Finding The Next Vocus - 5G Networks

What a difference 3 months can make. Investors are nervous with the main Aussie index off about -13% from its highs amidst talk of a bear market. But in small cap land, we are already there. The Emerging Companies Index is down by more than -20% this year, meeting the (admittedly arbitrary) definition of a bear market. Small caps, as is customary, have been hit harder than large caps as liquidity dried up.

This is a good time to begin looking for value, because plenty of it is emerging. You’ll probably want to be careful though and look for businesses selling products and services not exposed to consumer confidence and with a model that can still work in tough markets - there are a handful that we’ve been buying recently.

5G Networks (ASX:5GN) is one example of this. It is a completely under the radar telco and cloud services provider trading on ~5x EV/EBITDA. The company is cashflow positive, the MD and board own a big chunk of shares and they are pursuing a model the market loves, evidenced by a number of recent success stories.

In my opinion this may be a good time to get on board what will be a nice growth story over the next couple of years.

The 5G Story

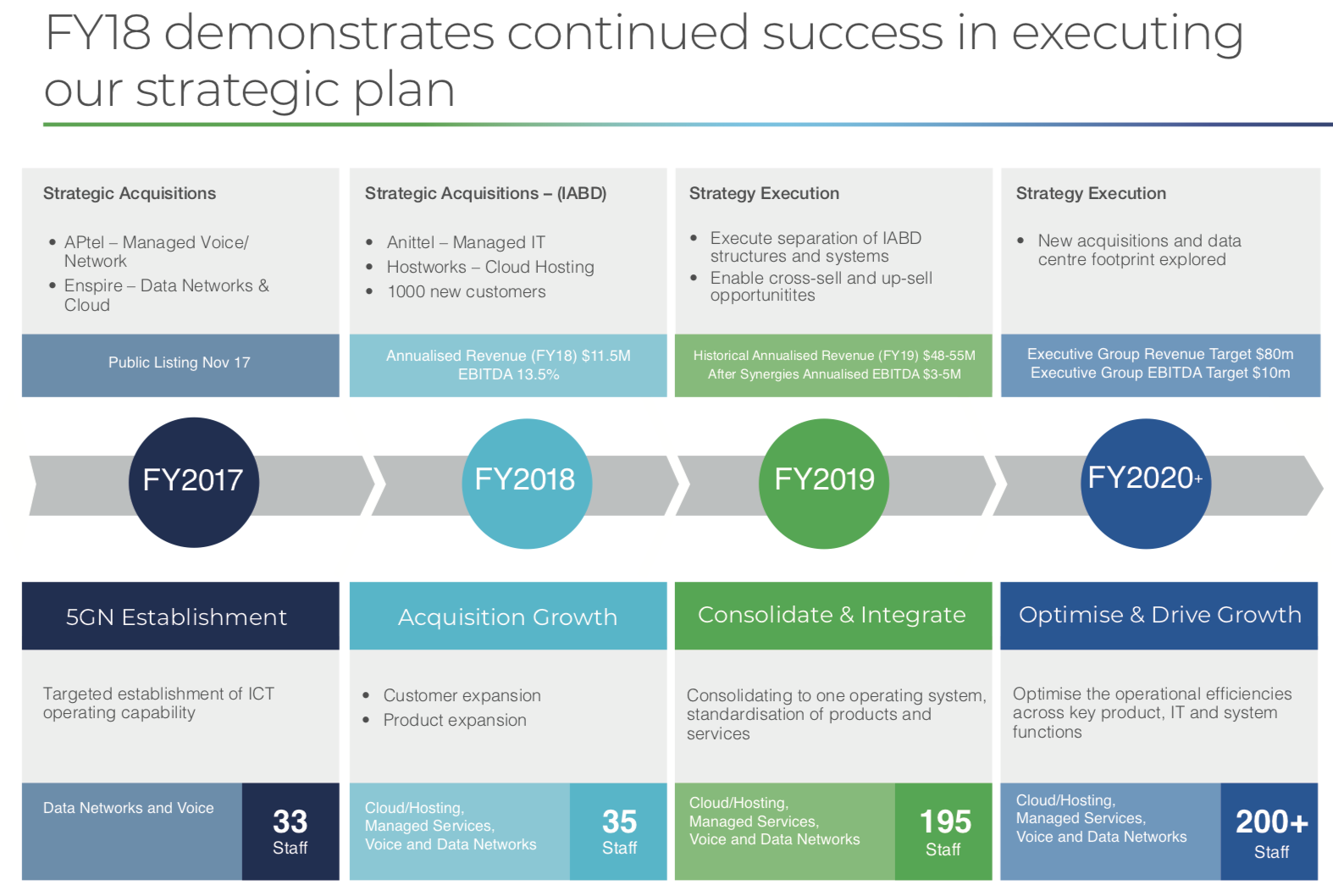

The CEO, Joe Demase, has had previous success with Uecomm (acquired by Optus) and Clever Communications (Big Air) and knows the market well. 5G is his chance to do it all again but this time as the CEO and largest shareholder.

They began by bringing together two Melbourne based businesses in APtel (managed voice) and Enspire (Data Networks & Cloud). This gave them a cash flow positive base to work from and about $11-$12m of revenue.

Then in August they bought IAB’s Direct business, which is a company the Capital H Inception Fund (until very recently) owned shares in and wrote about here. The Indirect business was later bought by MNF Group and I’ll explain in a moment why I think 5G may have gotten a bargain.

The IAB deal is transformative and a key part of 5G’s strategy. They now have annual revenues of well over $50m and a nationwide presence with offices across Australia providing data networking, cloud & hosting and managed services.

They play in the same space as companies like Over The Wire (OTW) and MNF Group (MNF) so there are direct comparables to help the market value the stock. These larger peers trade in a range of 11-15x, compared to 5GN’s 5x, providing plenty of upside should the market take a liking to the story.

They are on track to hit $3-$5m of annualised EBITDA in FY19 as the full synergies from the IAB deal kick in.

