Government policy shifts drive EV demand

Our EV thematic has been discussed in previous articles, most recently in February 2017. Given the major developments in this space during September, we felt it timely to provide another update.

EV’s mass-market rollout plans continue unabated. In September, China, the largest automobile market and a third of the global automobile market, announced plans to transition to full EV. This policy shift, likely to be enforced by 2030, signals China’s seriousness to address pollution levels. India, the fifth largest automobile market, indicated its plan to move to full EV by 2030. Other countries are also looking to eliminate internal combustion engines (ICE) and to only sell EV; for example, Norway moving to full EV by 2025 and France and the UK banning ICE sales by 2040. The governor of California also announced it is looking at banning ICE sales.

In addition to these policy announcements, Volkswagen backed up its US$80b EV investment with a tender for long-term supply for Cobalt, highlighting the need to build up an entirely new supply chain. Daimler also announced a US$1b investment in an EV plant in the US. Volkswagen plans to add electric or electrified versions of all 300 models of cars it manufactures by 2030. Many other auto manufacturers are making similar statements e.g. Volvo, BMW, Mercedes, GM, etc.

September also saw the first auto manufacturer, China’s Great Wall (US$18b market cap) make an upstream investment in Lithium production to secure supply of the critical raw material ingredient. Great Wall is investing in Pilbara Minerals’ greenfield project in WA for its stage 2 expansion. Note. Pilbara’s stage 1 is currently under construction. This development has significant implications for the sector. It is likely to be the first of many upstream investments made by downstream players, namely auto manufacturers, in order to secure raw material supply. We’ve been anticipating this for some time, similar to the market dynamics witnessed in the 2003-2011 Iron Ore bull market. Great Wall’s move will likely see similar moves by European auto manufacturers looking to secure Lithium and Cobalt supply. This bodes very well for our investments, particularly Kidman, which should be able to fund their 50% share of the capex for the Mt Holland integrated-project JV on favourable terms.

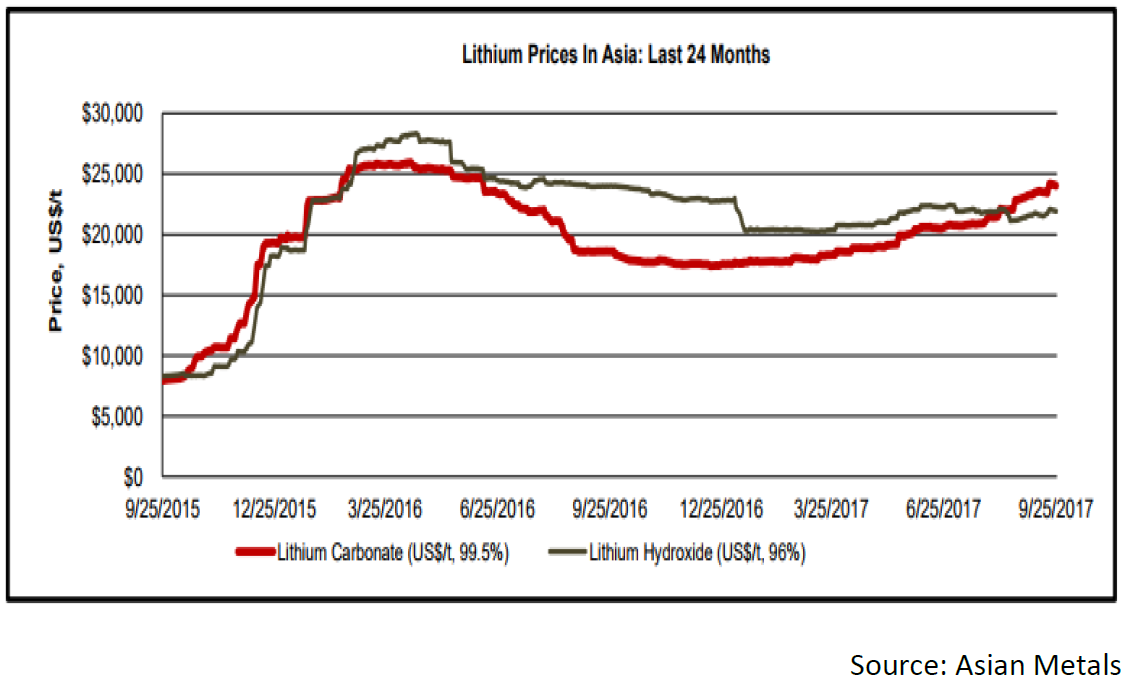

We continue to closely follow and model both demand and supply, remaining constructive on the fundamentals for both Lithium and Cobalt over the medium to long-term. As expected, Lithium and Cobalt prices have continued to strengthen.

Lithium demand has continued to surprise to the upside (was 7-10% CAGR, currently 15-20% CAGR) which has been driven by growth in EVs. The supply response is underway, albeit likely to experience difficulties and delays, which ultimately will be absorbed by the strong global Lithium demand. Cobalt demand growth is expected to be >10% CAGR with an even more challenging supply response than Lithium.

