Global bonds suggest Australia’s yields will go much lower

As a manager of high grade bonds, we are quite amused to see so many comments of late regarding bonds and yields, making it difficult for investors to distinguish myths from realities. Whilst we can see some comments on inflation as rational, we struggle to see how this will equate to rampant inflation in the near term given the obvious slowdown in economies, the second wave of Covid-19 fears, massive debt overhangs around the world, technology driven efficiency, non-unionised work forces, as well as zombie companies producing at their lowest costs to survive. These are just some examples of the newer secular forces driving disinflation currently.

With many viewpoints on the prospect of inflation arriving due to QE4 (the fourth round of quantitative easing established by the US Federal Reserve) and the growth of money supply (M2) to the economy, we believe there is a bigger risk in the near term of disinflationary and deflationary events.

Chair of the US Federal Reserve (the Fed), Jerome Powell admitted in his June commentary, that in 128 months since the financial crisis, the Fed had not met its inflation targets. That is despite QE1, QE2, QE3 (massive M2 growth) and an overall buoyant economy. M2 money recent growth can also partially be explained by the rational of corporates drawing down every single credit line they could in the March and April period, and then parking those funds back into the banking system as deposits, in preparation of the worst case scenario which has not eventuated. Thus, some companies are likely to be paid back via a shrinking M2.

In Australia, the RBA has not hit its inflation target of 2-3% for the entire duration of Governor Lowe’s tenure. RBA deputy Governor Debelle, recently said that it would take at least three years for inflation to be back in its target zone of 2-3%. This means that it would be almost 10 years before the RBA hits one of its two mandates of inflation at 2-3% (full employment being the other, also years away). In order to come close to getting there, the RBA is going to have to put the pedal to the floor!

We suspect the RBA will to have to do a lot more to even come close to reaching those targets. If we turn to New Zealand for guidance, the 2 year and 5 year bonds are negative. Some call New Zealand a leading signal for Australia, and the following chart of Australian and New Zealand 5 year bonds would suggest this is the case.

Is New Zealand leading Australia?

Source: Bloomberg

Source: BloombergSo what does this mean for bonds?

Whilst we are in a truly strange environment with rates seemingly lower in a comparative sense versus what we are used to in Australia, our bonds, on a global basis, look incredibly cheap.

This is why the Australian Office of Financial Management (Australia’s Debt Management Office) is setting record after record, in each new issue it brings to market. This week a 6 year Treasury bond issue had over $82 billion dollars of demand, for a bond that only printed $25 billion dollars.

We are seeing tremendous international demand for our bond market given Australia is one of only a handful of AAA rated sovereigns globally, has a relatively small but growing bond market (thus bigger players can buy without fear of illiquidity), a Westminster system, a free floating currency and a nation situated in the Asian century.

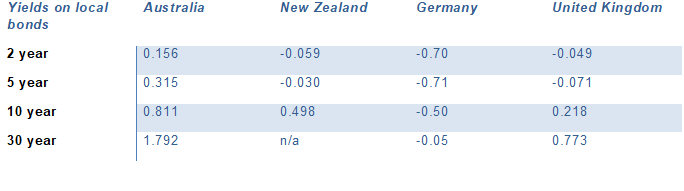

For a greater perspective on where the Australian bond market could go, we can look at comparative bond yields globally, and see what the rest of the world sees. German bond yields are negative out to 30 years.

Source: Bloomberg, Jamieson Coote Bonds analysis.

We have seen recently the complete inability for the bond market to sell-off too far without consequences elsewhere. Look no further than the 15 odd basis point sell-off in US 10 year Treasury bonds on the back of Jackson Hole in late August. The equity market was hit hard, with the NASDAQ (longest duration asset on the planet) down nearly 12% in the aftermath and the US 10 year back at 67 basis points.

One thing we are conscious about and often hear from many is that with bond yields so low and in some nations negative, that calls for a zero return. High grade bonds are not an allocation made for passive income (sadly), but what they do offer is liquidity in tremendous size, the backing of government debt - the best there is and a true diversifier from highly risky credit and equity exposures. Even negative yielding 10 year German bonds rallied ~70 basis points from -16 basis points in January 2020 to -85 basis points in the heights of stress in March 2020.

Like this wire? Let us know by hitting the 'like' button to the left. Or hit the 'follow' button to be notified whenever I post wires.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Angus established Jamieson Coote Bonds with Charlie Jamieson in 2014. He started his career with JPMorgan in London, before working at ANZ and Westpac, where he transacted the first ever Australian Bond trades for several large Asian Central Banks.

........

This information is provided by JamiesonCooteBonds Pty Ltd ACN 165 890 282 AFSL 459018 (‘JCB’) and JamiesonCoote Asset Management Pty Ltd ACN 169 778 189 AR No 1282427. Past performance is not a reliable indicator of future performance. The information is provided only to wholesale or sophisticated investors as defined by the Corporations Act 2001 (Cth). Neither JCB nor JCAM is licensed in Australia to provide financial product advice or other financial services to retail investors. This information should not be considered advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling units and does not take into account your particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice.

4 topics

Angus established Jamieson Coote Bonds with Charlie Jamieson in 2014. He started his career with JPMorgan in London, before working at ANZ and Westpac, where he transacted the first ever Australian Bond trades for several large Asian Central Banks.

Expertise

Angus established Jamieson Coote Bonds with Charlie Jamieson in 2014. He started his career with JPMorgan in London, before working at ANZ and Westpac, where he transacted the first ever Australian Bond trades for several large Asian Central Banks.

Expertise

Comments

Comments

Sign In or Join Free to comment