The market cap is $21m, the company has about $2-$3m of net debt and runs a relatively capital light business model, outside of select fibre and network deployments, meaning free cash flow should continue to be strong.

Importantly, there is a pipeline of future acquisitions and the vision is to grow 5G into a sizeable mid-market player in the telco space.

A Public Market Model That Works

The core of this thesis is that when a telco roll up strategy is well executed, it can work phenomenally well for shareholders. You don’t have to look too far to see examples - Over the Wire, MNF, Vocus and TPG in the early days.

There are a couple reasons why.

Firstly, there is the multiple arbitrage. Smaller private companies can be acquired for 4-5x EBITDA while the public vehicle will typically trade much higher. 8-10x is very fair if well run but there are many examples of these stocks trading higher once the market starts to believe in their growth outlook.

The shareholders of the public vehicle benefit immediately from this arbitrage and it can be attractive to the vendors too as they can take equity in the transaction and participate in upside that wouldn’t have been possible as a privately owned business.

Second, is the synergies. There are always material synergies in these deals that further increase the extent of the multiple arbitrage. They might acquire on 5x EBITDA but once synergies are realised the multiple might drop to 2-4x.

What is important is that for businesses like 5G these synergies are usually both easily definable and fairly low hanging fruit. You’ve got the obvious in staff overlap and back office/support costs that can be removed each time a new deal is made (this is one reason why IAB Direct’s nationwide presence is important - the infrastructure is already there in future deals to strip out costs faster).

There are cost savings from integrating two networks and negotiating better supplier terms as scale increases. These take a bit longer to kick in, but they can be easily measured and implemented.

You can run services to acquired customers over your own network in what is a low risk way to both boost margins from existing customers but also build out your coverage with a definable ROI from the start. 5G can do this with their fibre network as the business grows over time.

Finally there is cross and up selling between customer bases, which a company like MNF has executed perfectly in the past. You can build out your product and service offering and then sell to what is essentially a captive customer base - provided you keep those customers happy of course - as you are in the best position to offer them the most competitive deal.

