Growth vs Value in Australian Small Caps

Growth vs value is a well-documented discussion in stock investing. It describes two fundamental approaches or styles to investing where in a basic sense, the growth approach seeks to invest in companies that exhibit strong growth characteristics (whether this be in the sales, earnings and/or cash flow of a company), while the value approach seeks to invest in stocks that are undervalued (based on several measures including a low price to earnings (P/E) ratio, low price to book (P/B) ratio or high dividend yield etc). These measures aren’t exhaustive and different investors will have their preferred metrics. Our belief is that a focus on growth when investing in small companies delivers superior returns.

Growth is the best approach to Australian Small Caps

To us, this is intuitive since small companies typically strive to become larger companies over time. They aspire to grow – finding the ones that have a sensible growth strategy in place with competent management who can execute on the strategy is the challenge that we face as investors.

There are three ways that a company can grow:

- First is organic growth which is clearly the most desirable and sustainable, whereby companies look to grow by reinvesting profits back into the business. In the right sort of business (where the reinvestment generates decent returns), this type of growth can drive earnings and hence the valuation of a company over many years.

- Second, companies can grow by making acquisitions. This can provide scale and/or capability to a business but typically also increases the risk profile.

- Finally, a company’s growth can be driven by cyclical factors, but this is usually shorter duration in nature and investors need to understand these finite cycles to generate investment returns.

We acknowledge the value approach has significant merit (no one wants to overpay for a stock!). It essentially seeks to pay a price for a stock that is a discount to the intrinsic value. This value can be measured in a number of ways.

The reason for the discount can be many – perhaps a company has fallen out of favour for some reason despite exhibiting solid fundamentals, or maybe a company is yet to be fully recognised by investors. A ‘margin of safety’ is sought, and the intrinsic value of a stock should be realised with the passage of time.

The data supports a growth approach

It’s our contention however that a growth approach to small companies investing delivers superior returns to the investor over the medium to long-term. While past performance is no guarantee of future performance, it can be instructive.

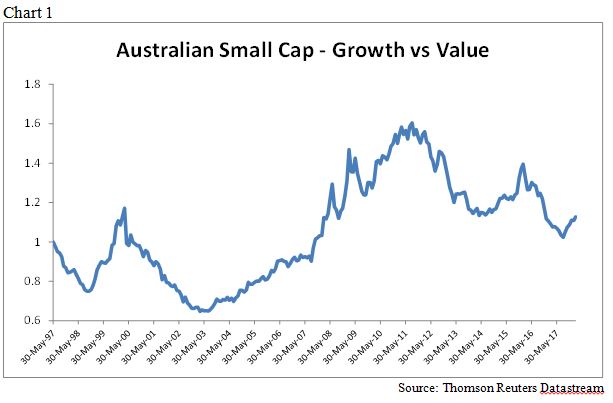

Focusing on the Australian market, Chart 1 shows the performance of the MSCI Australia Small Cap Growth index versus the MSCI Australia Small Cap Value index since the inception of the two indices over 20 years ago. While there have been periods when a particular style has been in favour, the growth approach has yielded outperformance in the Australian small cap market over the long-term.

NB all charts below are based on total returns (which includes dividends). Chart 1 has been rebased to 1, with an increasing unit indicating outperformance in growth, and a decreasing unit indicating outperformance in value.

Chart 1 shows that the quantum of the cumulative returns has been superior for the growth style in the Australian small cap market i.e. the current value is >1.

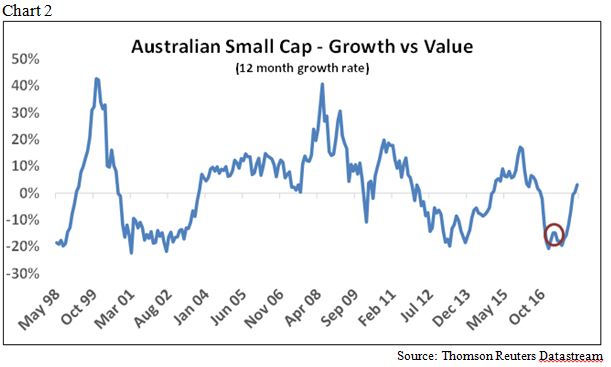

In addition, when reviewing the series plotted for a rolling 12-month return (Chart 2), growth remains positive ~60% of the time over the time series (a reading greater than 0% in the chart). This illustrates that as a signal, growth has a material rate in the small company’s universe.

The key conclusion is that a focus on growth when investing in small companies delivers superior results for investors over the medium to long-term.

Clearly, the outperformance of a particular style will vary depending on which point of the cycle we are in, however over longer periods, an investment style based on growth in this part of the market has great merit.

Look out for extremes!

When we originally did this analysis in April 2017, we observed that Growth stocks had dramatically underperformed in the preceding 18 month period, and that we were at 20-year extreme levels (circled in Chart 2 above). There was no particularly good reason for this, so it was our expectation that a reversal would occur with growth stocks to outperform strongly given compelling valuation and price signals. Pleasingly, this has occurred in the last 10 months.

As a final thought, while Chart 2 suggests we are no longer at extreme levels, the current neutral level still bodes well for growth stocks going forward as they have historically outperformed Value stocks ~60% of the time.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Naheed is Deputy PM of the Flinders Emerging Companies Fund which provides investors with an actively managed portfolio of listed small and emerging Australian companies, and is one of the top investment managers in the space.

3 topics

Naheed is Deputy PM of the Flinders Emerging Companies Fund which provides investors with an actively managed portfolio of listed small and emerging Australian companies, and is one of the top investment managers in the space.

Expertise

Naheed is Deputy PM of the Flinders Emerging Companies Fund which provides investors with an actively managed portfolio of listed small and emerging Australian companies, and is one of the top investment managers in the space.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management