TOL - 6th Nov, 2020

Don’t fall for a great story (find great investments instead)

It is not unusual for investors to be captivated by emerging technology but for Ted Franks from the Pengana WHEB Sustainable Impact Fund, the COVID-19 crisis has first and foremost highlighted the benefits of long-term investing.

WHEB has accordingly designed its process to limit the chances of falling for the ‘great story’. The fund invests exclusively in companies which produce goods and services to address the challenges of sustainability. These are the companies which are solving or averting the problems of tomorrow and catching the positive tailwind associated with businesses that experience growth associated with more sustainable outcomes.

Underpinning this is a focus on nine sustainable investment themes — five environmental and four social — which represent parts of the market that will have superior long-term growth prospects as they address underlying structural trends in the global economy.

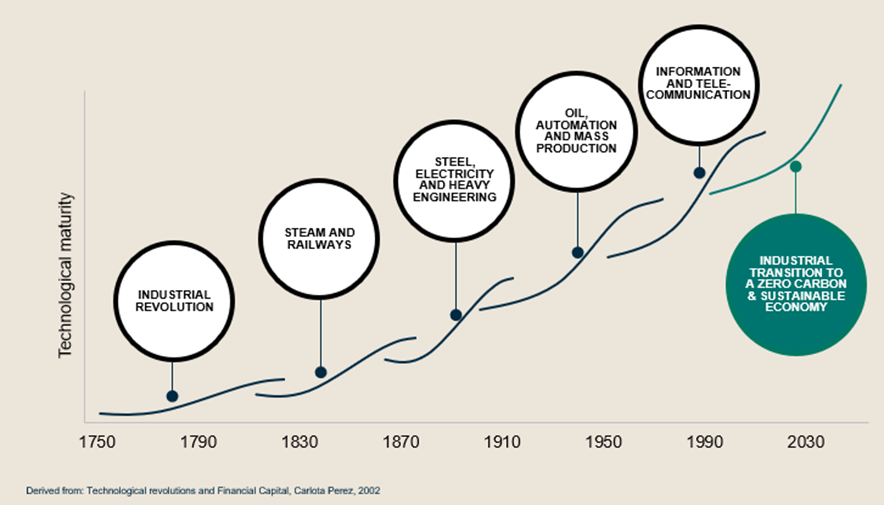

You’ve previously opined that impact investing offers the opportunity to access the ‘6th Industrial Revolution’. Can you explain what that means, and the opportunity presented by impact investing for investors looking at your fund today?

The 6th industrial revolution refers to the next wave of economic advancement associated with the transition to a sustainable economy. Previous revolutions were largely predicated on existing technologies and unconstrained factors of production. We now live in a world of almost 8 billion people, more than double the population that existed when the last revolution was taking hold. Resource constraints and environmental risks are forcing the emergence of more efficient technologies and industrial processes, which result in better social or environmental consequences as they are implemented and adopted.

The Pengana WHEB Sustainable Impact Fund exclusively invests in companies which produce goods and services to address the challenges of sustainability. These are the companies which are solving or averting the problems of tomorrow and enabling the 6th industrial revolution, and naturally there is a positive tailwind associated with businesses which experience growth associated with more sustainable outcomes.

One facet about global markets you criticised back in 2019 was the rise in short-term trading. This trend has accelerated with COVID-19 and the rise of trading apps like Robinhood. Can you provide a fresh view on this topic and the risk it’s creating in global markets?

Really short-term investors typically buy stocks on the back of positive sentiment or momentum or look to trade on news flow. Those with shorter-term horizons are usually looking for catalysts to propel stocks higher, for example the next set of results, a regulatory approval, or a news release. Periods of high volatility can encourage this. Ironically, many shorter-term investors extol the benefits of ESG analysis. At a company level, the impact of ESG practices and policies tend to manifest only over time.

However, the crisis has also highlighted the benefits of long horizon investing. Ultimately, company fundamentals prevail and detailed analysis incorporating ESG analysis provides important information about the long-term investment prospects. WHEB’s strategy has structural exposure to trends, which we think will benefit over the coming decades from the transition to a more sustainable economy. But the path of such trends is never smooth, and crises such as the current pandemic can lead to a sudden acceleration of change. As longer-term investors we are also inclined to focus on higher quality businesses, and we expect them to be more resilient in difficult times, protecting shareholder value as a result.

How do you define your investment universe?

WHEB’s investment universe broadly consists of high-quality companies that provide solutions to critical environmental and social challenges confronting society. It is then refined to a focus on nine sustainable investment themes — five are environmental and four social themes.

