Don’t fear negative yielding bonds in a portfolio

High grade sovereign (or government) bonds remain as relevant as ever in an uncertain and complex market environment. Today’s bond yields are indeed low, and some investors may be finding it difficult to justify a portfolio allocation to high grade bonds. However, research and experience shows that in periods of market stress, the inclusion of high grade bonds in a portfolio can provide investors with the opportunity for balance given their defensive characteristics, the mitigation of risk through low correlation with risk assets, and relatively robust returns over time.

In current times, Central Bankers’ range of liquidity and accommodation measures in response to COVID-19 have undoubtedly been enormous, most notably, a number of policy makers have chosen to cut their policy rates to even lower levels (including the U.S., Canada, U.K. and Norway). And, of course in Australia, policy rates have fallen to 0.25%. With the RBA’s target cash rate reaching historical lows, many multi-asset investors are questioning the role of high grade bonds in portfolios – that is, how much more can yields fall and can they still be relied on as a defender against risk assets?

High grade bonds have historically diversified against shares

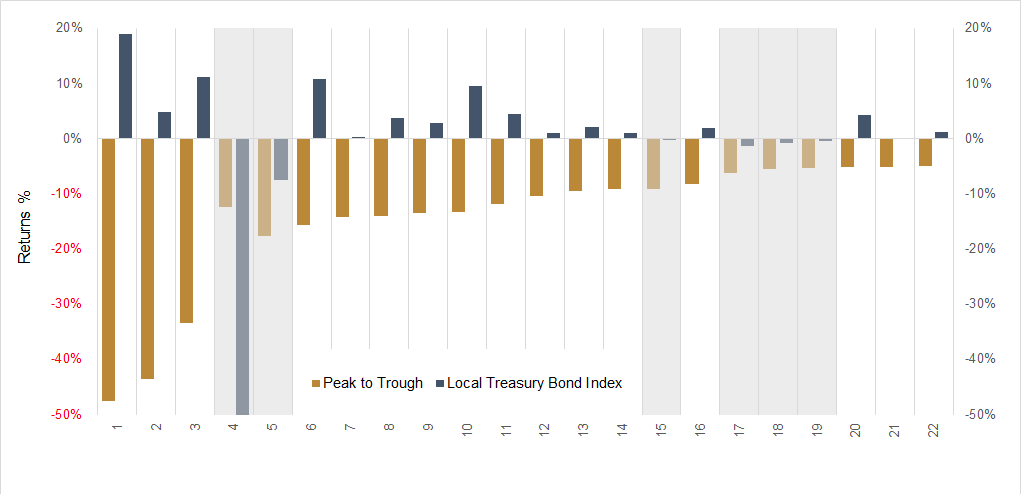

Australian high grade bonds have proven to be effective diversifiers for balanced portfolios, especially during stressed market environments. A look at the history of Australian shares and their drawdown episodes since 1976 shows there have been twenty-two (22) such cases, since 1976. With five (5) material equity market drawdowns in each decade, the cushioning effect of high grade sovereign bonds (represented by the Bloomberg AusBond Treasury Bond index) is evident throughout this time.

Chart 1. Australian high grade sovereign bonds have played an effective role in cushioning the impact of share market drawdowns.

Maximum Australian share market drawdowns and Australian Treasury Bond Market performance, 1976 to July 2020.

Source: JCB team analysis, using data sourced from Bloomberg.

While it’s true that high grade sovereign bond returns aren’t spectacular relative to growth assets, their role as a diversifier and counterweight to major falls in the Australian share market is. In all of the 22 share market drawdowns, Australian Commonwealth Government Bonds outperformed their risky exposure counterparts and offered a valuable shock absorber. On one occasion in 1994, the defensive exposure recorded its softest return – even so, the exposure still outperformed the share market. In financial market terms, this event was extraordinary, marked by a rapid rise in rates by the RBA of +2.75% within a brief six-month period − as the RBA followed the U.S. Federal Reserve’s lead in an effort to tame inflation once and for all.

In contrast to modern times, the past decade’s inflationary pressures have been modest even in a low-interest rate environment. The reality is that the world, and in particular the U.S., is currently more concerned about deflationary pressures.

