TOL - 7th Dec, 2020

Don’t fight the central banks in 2021

It’s that time of year again: the annual fixed income bond kicking competition as we head into 2021, something not even Pfizer could develop a vaccine for.

No doubt you will read plenty of articles in the coming weeks about why bonds should be avoided in the future. Most will be written by the same folks who have been wrong quite consistently – but this won’t stop them arguing why you should own things like gold, bitcoin or just more equities in general.

If we’ve learned anything in the post GFC period, it must be ‘’don’t fight the central bankers”. Such changes would introduce volatility and differing levels of liquidity reduction to defensive allocations. Alas, the current narrative machine is humming a sweet note of pro risk and general optimism into a vaccinated post COVID-19 world. The narrative machine also suggests inflation will magically appear despite powerful secular forces including:

- high debt levels

- poor demographics

- technology

- automation

- lack of unionisation

- globalisation.

Add to that high single digit unemployment around the world as we see plenty of spare capacity keeping disinflation as the prevailing pricing force. The anti-bond commentators will suggest bond yields will rise BUT risk assets will be a nirvana allocation that will also go up in value.

Hang on – what?! – did we miss something here? As I join those dots, I fail to make the connection between higher asset prices and higher cost of capital in the most leveraged global economy of all time. We see some real problems in this, as we again remind folks that interest rates are the virus that affects all asset markets.

There is likely some recency bias in this thinking. The meltdown of March is now a distant memory, as markets have powered ahead on policy response combined with a steep economic recovery from a dire situation. 2021 certainly looks brighter on several fronts (an adult in the White House is a great start) but as the disaster relief funding programs start winding back, it is rational to expect a period of anti-risk as markets taper to demand and incentivise policy makers to complete on ‘’whatever it takes’’ policies, adding to financial repression.

Mandated performance, defense

Bond yields will likely remain rangebound, anchored by central bankers’ long-term commitments to low policy rates, combined with active quantitative easing programs that essentially mandate performance. We are not predicting this; we are observing it the world over. Markets have been supported by QE for many years, as far back as Japan’s first QE-style program in 2001.

Counter-intuitively, bonds in markets with very low or negative yields still generate positive total returns due to the steepness of their curves which experience powerful roll and carry. Amazingly, despite low or negative yields, bonds still generate negative portfolio correlation to risk assets. This is particularly true in periods of equity stress and exceptional liquidity, which allows investors and allocators to vary their portfolio to take advantage of deeply discounted growth assets like we saw in March.

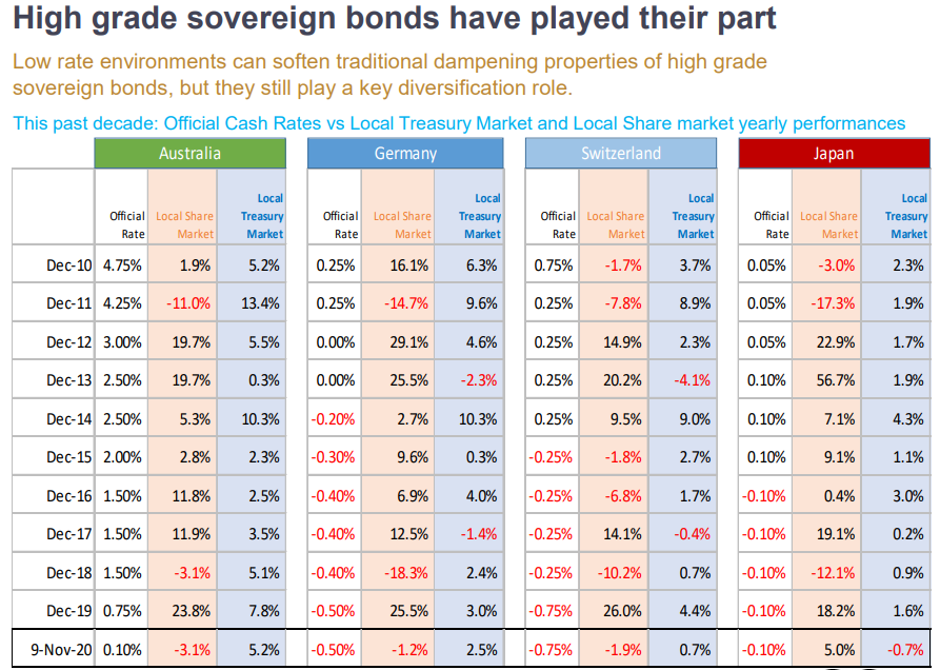

Source: Jamieson Coote Bonds. Past performance is not indicative of future performance

Looking at developed markets such as Germany, Switzerland and Japan, total returns from government bonds have remained positive despite negative Central Bank rates (local equity market performance also included).

This is driven by ‘’carry and roll*’’ a compelling force in a positive sloping term structure of interest rates. Many folks could be forgiven for thinking the near 50% return from US Treasuries over the last decade would be attributed to a rally in duration when in fact that was only a fractional (20%) return driver – far more important is the ‘’carry and roll’’ function when decomposing the return streams as seen below.

US Treasury performance attribution*

* Past performance is not indicative of future performance

So, when the bond market naysayers come knocking again this festive season, politely remind them that they have been consistently wrong and that fighting their friendly central banker will likely prompt an unplanned career change fairly soon in a market that is mandated to perform.

One thing investors can't ignore in 2021

The above wire is part of Livewire's exclusive series titled "The one thing investors can't ignore in 2021." The series will culminate in the release of a dedicated eBook that will be sent to readers on Monday 21 December. You can stay up to date with all of my latest insights by hitting the follow button below.

*The ‘’carry’’ is the bond income – just like a dividend. The ‘’roll’’ is as follows: If RBA has Yield Curve Control to hold 3 years ACGB bonds at 0.10%, if we buy a 5yr ACGB bond at 0.50% and hold it for one year it becomes a 4 year bond. Assuming it will be a 3 year bond with a yield of 0.10%, unsurprisingly the as a 4 year bond its is very likely to yield around 0.30% ( ie over a one year period it has had a capital appreciation from 0.50% to about 0.30% - as falling yields = higher prices). So the steepness of the bond curve generates huge amounts of ‘’roll’’ as seen in the UST example table where ‘’duration’’ is only 20% of the UST return for last decade

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from 2001 in New York, Tokyo, London and Sydney, with Merrill Lynch/Bank of America Merrill Lynch. Over his career, Charles has managed large Government Bond portfolios in key major currencies and derivative instruments. During this time, he has managed through the spectrum of financial market dynamics, including September 11, 2001, the Global Financial Crisis, Eurozone crises, the US credit rating downgrade and Chinese/Greek concerns.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

2 topics

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from...

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from...

Comments

Comments

Sign In or Join Free to comment