Don is good for Aussie housing

"I like thinking big. I always have. To me it's very simple: if you're going to be thinking anyway, you might as well think big." – Donald J Trump. The world has been mesmerised by The Don this week with mixed reactions and outlooks hitting our desk. Will Trump go on a spending spree to "rebuild America" which will stimulate the economy, lift inflation and lead to a sell-off in bonds? This would signal a further rotation into growth stocks. Or will he create enough uncertainty and upset so many people that confidence wanes and growth stutters? Could we be faced with a real life version of the classic sci-fi movie Dawn (Don) of the Planet of the Apes where humanity struggles to stay alive? 24 hours into his elected Presidency it seems that it's a risk on environment favouring growth stocks.

Pat Barrett

UBS Asset Management

What does it mean for AREITs?

As previously written, defensive assets will likely underperform in a growth environment. This trade is occurring purely on the back of expectations, as real global growth has not yet occurred nor have US interest rates actually risen! AREITs will theoretically struggle in this environment for the short term until economic growth kicks in, businesses make more money and have more capacity to pay higher rents which leads to higher earnings growth for REITs and other defensives. Never mind that the world is suddenly an even more volatile place and that we have upcoming elections in Italy, France, and Germany. There could be absolute chaos in Europe, and despite the "smart money" rotating into growth, I believe that stocks delivering 9–10% IRR are very appealing. Some AREITs are now trading back near NTA levels, which is a traditional signal for buybacks.

This uncertainty has one unintended benefit, and that is Australia is seen as a relatively safe haven. While our immigration website did not crash like Canada and New Zealand, we are a very attractive and isolated place. International investors will be attracted to our relatively stable government, security of title and an attractive FX rate. Channel checks with foreign capital suggest that their appetite for Australian commercial real estate has not been diminished by The Don. Indeed, a few signalled that Australia would be even more attractive given potential electoral issues in Europe next year. In terms of housing, and given the strong Clinton vote in the US West Coast, don’t be surprised to see some US citizens bidding at upcoming residential auctions.

Hong Kong taxes

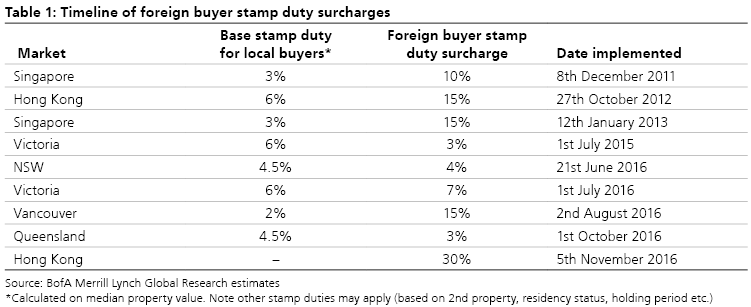

Further helping Australian housing attractiveness is Hong Kong's imposition of further stamp duty such that non-first-time HK resident buyers will pay 15% and non-HK buyers will buy 30%. This applies to residential properties only. This new measure should curb investor demand, particularly for small-sized units as transaction costs will be significantly higher. Compounding Hong Kong's woes is the fact that their retail sales declined for the 19th straight month in September as China's economic slowdown and relatively strong local currency impacted business activity and mainland tourism. Mainland Chinese are apparently flying straight to Paris, London, etc. to shop.

There are now four countries that have introduced additional stamp duties for foreign buyers of real estate – Australia, Hong Kong, Singapore, and Canada (Vancouver). In all cases, these surcharges have been implemented in response to a perceived surge in demand from offshore investors, coupled with accelerating house prices. In Australia, there are three states where stamp duty surcharges have been implemented (for foreigners) – Victoria (7%), New South Wales (4%), and, most recently, Queensland (3% from 1st October '16).

The recent adoption of a stamp duty surcharge for foreign buyers in Vancouver has attracted heightened media attention, including reports that sales volumes have slumped 30% since the tax was introduced, and that foreign buyers have exited the market entirely. However, locally, we have seen limited evidence that increasing stamp duties have had a significant cooling effect on the housing market, either from the perspective of offshore buyer activity in Australia or across the market in general.

Elsewhere, sales of new condominiums in Tokyo have fallen to the lowest since the nation’s 1990s property bubble collapse, according to data from the Real Estate Economic Institute. Stagnant wages are blamed for the decline in potential purchasers, despite 35-year fixed-interest mortgages as low as 1.06%. It all adds up to be positive for Australian residential real estate.

Written by Pat Barrett, Property Analyst, UBS: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Pat Barrett has twenty five years experience in the listed and direct property industries, most recently covering property securities, infrastructure and utilities analysis at UBS.

3 topics

Pat Barrett

UBS Asset Management

Pat Barrett has twenty five years experience in the listed and direct property industries, most recently covering property securities, infrastructure and utilities analysis at UBS.

Expertise

Pat Barrett

UBS Asset Management

Pat Barrett has twenty five years experience in the listed and direct property industries, most recently covering property securities, infrastructure and utilities analysis at UBS.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management