Looking at this historical view where interest rates were much higher than today and inflationary pressures were mounting, high grade bonds have been an effective diversifier. However, in evaluating how the asset class has performed in conditions more similar to our current environment (i.e. low prevailing interest rates), can they still be relied upon today?

Performance of high grade bonds in low (or even negative) policy rate environments

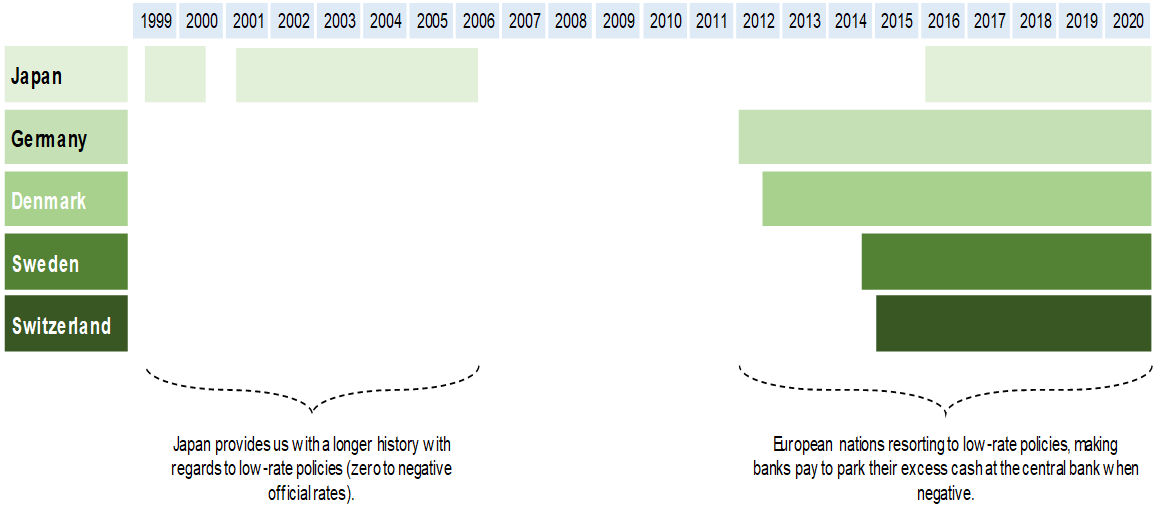

Low (and even negative) rate environments have been employed by central banks across a range of developed market countries, including most notably Japan, Germany, Denmark Sweden and Switzerland (see chart 2). A look at a range of real-life and tangible episodes from around the world to assess the low rate policy effects on the ability of high grade sovereign bonds to defend and protect portfolios against equity risk.

Chart 2. We have access to a long history of low-rate policies (zero to negative official rates) across a range of developed market countries

Selection of developed markets that have employed zero to negative interest rate policies.

JCB team analysis, using data sourced from Bloomberg.

