GMG: the future of warehousing

Julia Weng

Paradice Investment Management

Warehouses have come a long way from being dirty sheds in the middle of nowhere. Today, highly automated warehouses are occupying populous urban locations and powering a world hungry for convenience and speed.

Goodman Group (ASX: GMG) is riding this wave of warehouse evolution, and what we consider to be a best-in-class global developer of logistics real estate. With the business having risen 125% over the past 3 years (vs +9% for the ASX200) and now trading at 27x FY22 P/E, we revisit GMG to determine whether it remains a good investment.

First, a few "fun facts" about warehouses:

- The average Amazon warehouse spans one-third of a square mile and is about the size of 60 football fields (100,000 square metres). Amazon today has 175 fulfilment centres around the world, and currently has requests for proposals (RFPs) for 100 warehouses in Europe alone.

- The number of robotic warehouses is expected to grow by more than 1200% by 2025 (~240% pa). Amazon alone has an army of 200,000 robots in its fulfilment centres today roaming across thousands of QR codes to pick and pack products.

- Hong Kong currently has the world’s tallest warehouse at 24 storeys spanning across 223k sqm of warehouse space. Built by Goodman in 2012, the first 15 floors are fully accessible by vehicles and the remainder by goods lifts. The first vertical warehouse is being considered in Australia over the next 3-4 years as centrally located sites are in short supply.

The era of digitisation fuelling an acceleration of growth

There is little doubt that COVID has accelerated e-commerce penetration and provided a catalyst for retailers and transport providers to reassess their optimal strategy and supply chain solution. Global e-commerce penetration was at 14% in 2019 and had been growing about 1ppt a year; fast forward 9 months, and e-commerce penetration was estimated to be 20% as of 3Q20. Even China and Korea, which already boasted the world's highest eCommerce penetration rates at 27-30%, saw another surge of 3-5ppt. The ceiling remains untested at this point in time. While we're likely to see online sales growth slow from here, we know that retailers were underprepared and underinvested, and the catchup will likely be a multi-year investment.

The e-commerce growth curve is steepening around new categories and new cohorts in particular. A sizeable segment of consumers – for example, elderly people – who previously resisted online shopping are enjoying the newfound convenience. Consumer staples and household products, previously laggards of the e-commerce take-up, are likely to witness continued growth, fuelling an acceleration of warehouse developments.

Growth is not just about e-commerce sales

We also consider other aspects contributing to warehouse requirements:

- The multiplier effect of e-commerce sales - Each square metre of retail space equates to 3 square metres of warehouse space required given higher delivery efficiency requirements.

- Our definition of "fast shipping" has changed. What was perceived to be fast shipping, usually around five to seven days, is now same or next day delivery. As such, proximity to the end-customer is paramount.

- Growth in click & collect means retailers need a warehouse much closer to each storefront, increasing the importance of location.

- Time spent sitting in traffic - increasing road congestion means that location and access to alternate transport networks are increasingly important.

- Warehouse rents are less than 5% of supply chain cost, compared to transport which accounts for 50% of supply chain cost. Even if rents increase by 5-15%, there may still be savings in the form of reduced transport costs and better access to labour.

- COVID has shone the spotlight on supply chain resilience. With just-in-time (JIT), inventory-to-sales has fallen to the lowest levels on record, and many retailers are operating with razor-thin inventories and caught out by demand volatility. Rent is typically only 25-30bps of end sales value. The retailer is much better off having slightly larger warehouses than losing the product margin from not having the product available.

Acceleration of the development pipeline is evident in GMG’s work-in-progress (WIP) increasing from $4.1b as at Jun 2019, to $6.5b in June 2020, and now expected to increase to more than $8b by June 2021. With projects increasing in size and complexity, this level of WIP underpins at least 2-3 years of earnings visibility.

Not all warehouses are created equal

- Location, location, location - it is interesting to see that western Sydney rents have remained mostly unchanged over the 3 years and incentives have increased, whilst rents in south Sydney and inner Melbourne have escalated by 5-10% pa over the same period.

- Similarly, rents in Toronto, New Jersey, Southern California and Seattle rose by 12-18% in 2019, exceeding CPI escalators and rest of North America.

- There is little correlation between supply and demand in last-mile logistics, with scarcity in developable sites that can reach $500m annual income within 1 hour of delivery continuing to put upward pressure on rents.

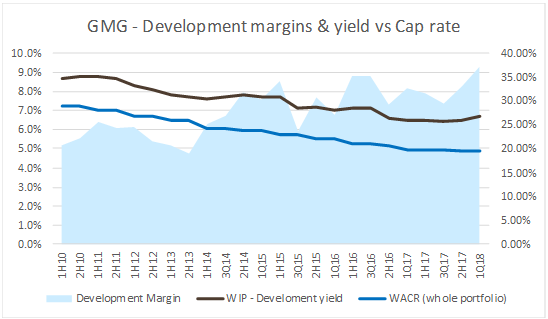

GMG's competitive advantage is its ability to anticipate customer demands 5-10 years in advance, acquire income-producing land and selectively choose more complex projects, requiring multi-year permits and approval processes. The quality of GMG's builds is perhaps most evident in its ability to increase development margins over the last 10 years. Even as bond yields have declined, GMG's development margins have increased to 25-35%.

Source: Company reports, Paradice

A capital-lite model affords high ROE

Unlike most developers, GMG runs a self-funding and capital-light structure where GMG typically funds 20-30% of investment capital. GMG shares the upside of development profit and property revaluation with its capital partners (mostly pension funds), and in turn, earns a base and performance fee akin to a fund manager.

When we look at the entire value chain (development, funds management and rent collection) over a 15-year period, which is the average term of a new lease, we estimate GMG can earn 18-25% ROE which places it within the top decile of the ASX200. This is even more impressive when considering it has consistently de-geared over the years - gearing was 7.5%, and 20% on a look-through basis in FY20.

Conclusion

GMG has all the ingredients we look for in a portfolio holding - strong defensive and growth attributes, healthy balance sheet and earnings visibility, and yet trades a small discount to ASX industrials.

Clients and performance come first

The Paradice difference comes down to accountability, alignment, experience and performance. Click the 'FOLLOW' button below for more of our insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Julia is a Portfolio Manager / Analyst in the Paradice large caps team.

Featuring

Julia Weng,

Paradice Investment Management

Julia is a Portfolio Manager / Analyst in the Paradice large caps team.

........

This material has been prepared by Paradice Investment Management Pty Ltd (ABN 64 090 148 619, AFSL No. 224158) (“Paradice”). This material is not intended to constitute advertising or advice (including legal, tax or investment advice) of any kind. It is of a general nature only and has been prepared on the understanding that Paradice is not providing professional advice on a particular matter. The information and opinions contained herein are not necessarily all-inclusive and, as such, no representation or warranty, express or implied, is made as to the accuracy, completeness or reasonableness of any assumption contained herein and no responsibility arising for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Paradice, its officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Before relying on the material or making any decision in relation to the funds, you should consider your needs and objectives, consult with a licensed financial adviser and obtain a copy of the relevant product disclosure statement, which is available by visiting www.paradice.com. Past performance is not a reliable indicator of future performance. The value of an investment in the funds may rise or fall. Returns are not guaranteed by any person.

2 topics

1 stock mentioned

Julia Weng

Portfolio Manager

Paradice Investment Management

Julia is a Portfolio Manager / Analyst in the Paradice large caps team.

Expertise

Comments

Comments

Sign In or Join Free to comment