Expect a retest of March lows; the bigger question is what happens next?

We’ve seen the panic. Now we’re enjoying the relief. But the worst is yet to come - and then what? That’s the big issue on the mind of Chris Watling from Longview Economics.

“I would expect a retest over the next 3 to 6 weeks of those stock market lows that we took in on 23 March.”

Watling made the comments at a recent webinar hosted by Fidante, where he presented some informative slides to show typical price action following a crash.

Image: Chris Watling, CEO & Chief Market Strategist, Longview Economics

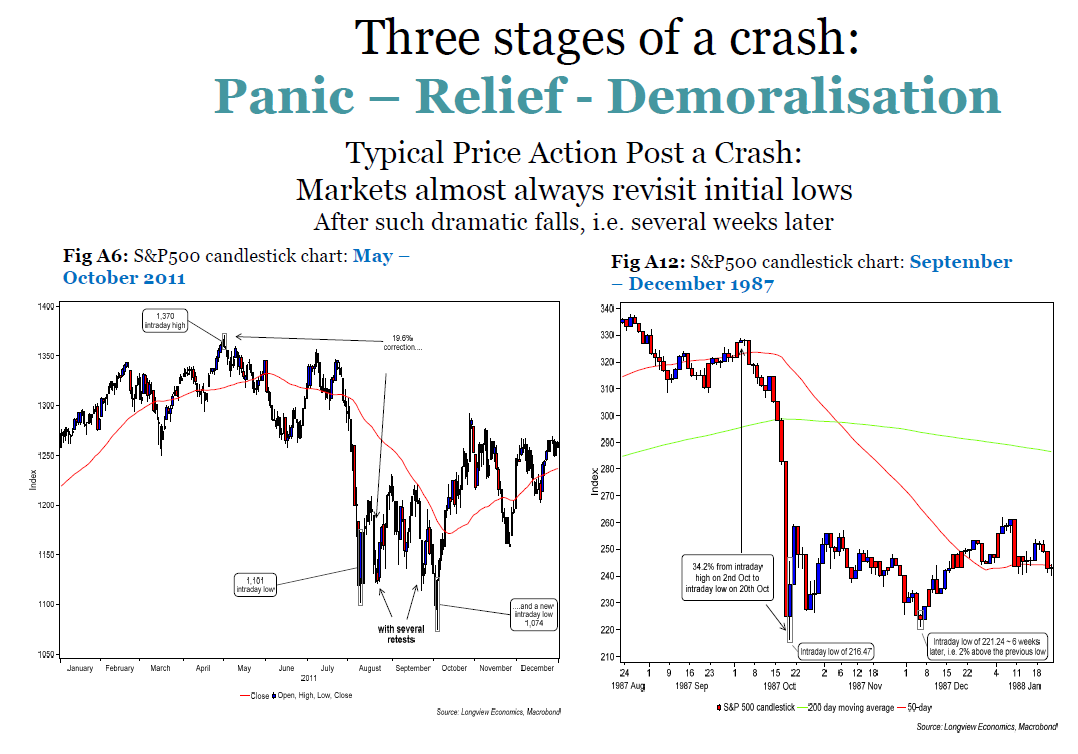

The below charts show the “demoralisation” stage is looming, as evidenced by the S&P 500 retesting its initial lows after sharp falls and subsequent relief rallies back in 2011 and 1987.

"In 13 of the previous 15 sharp corrections in global equities, the market retested it lows several weeks after the initial low. Don’t be surprised if that happens and it will happen quickly."

Click on the image to enlarge

That being said, equities have priced in a lot of the bad news wrought by the “three black swans” of COVID-19, the oil price crash and dysfunctionality in markets.

The case for a 2-3 month rally, but then what?