This alone can generate good organic top line growth and given the economics of these businesses the operating leverage usually means earnings will outpace revenue.

That’s why this model can work really well. Investors and fund managers know this and so once they have faith in the management team they will usually be more than willing to support the story.

With a supportive investor base the acquisition strategy can then deliver phenomenal returns if well executed.

IAB Direct - Why It Made Sense

Back to 5GN specifically.

In August they bought IAB’s Direct business (Anittel and HostWorks) for $5.7m. A lot of the purchase price was in assumed liabilities (debt and leases), so not much cash actually left the bank.

When they bought it IAB were telling the market the Direct business was breaking even. 5GN removed $1m of executive costs immediately to turn the business profitable and are forecasting $3m EBITDA from this business once full synergies are achieved. That would equate to <2x EBITDA.

Despite what looks like a huge bargain the stock actually sold off on the news of the deal because the market did not appear to have the best feelings towards IAB and that company’s track record, which was reflected in IAB's share price for a long time. Those businesses struggled under IAB ownership and they sold them for a lot less than what they originally paid.

But I think this deal made strategic sense for 5GN and that they got a bargain. As investors know all too well the price you pay is everything and the price 5GN paid here provides a decent margin of safety.

With hindsight, and the MNF deal playing out quite publicly, we can start to see exactly how 5GN may have gotten a good deal.

While the Fund owned IAB on the belief it would sell its Indirect business for a premium, it was impossible to make it a big position. They’d stated in notes to their 2018 Annual Report that from January interest repayments would increase (Note 16, 2018 IAB Annual Report). It seemed touch and go as to whether cash flows would be sufficient to meet these repayments.

But the flip side was it meant IAB would likely need to get a deal done soon. There was impetus for the company to sell itself quickly and they probably couldn’t play the waiting game - in my opinion at least.

The crown jewel of IAB was always the Indirect business. To the IAB management team’s credit they pioneered the concept of offering a full service wholesale telco offering ‘in a box’ to essentially any business that wanted to offer telecommunications to their customers. And they built a dominant position in that market, reinforced by MNF’s strong desire to buy the business.

There were always going to be more suitors for the Indirect business and for a much higher price than Direct. MNF, for example, would have had no interest in the Direct business.

I believe IAB needed to sell the Direct business quickly in order to get the best deal done for their Indirect business.

That appears to have put 5GN in the position to get a good deal. There probably weren’t many other acquirers for which the Direct business made perfect sense, but for 5GN the increase in scale and presence it provided for minimal outlay was attractive.

The 5G business was Melbourne-centric before this deal, but they now have a nationwide presence. That allows them to provide services to larger customers who also have a presence across Australia, expanding the addressable market.

It also greatly increases the scope for new acquisitions and provides the existing infrastructure from which to realise greater synergies from future deals.

For example, if they bought a business in Sydney tomorrow, they could move it into their existing office space, integrate customer service & back office and procure hardware through their existing procurement team. This wasn't possible with the Melbourne centric business pre-deal.

Each additional acquisition from here is now a lot more valuable due to 5GN’s increased scale.

It is this increasing scale that makes the model so attractive. The IAB Direct acquisition brought this scale quickly and at minimal cost.

From an earnings perspective, IAB were previously telling the market that Indirect was doing greater than $50m revenue at 12% margin (implying $6m EBITDA). Yet MNF now state the Indirect business is doing $4.2m of EBITDA, and IAB did not seem to dispute it.

That is a meaningful discrepancy and there hasn't really been much further explanation on the underlying reasons. My best guess is that costs that MNF believe should of been allocated to Indirect were instead allocated to Corporate or Direct. If the latter, it is positive for 5GN's purchase.

The combined business will now do well north of $50m of revenue and up to $5m of EBITDA, making 5GN a meaningful player in their market.

What Are The Catalysts?

There are two things the market will want to see in order to re-rate 5GN from here.