We have selected these nine themes because we believe they represent parts of the market that will have superior long-term growth prospects as they address underlying structural trends in the global economy. Examples include, resource scarcity, an aging population, and rising populations and living standards. Finally, we hone-in on the most impactful companies, evaluating the dimensions of the positive impact they generate with reference to factors including the uniqueness of the product, the vulnerability of the client and how critical the impact is. All of this information is captured and shared openly with our investors.

You’ve said that there’s a difference between a ‘great story’ and a ‘great investment’. How do you capture this risk?

It is not unusual to be captivated by an emerging technology and believe it has world-changing potential. But things are often more complicated than they initially appear and the road to scale and commercialisation is bumpy and twisted. We have accordingly designed our process with inbuilt mitigants to limit falling for the ‘great story’. The first mitigant is to avoid companies that are either not listed on a main board exchange or which have a market capitalisation of less than US$200m. Secondly, we only invest in profitable companies. These criteria are generally associated with proven technology and established business models, and our investors are accordingly more exposed to growth risk during the period of adoption rather than the risk of technological failure. At a portfolio level, we have a mid-cap focus with only a very small proportion invested in sub-US$1bn companies.

Quality and valuation are also key. We regularly search for companies with attractive and consistent returns and profitability, a track record of steady growth, low leverage and above average ESG attributes. We will only invest in those companies if the valuation is reasonable on both a longer-term basis as well as compared to other companies in their peer group.

Hydrogen is a good example where many have recently failed to distinguish between a good story versus a good investment. During Q2, the stock price of hydrogen-powered car company Nikola shot upon the back of frenzied speculation and dragged other listed hydrogen plays along with it. These companies are all loss-making and are expected to be so for several years yet. In the third quarter, this momentum waned, and their share prices slumped. Further, looking across investment opportunities for green and blue hydrogen, we have found very few investable companies so far. Some are too small. Others are heavily loss-making and not yet commercialised.

We believe that the best way to gain exposure to exciting but emerging themes is by investing at reasonable valuations in profitable and established companies which already have a footprint in the space. Our investee company Linde is the largest industrial gas company in the world. It enables downstream clients to substantially reduce their own carbon emissions (achieving a net avoidance of 62.5 million tons of C02e in 2019). Linde is about to begin construction on the world's first hydrogen refuelling station for passenger trains in Germany. It also recently formed a partnership to build a 10MW green hydrogen production facility in Glasgow, which aims to supply hydrogen to the commercial market within the next two years.

Has COVID-19 created, or accelerated, any new opportunities within the impact investing universe?

As the demand from industry, travel and transportation dried up, one of the most dramatic features of COVID was the collapse in the oil price and the drastic underperformance of oil stocks which had already been under pressure for some time. Perhaps the starkest illustration of this was Exxon Mobile’s removal from the Dow Jones industrial Average after 92 years in the index.

By contrast, we have continued to see an acceleration in the rate of electric vehicle adoption. We hold a number of world class companies in our portfolio that benefit from, and enable, this trend. These include TE Connectivity, Norma Group, Adaptive plc, and Infineon technologies, which make components used in electric and autonomous vehicles.

We are also greatly encouraged by the more rapid adoption of renewable energy, stimulated by green recovery plans implemented in many regions and countries around the world. The EU, for example and in response to the pandemic, has proposed a €750 billion recovery plan to repair the economic and social damage with 25% earmarked for green investments. We also have a number of holdings in our health theme that are directly helping to contain and treat the virus. Thermo Fisher Scientific produces a widely used COVID test, Cerner provides critical software to enable efficient record keeping through entire public health systems, and Danaher sells laboratory products to clinical and medical laboratories including microscopes, analytical software and imaging devices. Its products make meaningful contribution in the COVID-19 therapeutic and vaccine development.

A couple of stocks from our safety theme have also contributed positively. Steris provides sterilisation and microbial reduction services to hospitals and other medical businesses as well as for food safety and industrial markets. Its products play a key role in the fight against COVID-19 in the hospital setting. Lastly, in the same theme but during a different crisis, MSA Safety provided a significant amount of safety equipment to our firefighters during the recent bushfire crisis.

FAANG stocks have been a key driver and enabler of commerce during COVID-19 lockdowns, allowing many businesses to operate; providing home entertainment, and connecting people to online shopping. Yet you exclude these stocks from your universe. Can you explain why?

We agree that the solutions enabled by technology companies (including those outside the FAANGs) have allowed business to continue functioning smoothly across companies in general as well as those that we invest in.

Very simply, however, we will only invest in companies whose products and services are providing a solution to a sustainability challenge. Every dollar of additional advertising revenue generated by Facebook and Alphabet/Google, and every new Netflix subscriber is not solving an environmental or social issue raised by resource scarcity, an ageing population or rising living standards.

