Gold stocks to buy on the back of stalling US policy and growth

Foster Stockbroking

Stockbroker

Heightened expectations of US growth are fading in light of no new economic data to suggest the promised fillip. The efforts of the new Trump administration continue to be frustrated on a number of fronts and cannot point to any meaningful progress so far (Obamacare repeal, debt ceiling, and other self-inflicted distractions). Global markets have been patient so far on US policy implementation, but who knows for how much longer? There appears to be a dawning realisation that progress on any policy front in the US will be slow, if at all, as demonstrated by the failed Obamacare repeal attempt.

The US dollar Index has fallen 1.8% since the start of the year, despite a very brief recovery through February. Markets are no longer as certain of further rate increases during the year, and the slower than expected US rate hike cycle will be supportive of gold prices in the near term.

Recent dovish statements and March minutes from the US Fed have dampened expectations of the expected three rate increases in the US this year and revealed concerns of an overvalued US equities market. 10 year US Treasury bond yields have fallen in the past fortnight, while the yield curve spread between 10-year and 2-year Treasuries have narrowed ~30bps to 2.3%.

Current volatility (VIX 12.39) remains low compared to historical levels (10 year average of 20.70), and with the above headwinds, we believe gold is the way to hedge against USD weakness and slowing US growth.

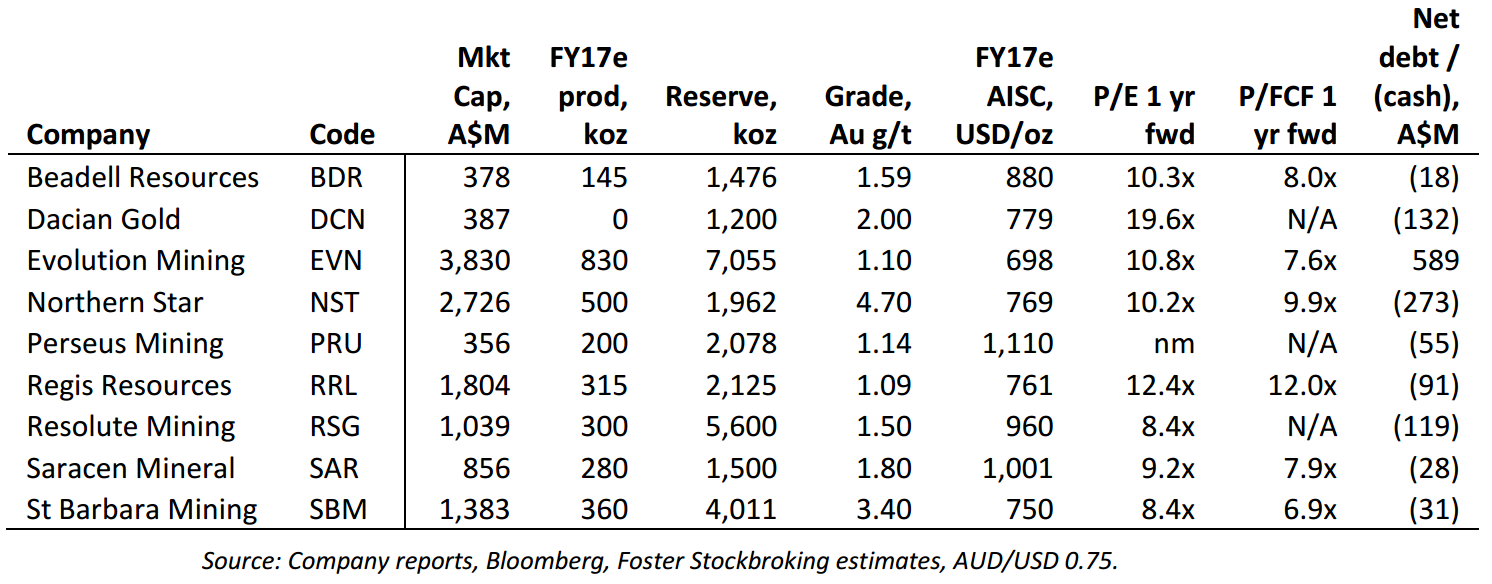

We recommend a basket of gold equities from the following companies:

- Beadell Resources,

- Dacian Gold,

- Evolution Mining,

- Northern Star Resources,

- Perseus Mining,

- Regis Resources,

- Resolute Mining,

- Saracen Mineral, and

- St Barbara Mining.

We have included a table of junior and intermediate ASX listed gold miners that are an attractive way to play the theme, given the recent pullback in domestic gold stock prices, and relative value across the space.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Providing investment strategies, research and ideas to institutional and professional investors since 1991, with a primary focus on emerging Australian companies.

8 stocks mentioned

Foster Stockbroking

Stockbroker

Providing investment strategies, research and ideas to institutional and professional investors since 1991, with a primary focus on emerging Australian companies.

Expertise

Foster Stockbroking

Stockbroker

Providing investment strategies, research and ideas to institutional and professional investors since 1991, with a primary focus on emerging Australian companies.

Expertise

Comments

Comments

Sign In or Join Free to comment