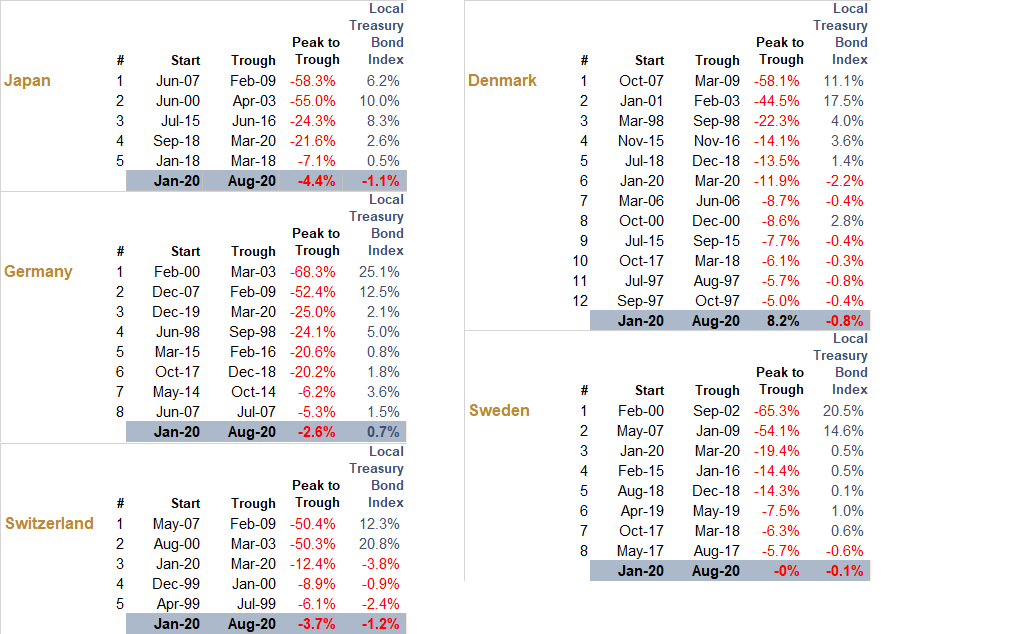

Consistent with the earlier analysis, chart 3 shows the maximum drawdown events for each nation’s local shares (i.e. less than -5%) versus the performance of the local treasury index (i.e. high grade sovereign bonds).

Chart 3. Local high grade sovereign bonds have dampened local share market drawdowns, even with low yields.

Maximum share market drawdowns, alongside treasury bond market performance.

JCB team analysis, using data sourced from Bloomberg. Dates to 23 July 2020.

High grade bond and equity positioning: a strong counterbalance

The share market declines (or left-tail events) illustrated above have been fairly frequent, and, as with financial market stress, other risk asset classes also suffered losses – including international shares and listed property, which can provide limited diversification during periods of extreme volatility as there is correlation between risk assets.

With more than 25 years of Japanese policy rates at 0.50% or lower, and low to negative rates since 2012 across key developed markets such as Switzerland, Germany, Sweden and Denmark, local treasury bond markets have provided solid accretive returns coupled with continued muted volatility. Low yield levels alone aren’t necessarily a reason for investors to ignore high grade bonds.

Duration and the risk/return payoff for portfolios

Some investors believe that a bond benchmark with a longer duration should be avoided. The reality is that a longer benchmark duration does not necessarily lead to greater risk. A +1% increase in yields will result in a higher capital loss relative to a lower duration (as it was during much of the 1990s) – this is mathematically true. But there is more to bond risk than just this single metric. To understand this, consider both the duration level (i.e. the weighted average time to receive all cashflows – coupons and principal), and the chance of a shift in yields.

With potential signs of an overheating global economy around 1994, the probability of yields increasing over a 12 month period were much greater than they are today. Policy makers were concerned with managing rising inflation and the potential for economic overheating. Today’s policy makers are busily trying to raise and maintain a reasonable inflation trajectory via significant stimulus and policy accommodation.

The world is in a far different place to the mid-1990s.