The first is the renewal of acquired customers and signing of new business through up and cross selling, as well as confirmation of the identified synergies being achieved. If this happens it will validate 5GN’s thesis for buying IAB Direct.

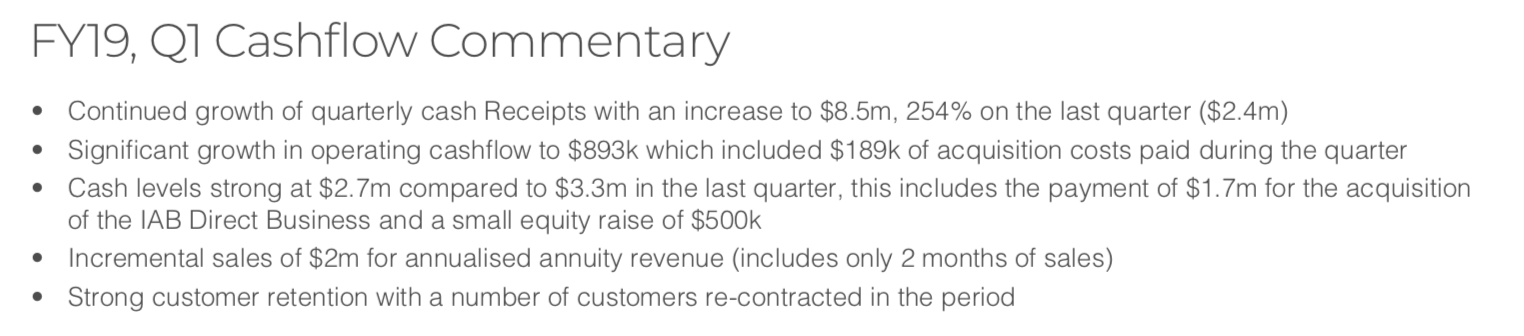

The signs are good so far. The company reported “strong customer retention” and $2m of new business wins in the first 2 months since the deal. Further wins would likely push the stock higher.

The second is free cash flow. They’ve said they expect to continue to generate positive free cash flow and the 4C’s thus far have been strong. The model is reasonably capital light with most of the CAPEX related to growth investments like fibre deployments or hardware to support customer implementations.

All up (both growth and maintenance) I estimate CAPEX will be c.$1.5m pa, allowing for good cash flow conversion.

If they tick those two boxes the market will start to show faith in the strategy and I would expect the share price to re-rate from here, opening up the real growth opportunity through acquisitions.

Building A Mid-Market Telco & Cloud Provider

5GN is trading on ~5x EV/EBITDA once all synergies are achieved and before any further growth.

OTW trades on 14x. MNF on 11x. A smaller example in ST1 trades on an estimated 10-11x.

5GN is trading very cheaply in comparison. If the market wakes up to it there is plenty of upside based on the existing earnings capacity of the business.

But the real upside, as I’ve tried to explain, is through acquisitions over the medium and longer term.

This is where the majority of earnings growth will come from. In their latest presentation they’ve hinted at $10m+ of EBITDA being a medium term target, so the ambitions are large.

They also touched on the possibility of entering the data centre market, and if they do they’ll likely experience multiple expansion given the market’s positivity towards that space, which would be great for shareholders.

The other aspect is that any raise in the medium term for an acquisition is probably going to be at a price higher than the current market price, the same way it was for the IAB deal (60c raise), a reflection of the board owning the bulk of shares and their desire to not dilute at cheap prices.

