Have the e-commerce stocks run too hard, too fast?

Markets have a common habit of getting far too excited on both the upside and downside, a phenomenon we often describe as stretching the elastic band of optimism / pessimism too far with the inevitable reaction i.e. complacent investors in either direction is a dangerous thing. This doesn’t mean that the market in question is in trouble fundamentally just that prices get pushed too far and often too fast – something that is generally obvious in hindsight.

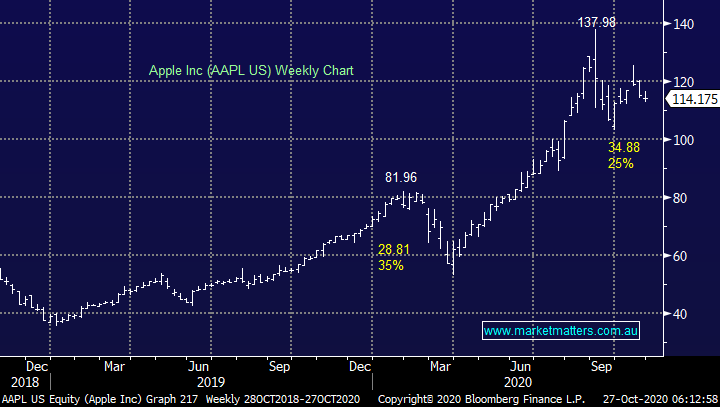

Apple (AAPL US) is a great example of this, it fell 35% in March like many stocks but it’s follow up 25% correction in recent weeks has been fuelled by investors chasing the stock too hard following its stock spilt which added zero fundamental value to the company / stock i.e. there’s no logical reason to have pushed AAPL up ~40% on the news of a stock split hence “value investors” appeared to have taken some much loved profits in what’s clearly been a challenging year, however they will be probably be lurking on the bid into weakness – sell high buy low sounds great when it plays out.

Apple Inc (AAPL US) Chart

One of my favourite quotes around this market characteristic is from legendary investor Baron Rothschild who was clearly more than happy to sell a stock / sector when it became too frothy comfortable in the knowledge he would miss out on some of the upside to avoid a potential sharp correction looming on the horizon.

“I never buy at the bottom and I always sell too soon”

Another couple of examples has been gold which was dominating the press mid-year before correcting over $US200/oz and CSL Ltd (CSL) just after March – if everyone’s long it doesn’t matter how good the story / rhetoric, a dearth of fresh buying is likely to be around the corner.

Gold ($US/oz) Chart

CSL Ltd (CSL) Chart

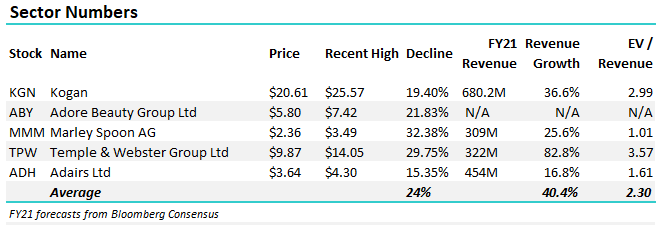

As we mentioned earlier the e-commerce stocks have endured a tough few days, today’s report is considering whether we should buy, sell or hold some of the most successful stories of 2020. We’ve touched on 5 in total which already illustrates how quickly the space has grown.

The table here looks at some broad numbers to give a sense of the 5 stocks we cover. The average pullback is 24% which is deep, while the consensus revenue growth for FY21 is +40% with upside potential when analysts publish forecasts for ABY which is growing revenue at 70%.