On a personal note, the key driver of Apple’s business is a continuous attempt to persuade my teenage son to upgrade his iPhone/MacBook/Apple Watch (again!) each time a new iteration is released. While Apple is becoming increasingly better at conducting their business in a sustainable way (for example, by using smaller and recyclable packaging), that is really just an increased focus of operations on ESG compliance.

There is no lockstep relationship between unit sales growth and positive environmental and social outcomes.

Apple is not enabling the transition to a more sustainable economy, rather their growth is ultimately driving increased product (resource) consumption, which is part of the problem. This is why our focus on investing solely in positive impact companies has been a cornerstone to our investment strategy and process since 2006, and our adherence to it provides our investors with comfort that the fund is not subject to greenwashing.

How would you differentiate yourself from other managers using ESG or ethical labels?

We have a holistic approach to sustainability, considering both social and environmental themes. This means we have a more complete view of the long-term challenges and opportunities a company faces, and our portfolio is diversified compared to other more narrowly focused thematic funds as well as to the broader market. We also only invest in companies which provide a solution to a sustainability challenge – we are disciplined and transparent about applying this definition and therefore less likely to suffer the charge of ‘greenwash’ from our investors.

Sustainability is ‘built in’ to our investment strategy as a source of investment return, rather than ‘bolted-on’ as a modification of another investment approach. We consider how a company addresses ESG risks and opportunities as an integrated part of our investment analysis (rather than as an overlay or screen) and believe that this gives us a competitive edge in identifying high quality investment opportunities.

We believe we are also differentiated in terms of best practice industry standards that we pioneered which can now be seen across industry leading peers globally. We were the first listed equity strategy (team) to publish an annual impact report, and continue to be widely regarded as a leading proponent of impact investing in listed equities. The investment team (WHEB) itself is also certified as a B Corporation and structured as a partnership, which enables and incentivises us to make longer term business decisions, and focus on the interests of our clients via a unique emphasis on transparency and governance (for example, we publish our holdings and investment advisory committee minutes).

What’s your favourite investment right now and how is it making an impact?

We are really excited by our investment in Strategic Education, which we initiated in April this year. It is a for-profit higher education provider in the US, which has historically been a controversial area because of perceived poor value-for-money for the students. But Strategic is in a different category: it has consistently excellent quality and value results in its two US institutions, Strayer and Capella Universities, and has always had good relationships with the Department of Education.

But it is a lot more than just the quality operator in a low-quality sector though. Firstly, Strategic is very impactful because it focuses on underserved populations. For example, Strayer’s student cohort is 70% female, and 70% black. Further, it builds its offering to support these students for whom higher education ambitions often sit alongside significant work and family obligations. From a historic position of leadership in distance learning, with Capella, it has built into a distance specialist, and has rapidly reduced the footprint of its physical campus.

The flexibility remote learning offers suits its students, so it has developed some of the best digital tools in the industry, including using AI to identify vulnerable students early and offer them additional support. It has also developed the “Flexpath” system to allow students to better control how they achieve their degrees, by either taking more modules when they have the time, or fewer when they don’t.

In a year in which a lot of impactful stocks have stretched their valuations, Strategic Education is also something of a value opportunity. With a net cash balance sheet, it trades on under 15x 2020 earnings, which in current US stockmarket conditions almost counts as deep value. Part of this is the perception that a Democratic administration would be bad for the sector. It also relates to negative sentiment against the cost of its recent acquisition of Torrens University in Australia and the Design and Media School in New Zealand.

We anticipate that both of those institutions will benefit from Strategic’s ownership and the acquisitions will be validated; we also think that sentiment will steadily improve as the US political situation is resolved, and the company demonstrates steady execution on its thoughtful digital plans.

Learn more

Click here to visit the Pengana WHEB Sustainable Impact Fund Profile to learn more about the fund, fees and performance.

Click here to visit the Ted Franks Contributor Profile, to discover his investment philosophy and content.

To view the Fund's Impact Reporting tool, please click here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life.

Patrick was a Market Analyst, Editor, Senior Editor, and Managing Editor at Livewire Markets between 2015 and 2022. He was the Content Director and a member of the Investment Strategy & Research Group at Betashares between 2022 and 2024. He is an expert on listed products, commodities, and investment strategy, with a particular interest in gold and uranium,.

Featuring

Ted Franks,

Pengana Capital Group

Ted is the Fund Manager for the Pengana WHEB Sustainable Impact Fund and helped to found WHEB Asset Management in 2009.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

5 topics

1 fund mentioned

1 contributor mentioned

Patrick is the founder and director of PLP Finance Media, a content production and strategy consulting agency specialising in investment content and communications. He also writes for A Rich Life. Patrick was a Market Analyst, Editor, Senior...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Consequences of capital flows can't be ignored

ClearBridge Investments

Property

The property market’s next big moment is already underway

Livewire Markets