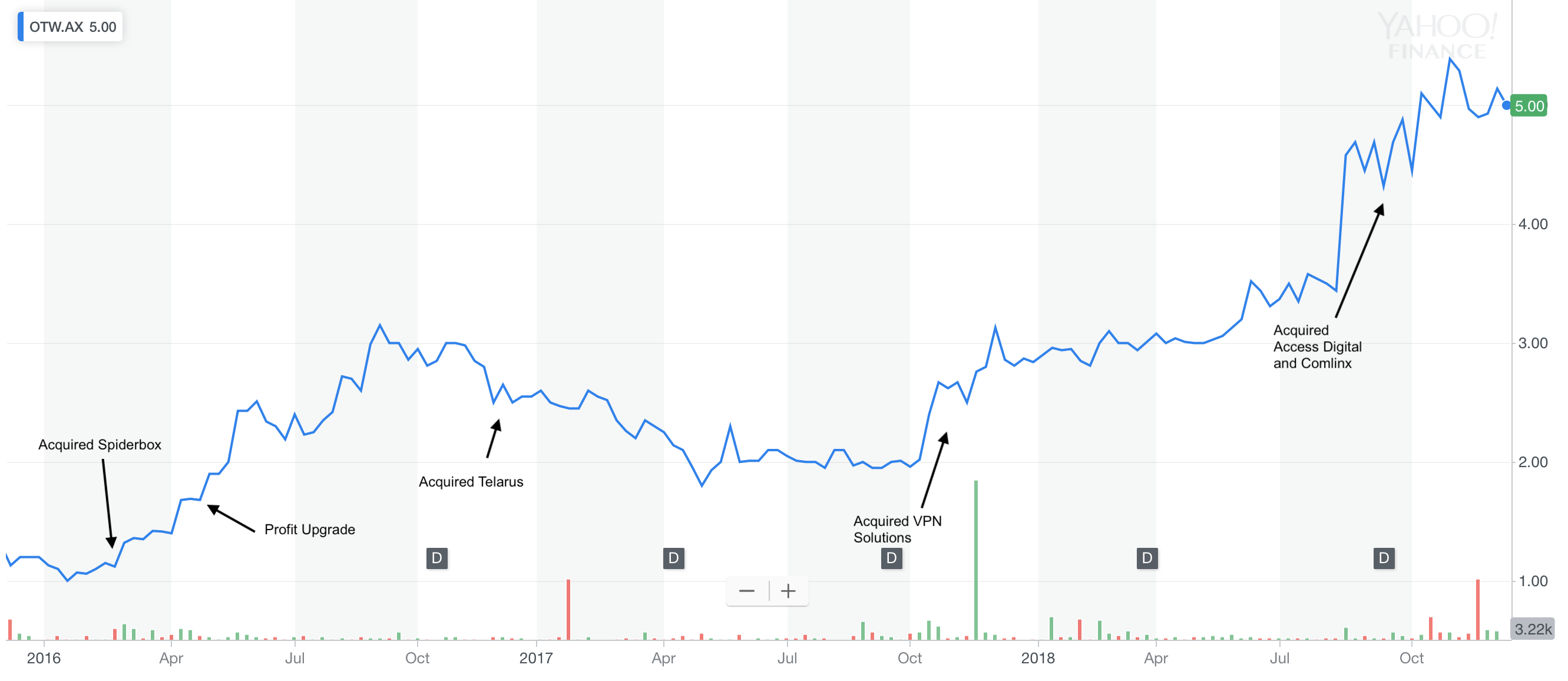

One more point: take a look at the chart below. It is the OTW share price with commentary around the timing of their acquisitions.

Two things to note.

1) Every time they did a deal the share price jumped and then went on another run, outside of 2017 where telcos broadly sold off. They acquired well and the economics of this model are attractive.

2) Before they really got on a run with acquisitions they over delivered on their promises to market (profit upgrade). This built faith in the management team and investors lined up when it came time for them to raise capital to fund deals. The stock eventually went from $1 to $5 in three years.

I could of shown you something similar for a number of other telco roll ups who all began another leg up in their share price each time they completed an acquisition. But OTW is the best comparable with regards to business model and market positioning.

That same opportunity is now in front of 5GN.

If they deliver on their organic growth expectations and successfully integrate IAB Direct then the market will be supportive of future deals. That will lay the groundwork for building a sizeable mid-market telco through acquisitions.

Given the economics of the model, shareholders would have the prospect of some excellent returns.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund.

Previously worked for Pie Funds and Bligh Capital.

2 topics

4 stocks mentioned

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

Comments

Comments

Sign In or Join Free to comment