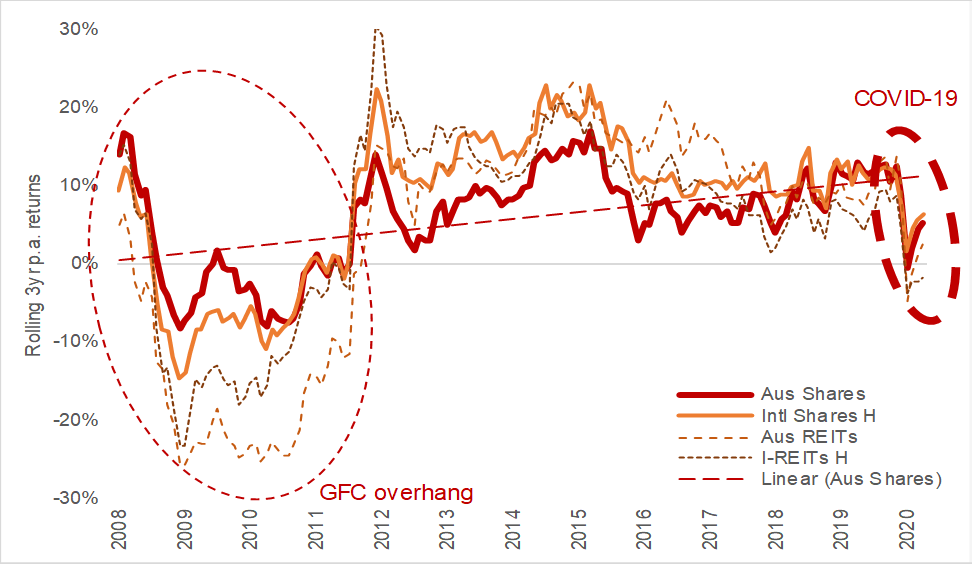

Asset class behaviours since the Global Financial Crisis (GFC) have long conditioned investors to expect more of the same (that is, elevated returns partnered with dampened risks, linked to central bank/government moral hazards) – see chart 4.

February and March 2020 reminded investors of the need to appropriately assess risks, changing economic conditions and the potential for real market drawdowns. Investors re-learned when markets turn, they turn quickly. Against this backdrop, it is no surprise that investors now lean toward defensive exposures and look to position portfolios for a sober forward-return environment.

Chart 4. Where will future returns come from?

Rolling 3 year p.a. returns of Australian and International shares, Australian and International REITs.

JCB team analysis, using data sourced from Bloomberg.

For a variety of reasons, bond yields have declined across the globe, providing investors with much lower coupon rates. This implies that compared to higher yielding environments, cash flows from fixed income are more dominated by the capital return at maturity. Even with duration levels rising, and yields falling, high grade sovereign bonds still retain their defensive properties.

Don’t fear zero or negatively yielding bonds in a portfolio

As illustrated, high grade sovereign bonds have broadly moved in the opposite direction to shares – even at very low yields – displaying low-to negative-correlation to risk assets.

High grade bonds as a classic defensive exposure are income-producing assets, meaning that unlike shares (which primarily rely on capital appreciation to drive returns), they derive the majority of their returns from income, and the income on their income. Far less defensive assets such as corporate credit, illiquid or speculative exposures are often allocated to portfolios for defence, income and liquidity, but often fall short of these qualities.

A global bond allocation can provide the additional country/regional, currency and security diversification, alongside with currency yield pick-up. Global sovereign bonds receive their returns from coupons (income), changes in bond values from term structure shifts and, often neglected, the currency hedge yield pickup (in effect, the forward premium from the difference between Australian and offshore cash rates in the currency that is hedged).

Correlation measures between shares (domestic being the Australian Treasury Bond Index and offshore, the G7 Treasury Bond Index as shown in charts 5 and 6) highlight the benefits of this defensive asset class. Rolling correlations remain relatively low (or even negative) over extended periods. Even with low interest rates, these metrics have not spiked, countrary to some market beliefs. Simply put, if high grade bonds were to lose their protective properties, correlations would also dramatically increase in poor share market periods, and approach 1.0. This however is not the case in Australia, or globally in the markets we have identified as having low to negative rates.

High grade sovereign bonds have done an effective job in diversifying share market risk

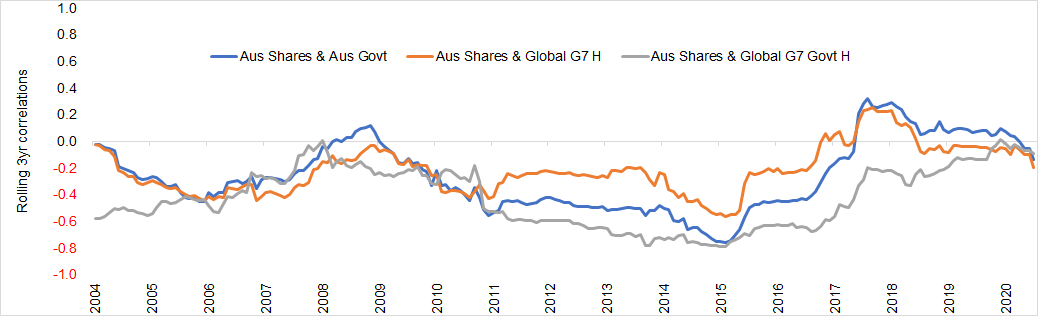

Chart 5. Rolling 3 year correlations: Australian Shares and High Grade Sovereign bonds

JCB team analysis, using data sourced from Bloomberg.

