TOL - 24th Nov, 2020

House prices rise again in November after October gains

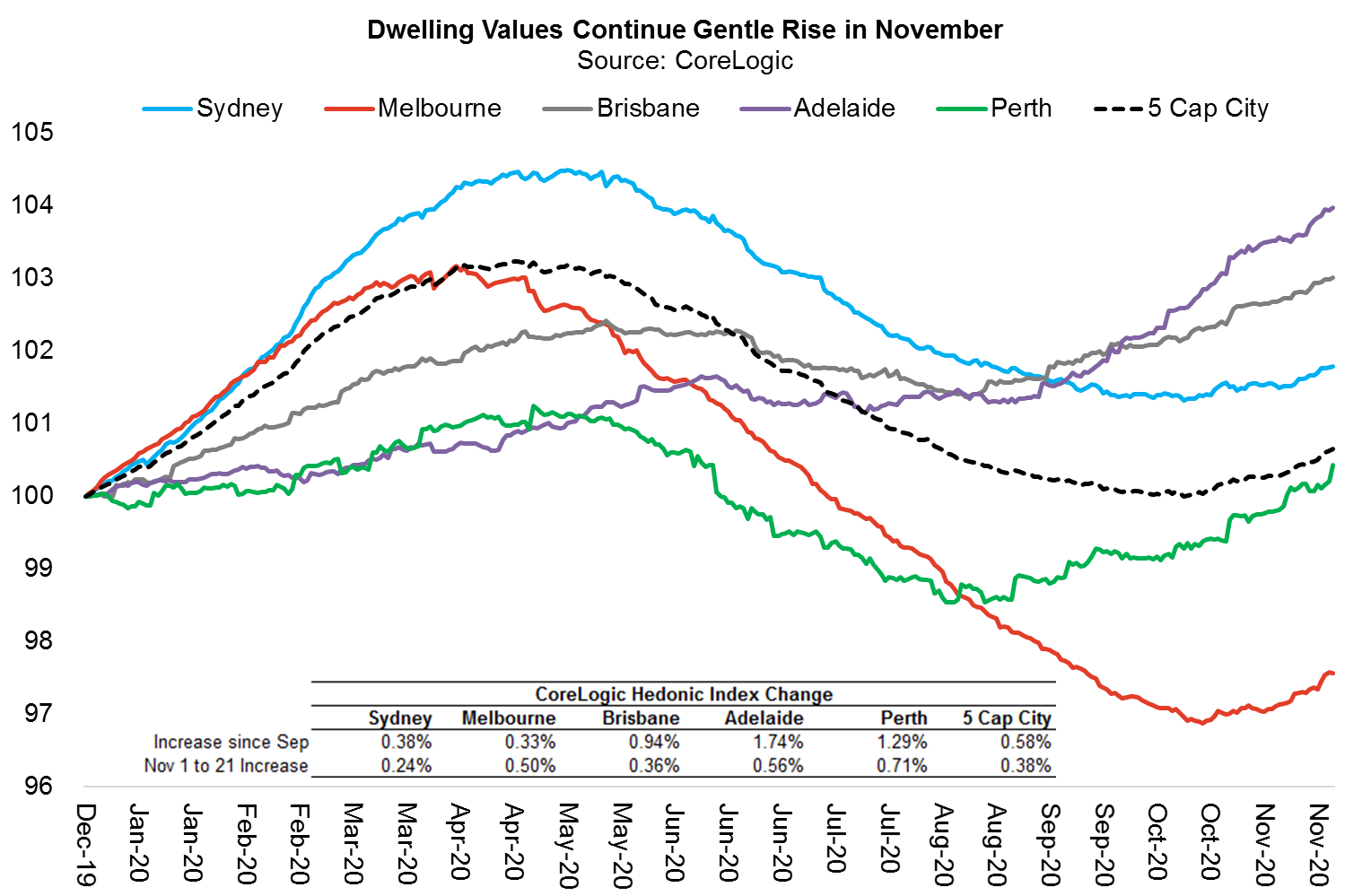

Further to our little note about the extinction of housing bears as a species, Australian dwelling values have continued to climb higher in the month of November to date. Over the first 21 days of the month, house prices---technically dwelling values (ie, including both apartments and houses)---across the five largest capital cities have appreciated 0.4% led by Perth (0.7%), Adelaide (0.6%), Melbourne (0.5%), Brisbane (0.4%) and Sydney (0.2%) according to the latest daily hedonic index data from CoreLogic.*

