Don't Dismiss Deflation: Implications for Real Yields and Risk Assets

Chamath De Silva

BetaShares

So much of asset pricing hinges on selecting an appropriate discount rate, which is how we transform future cash flows into a value today. In fixed income we have the metric of duration, which can approximate price movements to yield changes, but discount rate sensitivity applies to risk assets also, especially perpetual cash flow streams like equities and real estate. Real cash flows (i.e. inflation-linked) should be discounted at real rates (i.e. inflation-adjusted), which should consist of a real risk-free component (e.g. the yield on a long-term inflation-linked government bond) along with an appropriate risk premium (capturing, for example, volatility in the risk-free benchmark, credit spreads and credit spread volatility on equivalent corporate bonds, along with other capital structure risks and cash flow variability).

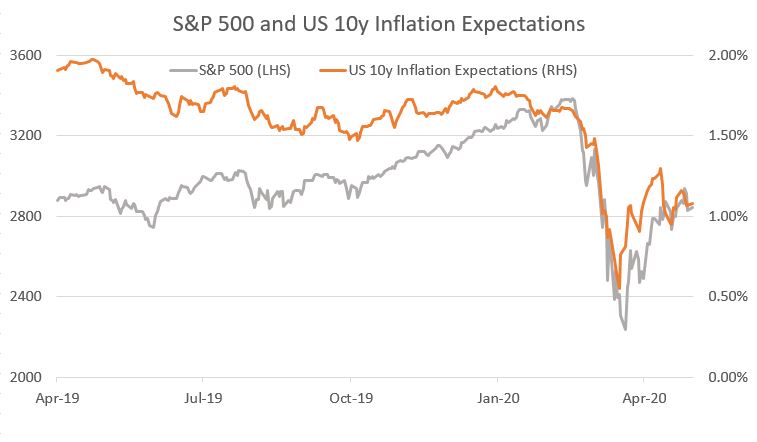

COVID-19 has created both a demand and supply shock, but whether inflation or deflation dominates is a question I’ll leave to the economists. Instead I’ll focus on the consequences of deflation on real yields and asset prices. With nominal cash rates, policy rate expectations and much of the nominal yield curves in the developed world pinned around the zero-lower bound, it’s likely going to be inflation expectations that drive real yields over the next few years. Over the past 12 months, arguably the most discount rate sensitive broad equity index of all, the S&P 500, has begun to broadly move in line with 10-year US breakevens (inflation expectations implied by the spread between nominal Treasuries and TIPS, Chart 1). With nominal US and Australian bond yields so low (and likely to face difficulty breaking below zero without policy rate expectations moving first), the risk now is a deflationary impulse sending real yields higher, which would have significant negative implications for risk assets, including those that have benefited from the secular disinflation of the past 30 years.

Chart 1: S&P 500 and US 10-year Inflation Expectations (breakevens); Source: Bloomberg

Disinflationary growth vs a deflationary recession

The secular forces of demographics, technology and globalisation have arguably driven not only headline rates of inflation lower, but also inflation expectations and term premiums on real yields. A world of disinflationary growth (albeit slowing in real and nominal rate of change terms) is an ideal environment for most financial assets if central banks have monetary space to take nominal and real rates lower to counter economic shocks. Indeed, the benefits of a lower discount rate can potentially offset a slowing rate of change in cash flow growth to still produce outsized real and nominal total returns for equity investors. This is largely what we’ve seen, and as investors flocked to growth stocks as growth increasingly becomes scarce in the global economy, broader market cap weighted indices have reflected this secular trend. The S&P 500 is now heavily skewed towards technology and the MSCI World is tilted towards the US.

However, once conventional monetary space is exhausted and QE is increasingly seen as ineffective at stimulating the real economy, deflationary expectations can become entrenched across longer maturities, sending long term real yields higher. The extent to which rising real yields hit equity multiples will likely depend on how the credit market behaves in a deflationary environment. Historically, deflation hasn’t always been bad, and the developed world has experienced periods of deflationary growth, such as in the late 1800s and 1920s in the United States as technological progress drove productivity booms. However, if an economy is highly indebted, deflation can have adverse outcomes for shareholders.

With corporate balance sheets highly leveraged today, a deflationary shock risks creating a negative spiral through both a rising real value of debt outstanding and higher real interest rates on refinancing, triggering forced deleveraging and asset sales. Management decisions to aggressively de-risk balance sheets and build buffers could mean stock buybacks and dividend payouts make way for capital raisings and dividend cuts. If balance sheet resilience takes precedence over efficiency, the balance of power shifts away from shareholders to bondholders, resulting in less equity participation in the eventual economic recovery.

Fortifying portfolios

As market cap equity indices have developed a profile over time that is more suited to disinflationary growth, they become more vulnerable to an outright deflationary recession. Despite higher credit spreads providing a greater margin of safety than at the start of the year, much of the corporate credit market is still unlikely to perform well in a deflationary environment, given the overall deterioration in credit quality of the global universe and high levels of debt outstanding. Instead, it’s the lowest yielding haven assets that will likely provide the best protection during such a cycle: cash, nominal government bonds and the highest tiers of fixed-rate investment grade during the initial deflation; gold to protect portfolios from the policy response to the deflation.