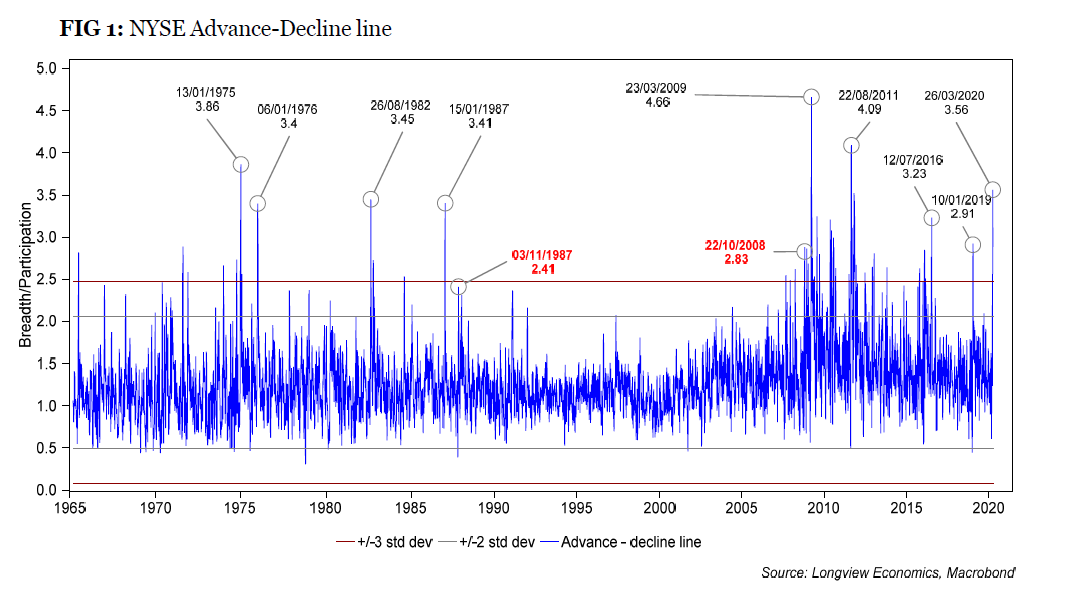

Beyond the retest, Watling reckons there is the case for a 2-3 month upswing. He points to one of his favourite indicators: the NYSE Advance-Decline line, which measures the number of advancing stocks against the number of declining stocks.

Click on the image to enlarge

When this indicator spikes to a very high level, it could signal the start of a short-term or secular bull market – and which one is the big question for investors. Watling turned to history to quantify two likely outcomes as shown in the below slide.