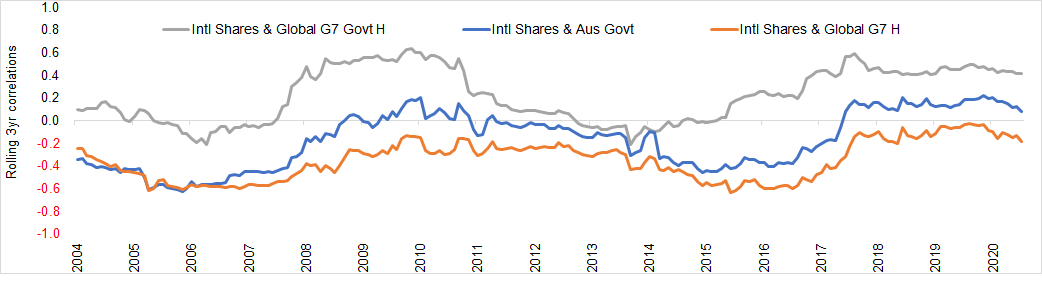

Chart 6. Rolling 3 year correlations: International Shares and High Grade Sovereign bonds

JCB team analysis, using data sourced from Bloomberg.

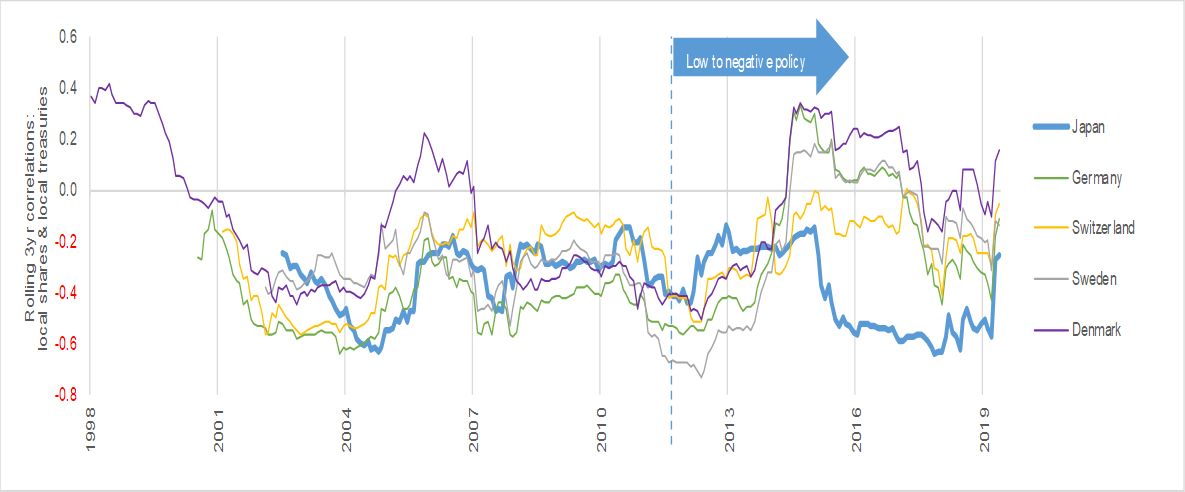

The countries with low interest rate policies show the same type of rolling correlation outcomes between their respective local share markets and local treasury markets. In some instances (such as Denmark), persistent negative correlations have become marginally positive in recent times – but very weak. This means that the diversifying properties of high grade sovereign bonds have largely remained intact.

Chart 7. Rolling 3 year correlations: Local share markets and local treasury markets

JCB team analysis, using data sourced from Bloomberg.

The prospect of a rise in inflation and future interest rates

By the end of 2019, the world was already showing signs typical of a late-cycle phase. Material structural imbalances were unfolding including spluttering regional and global demand, over-indebtedness in major pockets, and weak inflationary impulses. The onset of COVID-19 has dramatically devastated the world, and central banks and governments have quickly implemented enormous emergency liquidity and accommodation measures to prevent the world from descending into deep recession and potential depression.