We saw similar aggressive selling in the BNPL space in late August only for Afterpay (APT) to regain its mojo and make fresh all-time highs whereas some of the smaller players struggled to scale their same heights – we wouldn’t be surprised to see a similar reaction in the e-commerce stocks with a clear migration to quality as opposed to buying the sector collectively

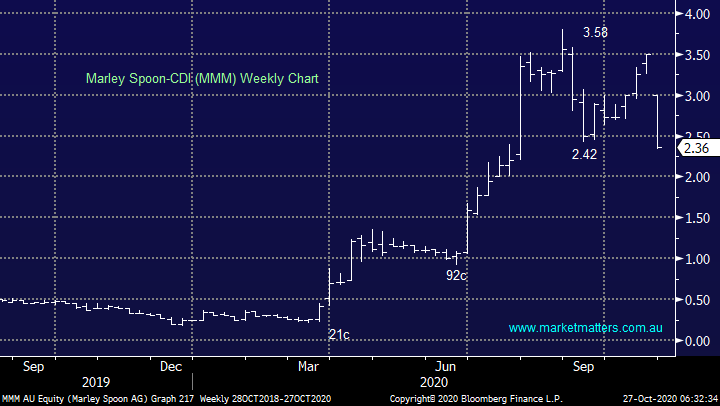

1. Marley Spoon (MMM) $2.36

Last week Marley Spoon (MMM) “tapped the market” for $56m in a quick / opportunistic capital raise to fund growth following the stocks huge appreciation post the pandemic. The placement was at $3.22 and was well oversubscribed, today the stocks 26% lower and the buyers have vanished. The herd has gone from buying to sitting on their hands in just a few days, when they decide to buy again it might be a scramble to get set.

The sectors clearly gone through a short-term valuation downgrade as investors have flocked to the sideline ahead of the US election with MMM’s capital raise certainly one of the catalysts for the stampede, while it might take a while for MMM to challenge $4 we believe from a risk / reward perspective the current pullback towards $2 is a buying opportunity for the brave.

MM likes MMM into current weakness.

Marley Spoon (MMM) Chart

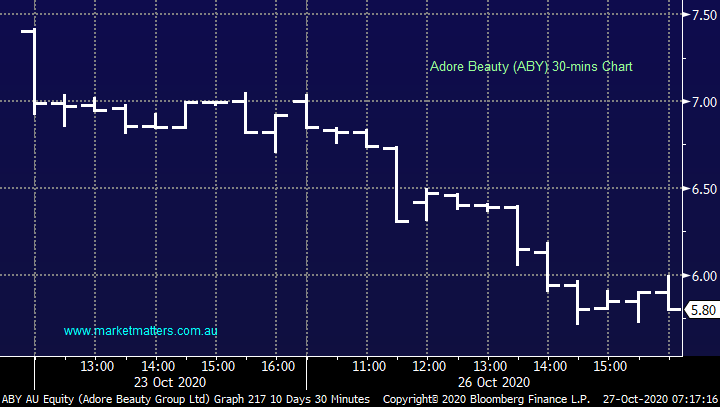

2. Adore Beauty (ABY) $5.80

ABY was smacked over 16% yesterday following the sector lower, disappointingly closing well below its $6,75 listing price just last Friday – another perfect illustration of how quickly e-commerce has moved out of favour, at one stage it was trading around a 10% premium to its raise price following a heavily oversubscribed IPO. Having been involved in the process, the demand was very strong, yesterday the stock was struggling to capture a bid ~10% lower, clearly a massive change in market sentiment.

As we suggested yesterday afternoon, the selling was aggressive however that was the theme right across the space. Simply put, we’ve seen indiscriminate de-risking of e-commerce stocks and when momentum traders are a major player in a stock / sector, moves can become hard and sharp.

We still like ABY, it’s a great business but it comes down to what valuation the market is prepared to place on the sector. As we wrote on the morning of listing last week, while this is clearly an expensive stock, if the market focusses on quality, then it should do well – on Monday the market focussed on valuation across the sector.

MM likes ABY as an accumulation into weakness.

Adore Beauty (ABY) Chart

3. Temple & Webster (TPW) $9.87

Temple & Webster (TPW) traded above $14 last week, only to close ~30% lower yesterday, the stock started its decline after its AGM last week failed to live up to investor expectations. The comments from the CEO were outstanding – revenue up 138% for the period to 19 October, EBITDA for the first quarter at $8.6m already ahead of the whole of FY20. The comments have a similar tone to those made at the full year result back in July where the company flagged a quick start to the year. Unfortunately the market had extrapolated these comments to mean that growth on growth would accelerate through the year – and while there is no real sign growth has slowed, it hasn’t picked up pace either i.e. optimism had gone too far.