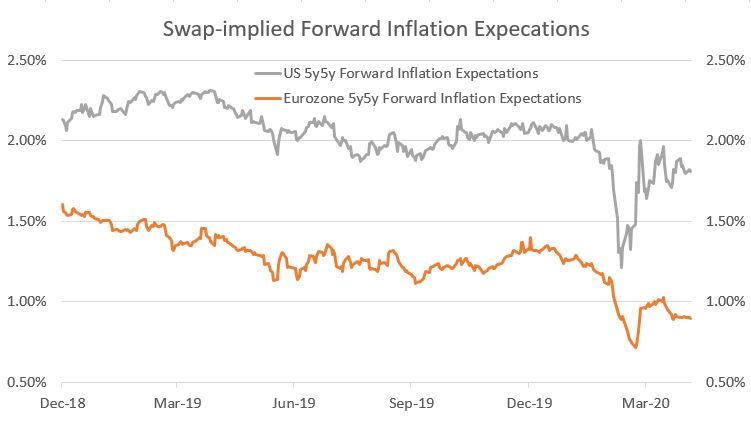

It’s easy to think that the unprecedented size of the global fiscal and monetary stimulus may prove to be inflationary, but breakeven and forward inflation swap markets (Chart 2) are expressing doubts about this. It’s also easy to think that accommodative central banks will provide a floor for equity prices. However, equity investors shouldn’t forget the fundamentals of where they sit in the capital structure. A bet on equities is a bet on credit: the bond holders must be paid and there needs to be enough residual free cash flow to justify the price when discounted at an appropriate real rate. If we’re in a world where real risk-free yields, default risks and the equity risk premium are all increasingly sensitive to inflation expectations and if all this policy stimulus fails to spur it, trouble could ensue for long duration real assets.

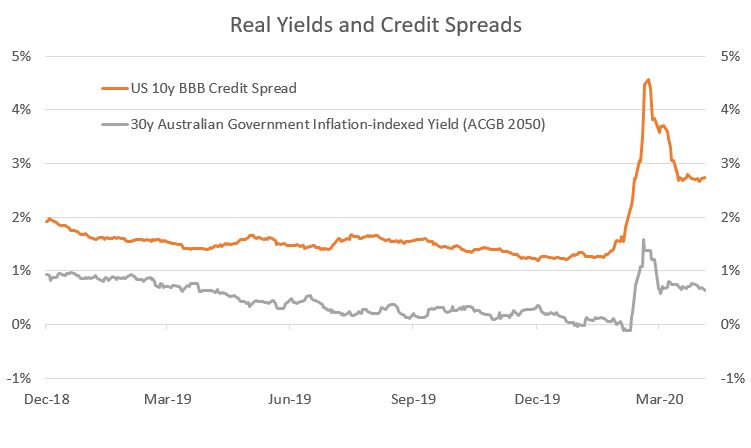

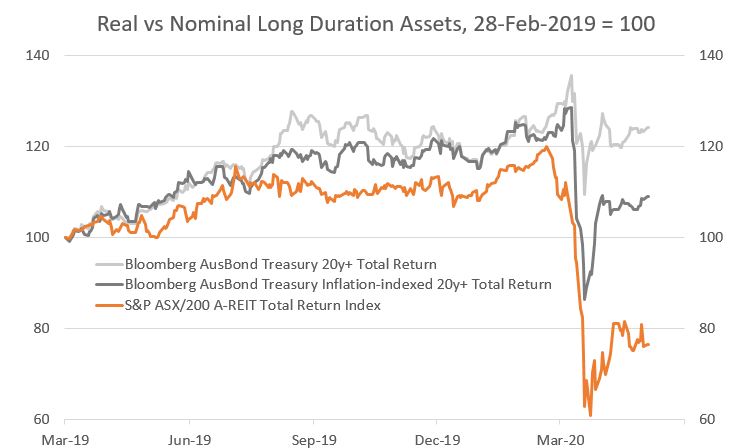

One under-reported aspect of the March chaos was the spike in long-term domestic real risk-free yields as inflation expectations collapsed (with inflation linked government bond prices falling sharply, Charts 3 and 4) alongside a surge in global credit spreads, which on their own should have sent equity multiples plummeting irrespective of the earnings outlook. Real yields and credit spreads matter and equity investors should acknowledge the implications of deflation, even if it isn’t the base case.

Chart 3: Real Yields and Credit Spreads; Source: Bloomberg

Chart 4: Nominal and real long duration assets; Sources: Bloomberg, BetaShares Capital

This information has been prepared by BetaShares Capital Limited (‘BetaShares’) (AFSL 341 181; ABN 78 139 566 868)

The information provided is not a recommendation or offer to make any investment or to adopt any particular investment strategy. Readers should make their own professional assessment of the suitability of such information, relying on their own inquiries.

Future results are impossible to predict. This information may include opinions, views, estimates, projections, assumptions and other forward-looking statements which are, by their very nature, subject to various risks and uncertainties. Actual events or results may differ materially, positively or negatively, from those reflected or contemplated in such forward-looking statements. Forward-looking statements are based on certain assumptions which may not be correct. You should therefore not place undue reliance on such statements. BetaShares does not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date such statements are made or to reflect the occurrence of unanticipated events.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Responsible for the portfolio management function and fixed income product development at Betashares. Previously, Chamath was a fixed income trader at the RBA, working in their international reserves section in Sydney and London.

Featuring

Chamath De Silva,

BetaShares

Responsible for the portfolio management function and fixed income product development at Betashares. Previously, Chamath was a fixed income trader at the RBA, working in their international reserves section in Sydney and London.

3 topics

Chamath De Silva

Portfolio Manager

BetaShares

Responsible for the portfolio management function and fixed income product development at Betashares. Previously, Chamath was a fixed income trader at the RBA, working in their international reserves section in Sydney and London.

Expertise

Comments

Comments

Sign In or Join Free to comment