Meanwhile, three key megatrends have conspired to temper worldwide growth and inflation.

- Aging demographics – the older generation increasing in proportion to many countries’ populations, meaning rising public financing obligations, and changing workforce dynamics.

-

Technology innovation (resultant increasing industrial efficiency, decreased production costs) and the altering of the human/physical capital balance – producing headwinds for global spending levels, economic growth and inflation.

-

Massive (and ever growing) debt burdens, which traditionally lower additional credit creation, spending and investment – incentivising central banks to keep rates lower for longer.

To be sure, inflation could become an issue down the track. The enormous fiscal and monetary easing alongside with re-emerging supply chains and disillusionment with globalisation in favour of local independence could all provide the impetus for rising prices. One possible scenario sees a global economic recovery brought about by vaccine development and widespread distribution, lockdown removals and the effects of stimulus combining to resemble the periods following World War II. Such an optimistic scenario differs markedly from where the world is currently. We have witnessed the sharpest fall in U.S. growth expectations and the fastest collapse in the U.S. labour market of all time. Treasury yield curves in Australia and the U.S. at the time of writing remain decidedly flat, with the market concerned about a prolonged global recession (or even depression) from the fallout of the COVID-19 shock. The pathway to recovery from here may be potentially longer than broadly expected.

Strengthening portfolios through high grade sovereign bonds

There can be no argument – bond yields are indeed at historically low levels, an indication of the emergency settings in place to keep the world from descending into a bleaker alternative.

Based on our assessment, in both rising and falling interest rate environments, high grade bonds can play a critical role in portfolios. Even more so in the current environment of poor global growth, low inflation and falling yields, which look set to remain.

Five reasons to rethink an allocation to high grade bonds

- Downside protection: High grade bonds perform vastly differently relative to risk assets and other debt instruments. They can be a source of genuine and evergreen liquidity and portfolio defence.

-

Low correlation to risk assets: Throughout history, high grade bonds have provided portfolio protection, especially against more risky exposures (albeit potentially tempered as a function of lower yield levels).

-

Efficient returns: While an exposure to high grade bonds will likely deliver more modest returns compared to long-term trend, this needs to be viewed relative to a set of traditional asset class returns which are likely to be more muted. Each basis point of return – especially looking ahead – will matter (and be harder to come by).

-

Asset quality matters: March 2020 has provided investors with a valuable reminder that ‘asset quality’ matters – especially in times of stress. Many asset owners have been soured by the experience of widening fixed income sell spreads, limited withdrawal windows, and for pre-retirees the occurrence of a sequencing risk event. More attention is likely to converge on higher quality assets.

-

Portfolio diversification: A defence exposure to balance out other defensive exposures and provide further portfolio diversification, in a world where volatility is here to stay.

Learn more

In times of economic stress, adding high-grade bonds to your portfolio alongside other risky assets can help get the balance right between risk and return – this is absolutely crucial now as investors seek higher income. Stay up to date with all my latest insights by clicking the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from 2001 in New York, Tokyo, London and Sydney, with Merrill Lynch/Bank of America Merrill Lynch. Over his career, Charles has managed large Government Bond portfolios in key major currencies and derivative instruments. During this time, he has managed through the spectrum of financial market dynamics, including September 11, 2001, the Global Financial Crisis, Eurozone crises, the US credit rating downgrade and Chinese/Greek concerns.

........

This information is provided by JamiesonCooteBonds Pty Ltd ACN 165 890 282 AFSL 459018 (‘JCB’) and JamiesonCoote Asset Management Pty Ltd ACN 169 778 189 AR No 1282427. Past performance is not a reliable indicator of future performance. The information is provided only to wholesale or sophisticated investors as defined by the Corporations Act 2001 (Cth). Neither JCB nor JCAM is licensed in Australia to provide financial product advice or other financial services to retail investors. This information should not be considered advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling units and does not take into account your particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice.

4 topics

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from...

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from...

Comments

Comments

Sign In or Join Free to comment