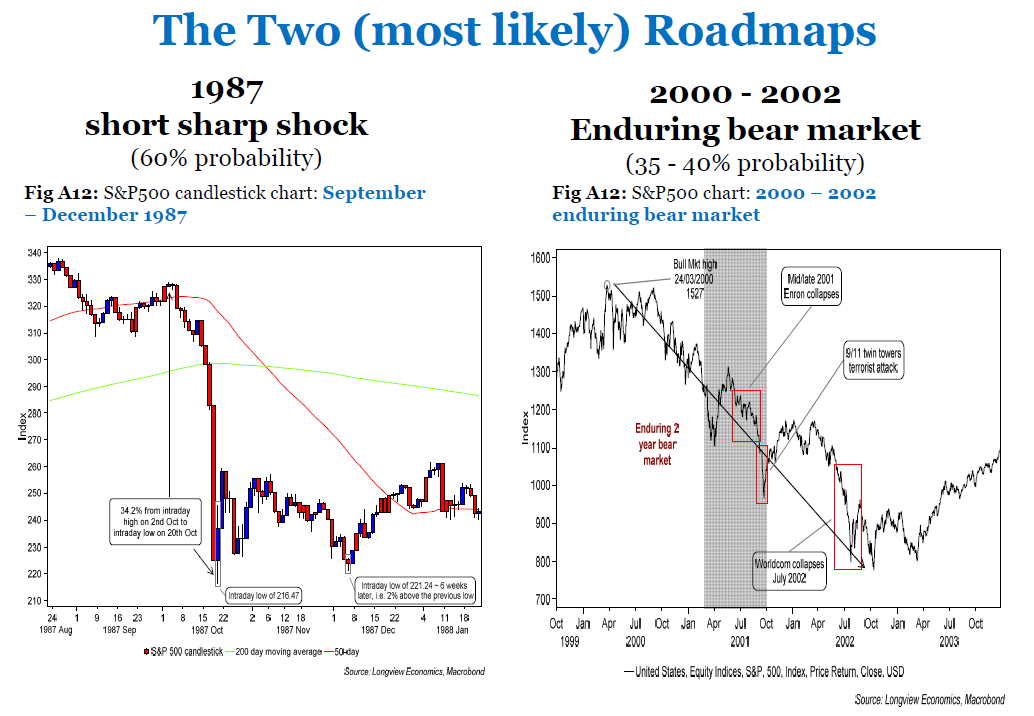

Click on the image to enlarge

- Watling was originally bullish for 2020 in a previous interview with Livewire but this view has changed due to the severity and evolving nature of the COVID-19 situation.

- The central case (60% probability) now is for a short sharp shock and then recovery for markets like in 1987. This would be contingent on the aggressive global policy response and governments successfully containing the virus and preventing future outbreaks (or finding a vaccine). In this roadmap, the market could experience a V-shaped recovery in the second half as household spending makes a roaring comeback when people return to work and partake in leisure activities again, and spend additional money that they saved or banked during lockdown.

- However, there’s also a high probability (35-40%) of an enduring bear market like the one seen after the tech bubble burst in 2000-2002. This would happen if 1) The virus resurfaces and lockdowns are repeated and 2) The “cheap money” holding up zombie companies and unicorns dries up, leading to a cascade of businesses going bust, with Watling pointing to WeWork as a potential victim.

Three investment themes on the other side

To finish, Watling said – as has happened during previous bull market rebirths – new themes and winners would arise from the current crisis, and he called out three in particular.

Theme 1 – Inflation is coming back

Firstly, inflation will re-emerge as a result of the accumulated monetary action and fiscal spending in the 2010s, COVID-19 and unwillingness of populations to tolerate cutbacks.

“The politics of the world now are too populist for austerity. I don’t think the populations of the western economies will take more austerity and I think governments will therefore have to keep doing QE programs, keep printing money to fund their deficits and I think that’s going to be much more inflationary than we saw post-GFC.”

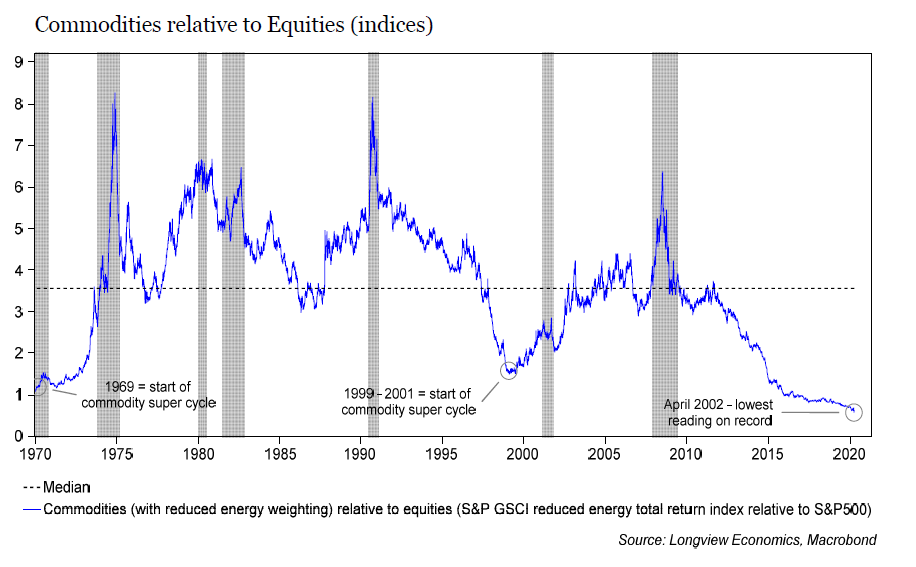

Theme 2 – Commodities to outperform

Dovetailing into the inflation thematic is commodities and resources stocks, which should benefit from rising prices.