We simply believe TPW was a crowded trade and a very similar story to the whole sector in recent sessions – remember herd mentality indiscriminate selling creates opportunity, and TPW is approaching the level that we are becoming increasingly interested.

MM likes TPW, ideally around $9.

Temple & Webster (TPW) Chart

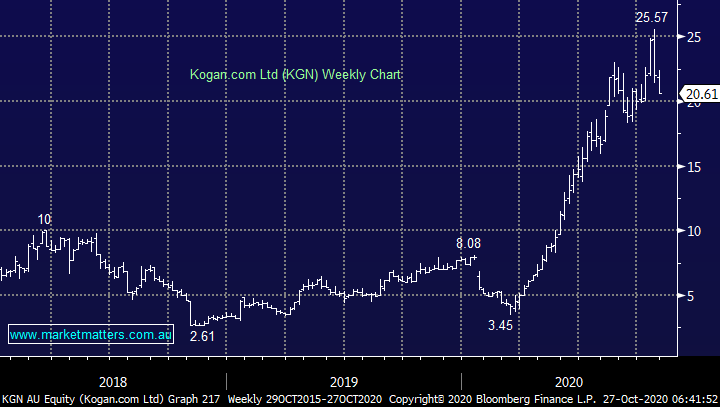

4. Kogan.com Ltd (KGN) $20.61

KGN has been a volatile stock over the years with lots of noise around founder sell-downs, granting of options and the like, however share prices follow earnings, or in the case of growth stocks, top line growth and KGN has been apt in continuing to deliver and innovate to achieve strong growth.

After the stocks soared more than $20 in 2020 a few months consolidation feels almost inevitable.

MM likes KGN around $18.

Kogan.com Ltd (KGN) Chart

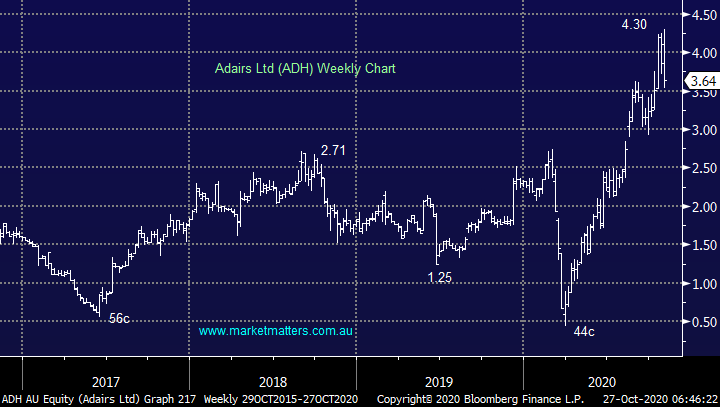

5. Adairs (ADH) $3.64

While not an outright e-commerce company with a large footprint of stores around the country, they have garnered attention due to strong growth in online sales and phenomenal success of their subscription model, something others will no doubt replicate.

While ADH have not grown sales at the dizzying heights of others, they are more established and trade on a fairly conservative P/E of 13.7x, cheap when sales are topped to grow 17% in FY21.

This is another stock we like on the back foot but we should remain cognisant that markets have a habit of pulling back aggressively when everyone disembarks the train at once.

MM likes ADH nearer $3.40.

Adairs (ADH) Chart

Conclusion

MM believes we only have to look at Amazon (AMZN US) to understand that quality e-commerce businesses are the future and they will command high valuations as they grow strongly, we believe the current pullback in the Australian group as an ideal opportunity to accumulate / establish a holding in the larger more established sector names.

Get regular market updates

At Market Matters, we write a straight-talking, concise, twice daily note about our experiences, the stocks we like, the stocks we don’t, the themes that you should be across and the risks as we see them. Click here for your free trial.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

........

Any advice provided is of a general nature only.

1 topic

6 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment