FAANGM-mania, or are there good reasons for these high prices?

Beatle-mania? Maybe, but it turned that John, Paul, George and Ringo sold a lot of records

Even after the recent pullback as a result of news of a likely COVID vaccine, the price appreciation of the FAANGM (Facebook, Amazon, Apple, Netflix, Google and Microsoft, to which we could add NVIDIA and Tesla) over the past few months has taken many investors by surprise, leading to questions around whether these valuations are sustainable.

At face value, it is tempting to say no. But the explanation is not that simple.

A BRIEF HISTORY OF MANIA(s)

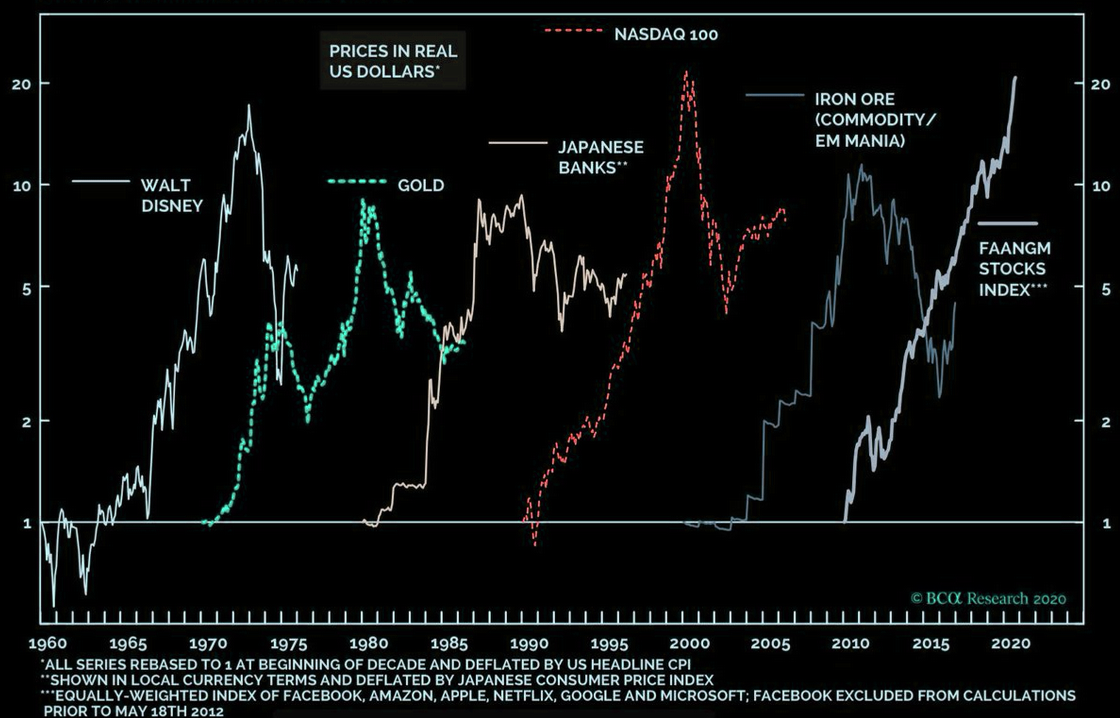

This is relevant to the chart below, which forms the centrepiece of a thoughtful analysis of stock price booms (mania, as the term is used below), including FAANGM, going back to 1960, by BCα Research.

None of these mania could be considered the mainstay of a global, broad-based usage megatrend driving growth in productivity across every sector, while simultaneously reducing the draw on global resources.

The iron ore/commodities mania of the nineties, shown in the chart above, was part of the modernisation of China by decree from the Politburo, with the aim of spurring industry and consumerism among the people. Australia and many commodity-rich emerging market countries enjoyed higher earnings as part of that trend. But the world’s largest economy, the US, did not really participate significantly, except through cheaper imports, but with an accompanying hollowing out in manufacturing. There was a boom in resources companies, but it did not represent a boom in global growth.

