Finding income in a 0% world

When COVID-19 hit Australia in March, credit spreads across the whole investment grade bond market responded by migrating wider and prices headed lower. We saw this as an opportunity to lend to quality companies at very attractive yields, with strong capital gains available for those investors who were able to look past the dark clouds of market turmoil.

Over the subsequent six months we’ve witnessed unprecedented policy responses from governments and central banks both at home and abroad. This has seen credit pricing recover, with spreads on average having rallied back toward pre-pandemic levels.

While most of the extreme value has perhaps already been realised, for high quality issuers the technical support for credit spreads to tighten further remains. From here, we see a gradual grind tighter in credit spreads as a distinct possibility.

Investing through a recession

As Australia prepares to weather its first recession in three decades, at first glance it may seem counterintuitive to expect positive outcomes from credit markets. We expect a lasting legacy from the 2020 lockdown shock, which will likely result in reduced consumption, mortgage arrears, property rental income falls and SME defaults. In this environment, industry and issuer selection becomes paramount as compensation for these risks through credit spreads and outright bond yields has migrated lower.

The current round of reporting from corporate Australia also makes bleak reading as trading conditions remain challenged in broad sectors. For defensive, income-oriented investors it’s important to focus on businesses that have a reason to exist and serve a valued purpose to society.

We look for prudently run balance sheets and ample financial flexibility in order for companies to survive and absorb temporary shocks. A ‘quality before price’ mindset remains crucial in navigating credit markets. For these reasons, investors must be disciplined in differentiating high quality, stable corporate debt with low default risk from lower quality (or lower in the capital structure) debt of COVID-exposed companies that have genuine default risks attached.

For more than 25 years our Fixed Interest team have invested through numerous market cycles. While this is Australia’s first recession in 29 years, we have learnt that investing through a recession requires investors to take a survivorship mindset.

Long-term spread trends

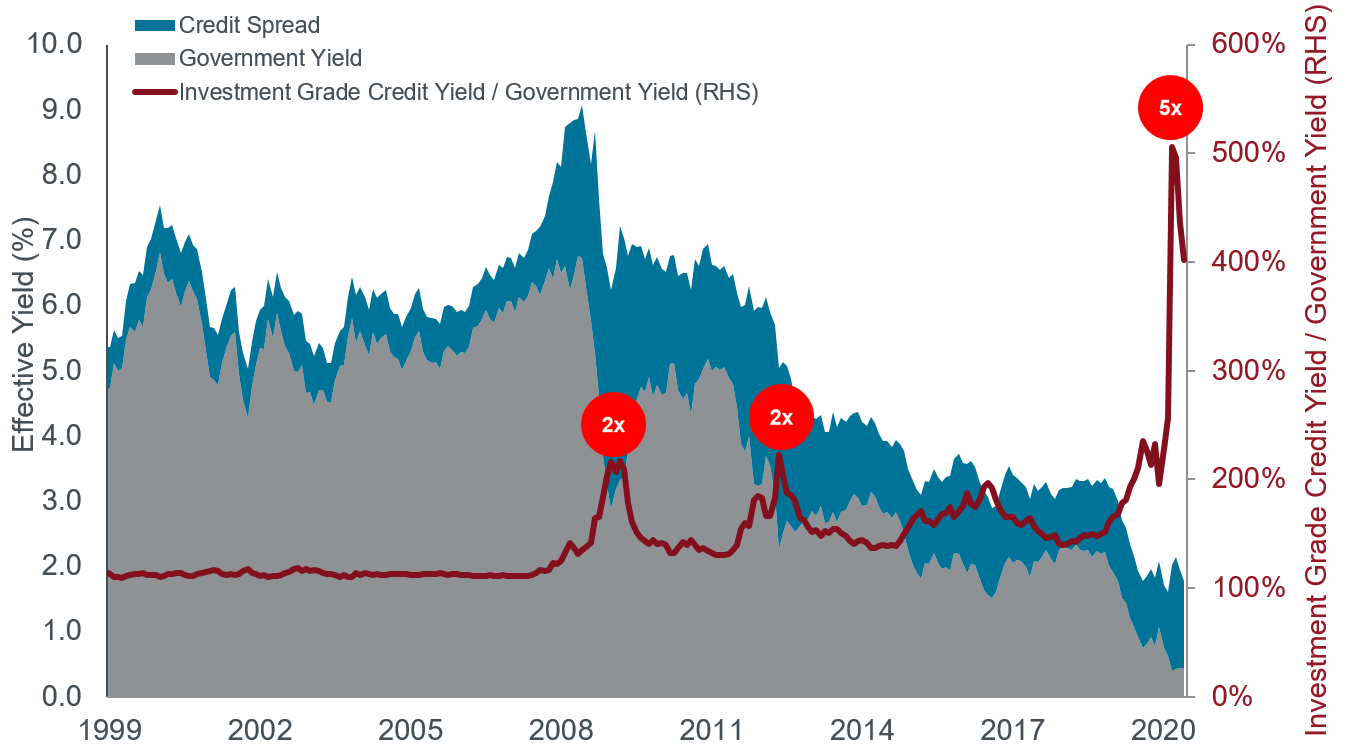

While the past 20 years have seen significant changes to the Australian corporate bond market, the past decade has been particularly influential, with improved financial system stability and unprecedented low interest rates being key factors. That said, we think it is instructive to look at longer-term data as an insight into the way markets can price credit risk for extended periods of time. This is especially the case against a backdrop of close-to-zero cash rates and ultra-low risk-free bond yields.