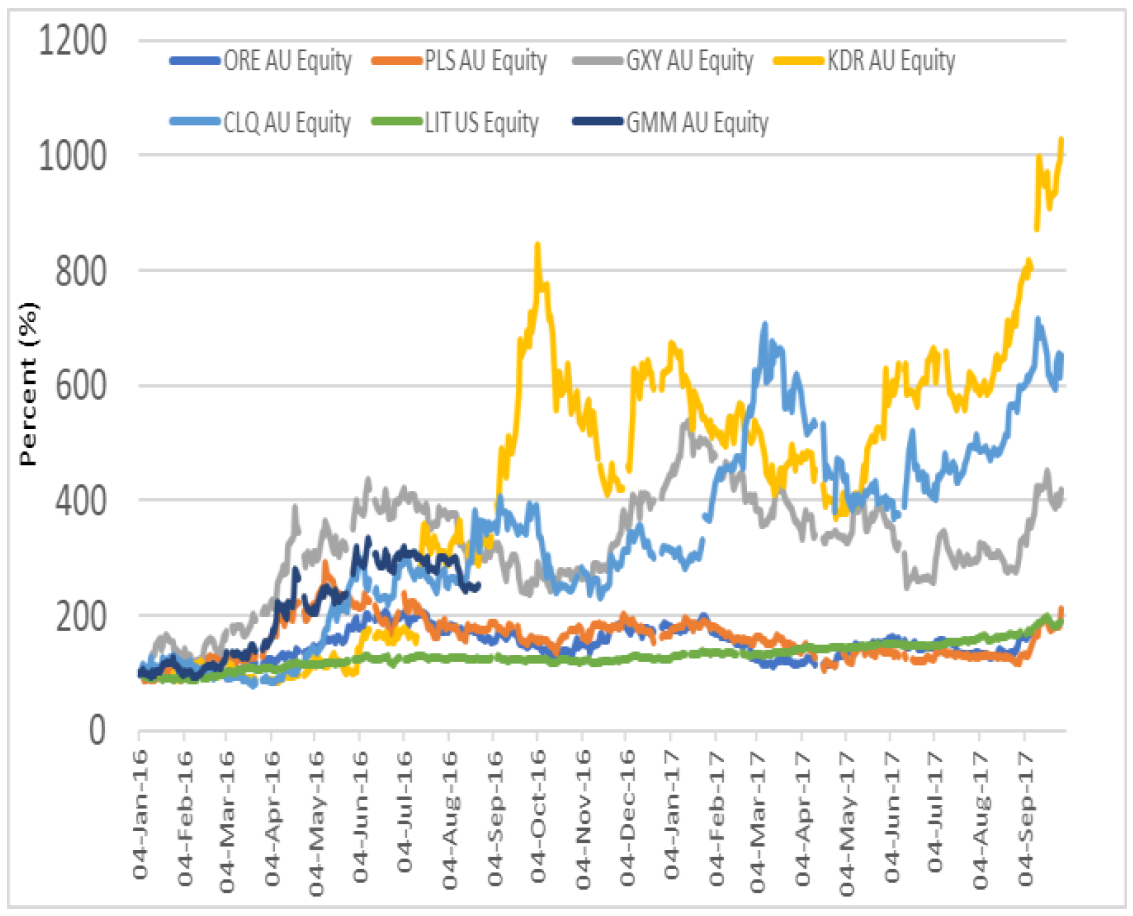

We are now seeing wider acceptance of the EV thematic, and recognise we have been earlier than most due to our unique process and deep research effort. Our EV theme has been the Fund’s best contributor to date and in our view, remains in its infancy. Paragon’s stock picks exposed to the EV theme are charted below against the global benchmark Global X Lithium & Battery Materials ETF (NYSE: LIT US; green line).

We’re currently long Orocobre, Kidman and Global Geoscience (Lithium), Cleanteq and European Cobalt (Cobalt), Lynas (Rare Earths) and Talga (Graphene).

While we expect Lithium and Cobalt to continue to perform strongly, it is equally as exciting to consider the growth opportunities with other EV-related raw material inputs which we forecast will experience bull markets as follows:

- 2017+ Lithium / Cobalt

- 2018+ Copper

- 2019+ Possibly Graphite / Graphene

- 2021+ Possibly Nickel (last due to massive industry surpluses that need to unwind)

We will be well positioned in these sub sectors (second derivatives of our EV theme) ahead of them playing out.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

John co-founded Paragon in 2012 and became principal and majority shareholder from 2017. John is responsible for executing the investment strategy and managing the Paragon Australian Long Short Fund.

John has had 16 years in financial markets, including the last 8 years at Paragon, 4 years at a global resources absolute return fund where he was solely dedicated to the Australian long/short component of the fund, and 4 years on the sell-side which included heading Industrials research.

4 topics

6 stocks mentioned

John co-founded Paragon in 2012 and became principal and majority shareholder from 2017. John is responsible for executing the investment strategy and managing the Paragon Australian Long Short Fund. John has had 16 years in financial markets,...

Expertise

John co-founded Paragon in 2012 and became principal and majority shareholder from 2017. John is responsible for executing the investment strategy and managing the Paragon Australian Long Short Fund. John has had 16 years in financial markets,...

Expertise

Comments

Comments

Sign In or Join Free to comment