Also shown above is the mania for Japanese banks (and the land associated with them). These were powerful trading houses in the eighties, but ultimately swooned under the weight of their own cross-shareholdings – at one point considered a strength. The mania around the value of Walt Disney reflected the growth in available leisure hours. In our view, none of these booms should be considered integral in the context of lifting global growth.

We have been around way too long to say with any conviction ‘this time is different’. But it is worth pointing out the particular characteristics of the pricing of these companies, and how it differs from previous mania.

FAANGM are at the core of a profound shift in global business

The FAANGM’s and their related companies, using the new silicon and software tools available to them are behind significant increases in productivity, cutting out unnecessary manufacturing, storage, processing and delivery.

Thus it is that the list of non-digital interactions shrinks by the day. Few people pay bills in person using cash, or visit a bank branch except when a major transaction is in train (such as a home purchase); online shopping with contactless delivery is well-advanced; the consumption of entertainment does not depend on a visit to a theatre or even the rental of a DVD – indeed in recent days UK cinema chain Regal has announced the temporary closure of 663 theatres, while in the US, Cineworld, which is the second largest cinema chain in the US, has closed for the second time after briefly re-opening. Newspaper sales have plummeted, as has subscription to traditional pay TV. Other than in museums, junk shops and garages, it is very hard to find a typewriter. The printing of material to inform consumers has diminished exponentially – information on areas as diverse as travel and tax treatment of income are all found online. The Woolworths across the road from our office does not accept cash (though this might be related to COVID). When was the last time anybody used a phone book?

A small amount of history: The first industrial revolution was kicked off by weaving machines, with a patent granted in 1747 to Robert Kay, which initially doubled output. The first machine age had begun, and it rolled through many industries from steelmaking to steam-powered train travel. Machine tools revolutionised weapons production, building and manufacturing. Electricity can be seen as the beginning of another industrial revolution including telephony and communications, as well as on the factory floor for mass production of cars, and eventually labour-saving devices.

We don’t have great data sets for the pricing of companies in either the weaving or electrification industries, but it’s probably safe to say they were trading at higher valuations than those companies still operating in the old ways.

Indeed, a paper published by the Harvard Business School written by Tom Nicholas in 2007 states “Intangible capital growth was substantial in 1920s America, investors realised it, and they integrated this information into their market pricing decisions. Conventional wisdom suggests that unrestrained speculation created a divergence between share prices and fundamentals. This article has offered a new perspective: the interaction between innovation and changes in investor attitudes towards intangible capital fomented large stock market payoffs for innovating firms. (It) was not an epoch of irrational exuberance as is often claimed, rather investors linked rational (positive) expectations about fundamentals to the market value of firms.”

The MIT academics Erik Brynjolfsson and Andrew McAfee in their book “The Second Machine Age” dimensioned the forces driving change in our lives, with businesses around the world adopting digitisation as a means of improving customer experience, including driving down the cost of goods and services.

The current machine age

Depending on definitions, we are now in the second or third machine age, and have been since the invention of the silicon semi-conductor 60 years ago. Broadly, what has taken place is that advances in miniaturisation of the chips themselves has made Gordon Moore’s observation into a law – processing power doubles and cost halves every 18 months.

The pricing of the FAANGM companies we believe simply reflects investors seeking to estimate the value of the intangibles (software, operating systems, platforms), just as the Harvard paper concluded. For example, the world’s companies are migrating their processing needs from on-premise servers (run by the IT department) to private and public based clouds – racks of servers and related equipment with pricing optimised for users. In the past, server users maintained in-house IT departments with server racks. While this allowed for the handling of the busiest day of the year, it would then run below optimal capacity utilisation the rest of the time, and so be a waste of money. The value of businesses running these cloud servers far exceeds the cost of the servers themselves, and goes to intangible value, as the Harvard paper notes.