With the risk-free rate at all-time lows, the additional yield and return from credit spreads makes up a higher proportion of the absolute yield than at any time in history. Arguably, credit spreads are now more valuable to an investor than ever before. The investment grade Australian corporate bond market is currently offering investors an additional spread of 1.10% above government bonds, equivalent to 3.25 times the yield, with very low default risk.

Chart 1: The rising contribution of credit spread to income

Source: Janus Henderson Investors, ICE BofAML – Australian Investment Grade Corporate Index (AUC0). As at 31 August 2020.

Spreads today are still higher than at the start of the year when bushfires and floods were the main concern. Relative to the past 20 years, this puts compensation for investors right in the fiftieth percentile for credit pricing, arguably a fair price given the easy financial regime likely to be in place over the coming years.

We have identified that the AAA and AA rating segments (dominated by covered bonds and major bank senior debt) are trading near record lows, while A and BBB rated corporate bonds are still trading wide of their average levels and wider than at the start of the year.

While sectors like Office and Retail REITs, Transport infrastructure and Auto Manufacturers have some uncertainty around a return to ‘normal’, along with risks of potential ratings downgrades, they still offer above average spreads.

We feel some ratings migration is likely but believe this period of uncertainty presents opportunities to invest at attractive yields in companies that are well-equipped to defend their credit profile through asset divestment or equity raisings. This may not be in the best interests of shareholders, but safeguards bond holders.

Policy tailwind

Monetary policy accommodation of effectively zero cash rates provides significant underlying support to risk markets, including credit. The Reserve Bank of Australia’s (RBA) yield curve control and low rate regime is likely to persist for many years as the economy begins the road back towards full employment and sustainable inflation. A similar message has been relayed by Jerome Powell on behalf of the US Federal Reserve.

We do not see the domestic cash rate lifting before H2 2024 at the earliest, with central banks around the world likely to let loose monetary policy run harder for longer until they regain full confidence in the economic recovery. This is likely to see a period of sustained negative real yields; traditionally a positive environment for credit assets and supportive of lowering default rates. The result is that investors will be left to search for yield in a low rate environment and buyers of high-grade credit will compete for quality income-producing assets as very low yielding cash and government assets will fail to adequately protect real wealth for investors.

Pent-up demand for credit

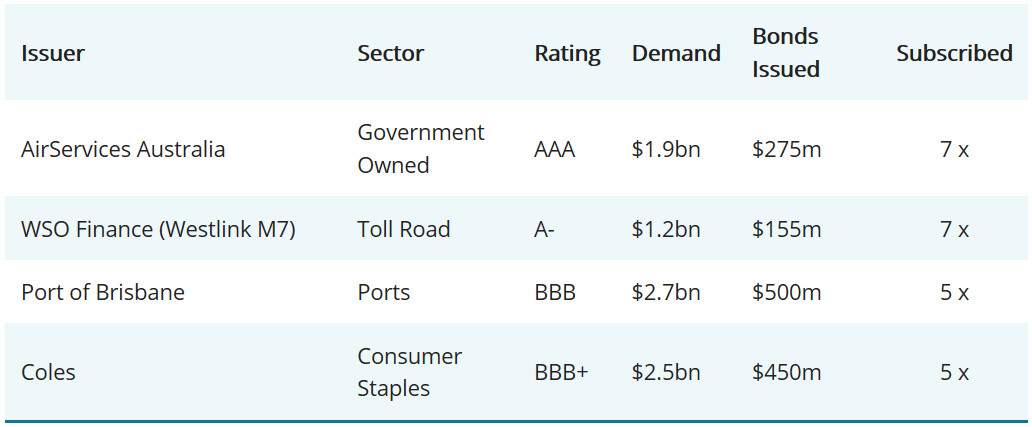

As the new primary market issuance pipeline resumed in Australia, new deals have been met with high demand. This is a theme stretching back before the pandemic and is shared with offshore debt markets. This strong appetite for new deals is indicative of pent-up demand, but with the subsequent scaling of allocations it leaves capital on the table looking for alternatives.

Table 1: Recent corporate bond issues

Source: Janus Henderson Investors, Bloomberg. As at 31 August 2020.

In answer to COVID-19’s impact on market function, the RBA established a Term Funding Facility (TFF) for Authorised Deposit Taking Institutions (ADI’s), providing surety of liquidity and allowing the banks to borrow a significant amount at 0.25% for the next three years. This facility was further expanded at the September RBA meeting to a size of $200 billion available through to June 2021.

The objective of this initiative is to reduce funding costs for local banks, which in turn reduces interest rates to support households and businesses toward an economic recovery. Australia’s first recession in 29 years has also seen a flood of deposits into the banks. These cheap sources of funding for the banks will put ongoing downward pressure on term deposit rates which could fall below 0.5% as the banks remain flush with cash over the coming years.

The knock-on effect for bond investors is that there will be little or no need for banks to borrow in public markets for an extended period.

This means investors are likely to struggle to suitably replace senior, covered or residential mortgage backed bond maturities as supply is severely curbed. Credit spreads on senior bank debt have been pushed tighter over the past few months as a result. Major bank 2025 maturity senior notes issued in January at a margin of 76 basis points (bps) are now trading at 46bps, dramatically down from highs of 150bps in March and resulting in a 5.0% return on these securities over the past five months. The lack of supply will continue to support credit spreads over the coming year.

In addition, the RBA’s repurchase facility allows corporate bond holders to access liquidity without having to sell the bonds, alleviating some of the selling pressure from market stress events like March. This may serve to curtail spread widening in future risk-off events.

The ongoing search for yield

Income-orientated investors may transcend asset classes in search of the best risk-adjusted returns and certainty of income. Equity income is challenged as some of the major dividend providers across the market have cut or withheld dividends, and shareholders may face further dilution through ongoing capital raisings. (For more information on global dividend cuts, see our long-running study here).

Current elevated equity pricing may also be a headwind, increasing the risk of a correction and potentially putting capital at risk. Meanwhile, property trust investors face a cut to their distributions as lease income faces uncertainty from tenants struggling with lockdown and social distancing measures imposed by governments.

On the other hand, the total return on corporate bonds could potentially be similar to that of equities with less volatility and lower probability of capital impairment. By way of example, Woolworths issued a 10-year, benchmark-sized, senior fixed rate bond in May this year at Asset Swap Rate (ASW) +195bps. This bond is now trading at ASW +140bps and has already delivered a 6.4% capital gain within a few months. If the spread on this same bond was to contract a further 20bps over the next year, this adds an additional 2% return in capital appreciation, which when added to the current 2.2% yield, brings the total prospective return to 4.2%. We note that even without the capital boost from spread tightening, the income alone generates an income return above likely inflation.

Despite the rally in spreads from May to August, Coles issued a similar 10-year benchmark-sized bond recently at ASW +137bps, which still saw overwhelming demand. Within one hour, the bonds were trading up 1.0% as demand for robust, “sleep well at night” corporate bonds remains an attractive proposition in a low rate regime.

Where to from here?

Recent developments in the hunt for a vaccine appear promising. While this global progress buoys risk markets, we are cognisant that we are still in a recession. It is prudent to invest on this more cautious base case and any vaccine delivery will deliver upside. Our forecast was for the economy to contract by 7% in the June quarter and fall again in the September quarter, before rebounding. For 2020 we look for GDP to fall by 5.75% before lifting by 5.5% in 2021. The economy is expected to take until at least the first half of 2022 to recapture end of 2019 levels.

As we navigate through the current economic lockdown uncertainty, further bouts of volatility and potential spread widening remain likely as sentiment ebbs and flows.

However, as we look to the years ahead, we view high quality credit income as an attractive risk-adjusted opportunity amidst a regime of zero cash rates, positive inflation and gradual economic recovery.

The journey ahead may not be perfectly smooth, but we believe above average returns are likely for corporate debt investors over the period ahead.

Learn more

Stay up to date with all our latest views but clicking the follow button below, and you'll be the first to read all our wires.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shan Kwee is a Portfolio Manager on the Australian Fixed Interest Team at Janus Henderson Investors. Prior to joining the firm, he was head of portfolio management at Omega Global Investors. He has 16 years of financial industry experience.

........

This content has been created by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). This content shall not in any way constitute advice or an invitation to invest. It is solely for information purposes. This content does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

No warranty or representation is given that as to the accuracy or completeness of the contents and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited for any action taken on the basis of this content. All opinions and estimates expressed in this content are subject to change without notice. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect.

2 topics

2 stocks mentioned

Shan Kwee is a Portfolio Manager on the Australian Fixed Interest Team at Janus Henderson Investors. Prior to joining the firm, he was head of portfolio management at Omega Global Investors. He has 16 years of financial industry experience.

Expertise

Shan Kwee is a Portfolio Manager on the Australian Fixed Interest Team at Janus Henderson Investors. Prior to joining the firm, he was head of portfolio management at Omega Global Investors. He has 16 years of financial industry experience.

Expertise

Comments

Comments

Sign In or Join Free to comment