“If I’m worried about inflation and money printing then commodities should be a beneficiary so I think there’s a very good argument for seeing a potentially good run in commodities, maybe even a commodities super cycle, as inflation comes back into the global economy”.

There’s also a value angle in this, with the below chart depicting commodities at record low levels relative to equities. Aside from iron ore, Watling notes that many commodities are at 15-20 year lows and oil prices would need to move higher to sustain production as demand recovers.

Click on the image to enlarge

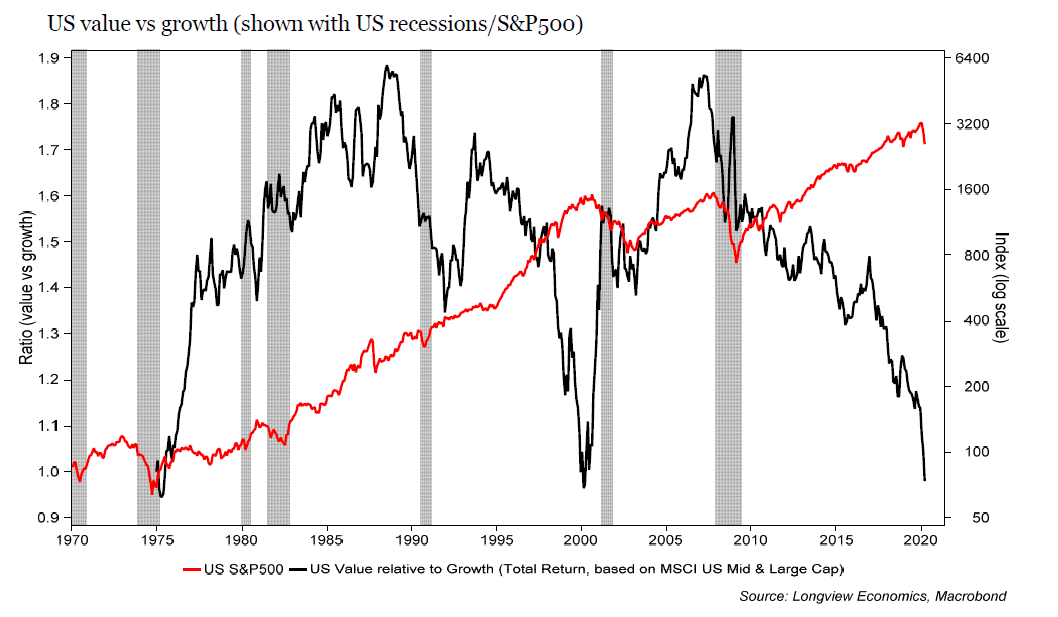

Theme 3 - Value will be King

On the same token, value stocks’ performance relative to growth are at extremes and inflation could be the trigger that sees these two styles of equities see mean reversion in performance; companies such as banks benefit from higher inflation and have the added luxury of governments and central banks backstopping loans.

“A lot of good news is in the price for growth and a lot of bad news is in the price for value.”

Click on the image to enlarge

Other ideas

Watling also favours gold and treasury-inflation protected securities (TIPS) in an inflationary environment, and he also likes US high yield and investment-grade debt as these assets are backstopped by the Fed. However, he's not keen on equities in the near-term and government debt in the medium-term.

Access the webinar

Access the full webinar recording here and view previous commentary/interviews with Watling on Livewire here.

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Based in Canada, Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

4 topics

1 contributor mentioned

Based in Canada, Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

Expertise

Based in Canada, Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

Expertise

Comments

Comments

Sign In or Join Free to comment