Moore’s law is breaking down with respect to Moore’s particular kind of CPU-based processing, but if anything, semi-conductor utility is moving massively faster than Moore’s law as accelerated processing takes off.

The usage boom and what comes next

So here we stand: Google processes around 67,000 search queries per second – there are not enough white-coated engineers in the world to manually find answers to this number of queries.

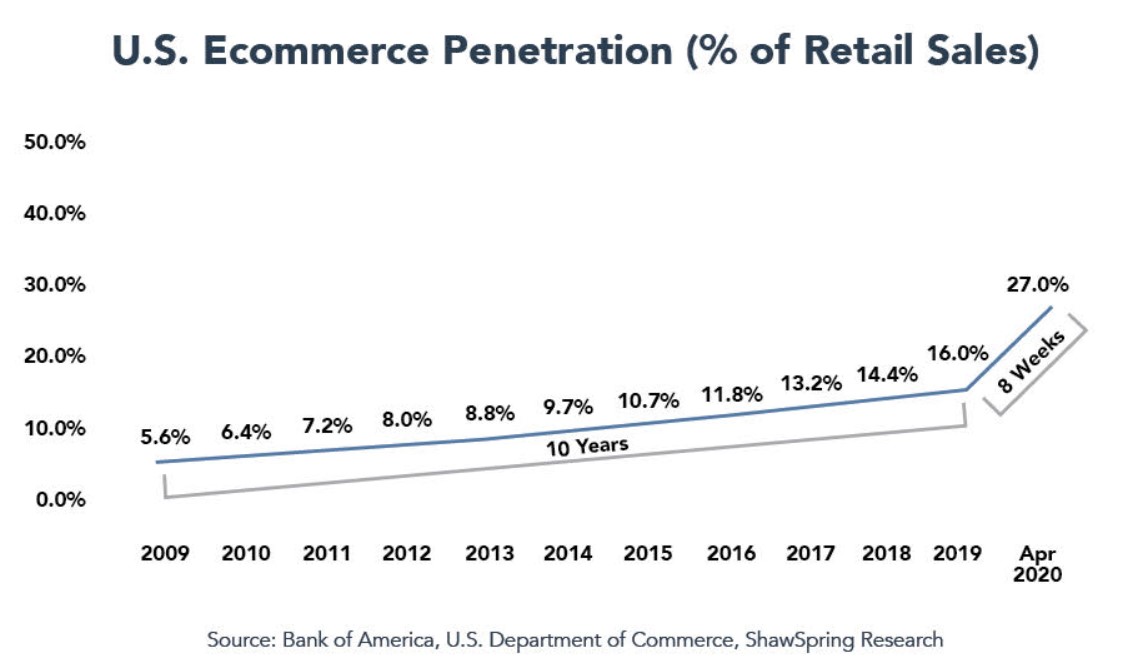

Ecommerce, which had only reached 16% penetration at the beginning of this year, has grown by almost half in a matter of months, as the chart below shows.

This is a true boom in usage – the technology bubble of 2000 suggested that there was little more to building a specialist online retailer of dog food than the registering of the website Pets.com. A lot has changed in twenty years.

So yes, there has been a surge in the share prices of companies that are delivering online productivity. The next phase in this process is that new companies will emerge, or existing companies will reinvent themselves, to create disruption across a whole range of industries. Our job is to identify these companies and make judgements about their valuations. In our view, what is happening to the FAANGM’s is a sign of a broader change that we expect to roll through our communities over many years to come, disrupting the businesses of incumbents across a whole range of industries.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

CIO of Loftus Peak, a specialist global fund manager with a track record of successful investment in some of the world's fastest-growing listed businesses.

3 topics

CIO of Loftus Peak, a specialist global fund manager with a track record of successful investment in some of the world's fastest-growing listed businesses.

Expertise

CIO of Loftus Peak, a specialist global fund manager with a track record of successful investment in some of the world's fastest-growing listed businesses.

Expertise

Comments

Comments

Sign In or Join Free to comment