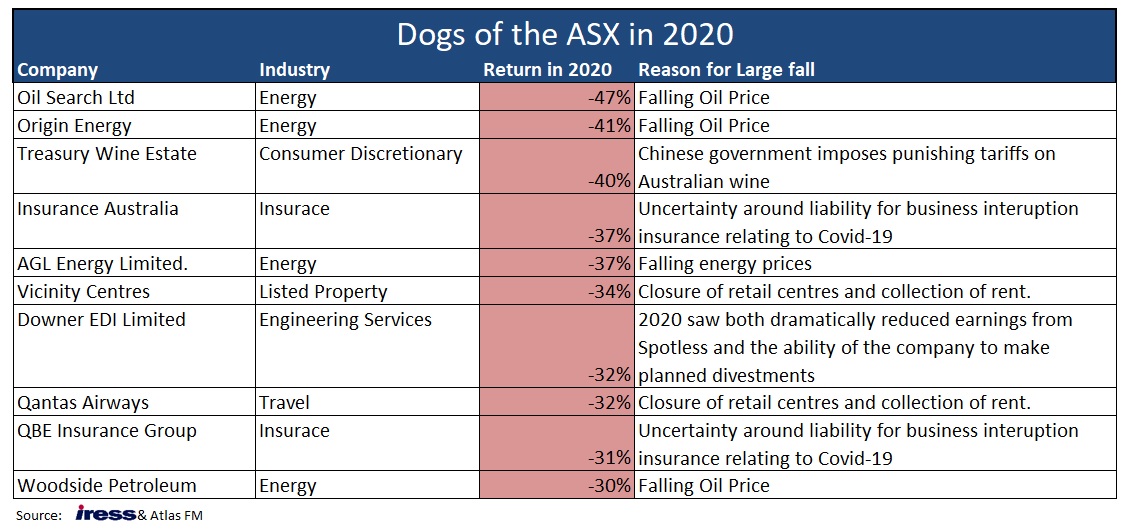

Unlike previous years, the list for 2020 is more concentrated in a few sectors – namely energy and insurance – reflecting industry-specific issues relating to Covid-19 causing underperformance, rather than more easily fixed company-specific problems.

Qantas and Treasury Wines have been strong performers in previous years and are leaders in their respective fields and in more normal markets both would be picked as candidates for a bounce in 2021. However, both companies are likely to face continuing pressure in 2021. The reasons for their falls in 2020 have been travel bans and punitive Chinese government tariffs on Australian wine respectively, and the resolution of these issues are beyond the control of the two companies' management teams. Insurance companies IAG and QBE are benefiting from sharply rising premiums, but face lower investment income from low-interest rates and uncertainty over whether business interruption policies written with pandemic exclusions apply to COVID-19 related claims.

Looking at the underperformers' list for 2020 in the ASX 100, the key theme impacting their share prices are falling energy prices.

January saw oil at US$66/bl: roughly in the mid-point of the US$65-75 range at which the commodity has traded between over the last five years. The COVID-19 crisis saw a very sharp decline in global demand for crude oil as 70% of global petroleum consumption is used in the transportation industry, and suddenly airlines were grounded and motorists quarantined. Further downward pressure was placed on the oil price in early 2020, as Saudi Arabia and Russia entered into a price war in March, flooding global oil markets with additional supply when demand was already falling sharply. These factors saw global oil prices fall below US$20/bl, though at the central US storage hub in Oklahoma in late April the oil price hit negative US$37/bl with sellers paying buyers to take oil off their hands as the storage facilities were mostly full. All energy companies lack a real ability to influence world oil prices and saw their share prices fall in step with the underlying commodity.

Looking through the list of the Dogs of 2020, it is harder this year than at any time over the past decade to select which poor performers from the past year will shine in 2021, as Covid-19 has created an additional level of uncertainty. Despite this grim outlook, historically there has always been between one and nine stocks on the annual list of the ten Dogs of the ASX that have outperformed significantly in the following year.

From the above list, Atlas sees that prize pooch for 2021 is likely to come from the energy sector. Already over the second half of 2020, the oil price had rallied to US$52/bl. Among these companies, we prefer Woodside over Oil Search and Origin Energy due to Woodside's lower cost of production and lower gearing.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

........

This document is issued by Atlas Funds Management Pty Ltd. Atlas Funds Management Pty Ltd is not providing any general advice or personal advice regarding any potential investment in any financial products within the meaning of section 766B of the Corporations Act. No consideration has been made of any specific person’s investment objectives, financial situation or needs. The provision of this presentation is not and should not be considered as a recommendation in relation to an investment in any entity or that an investment in any entity is a suitable investment for any specific person. Recipients should make their own enquiries and evaluations they consider appropriate to determine the suitability of any investment (including regarding their investment objectives, financial situation, and particular needs) and should seek all necessary financial, legal, tax and investment advice. Atlas Funds Management Pty Ltd, it’s directors and employees do not accept any liability for results of any actions taken or not taken on the basis of information in this presentation, or for any negligent misstatements, errors or omissions. This presentation is not an advertisement and is not intended for public use or distribution. Past performance of a fund is no guarantee as to its performance.

3 topics

6 stocks mentioned

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Comments

Comments

Sign In or Join Free to comment