After prices started drifting lower in late April and May (with a tiny peak-to-trough correction of 2.8% in metro markets and 1.7% across all metro and non-metro regions), the Aussie housing rebound commenced in September in six of the eight capital cities. The bounce-back picked up steam in October with all cities except Melbourne realising gains.

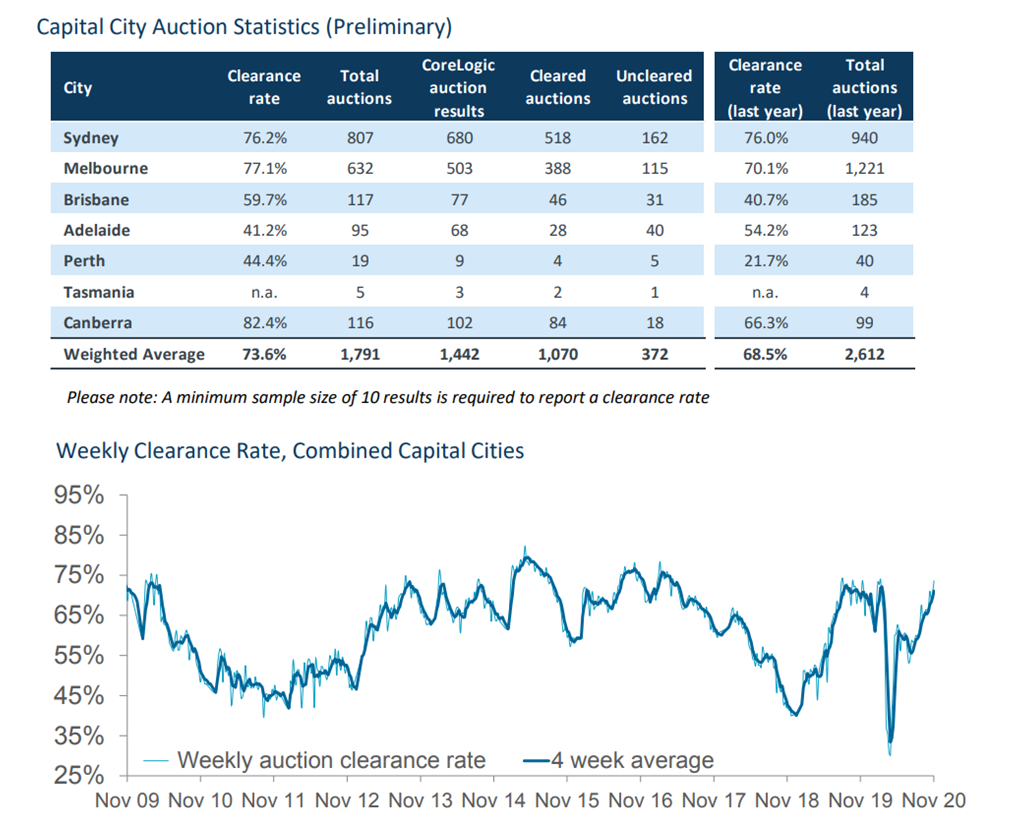

The locked-down Melbourne market, which unsurprisingly fared worst during this episode, appeared to trough in late October and started generating clear price increases at the end of that month. In the November month-to-date, Melbourne has outpaced Sydney in terms of its capital gains. This also reconciles with increasingly robust auction market results, with the preliminary clearance rate in Melbourne for the weekend of November 21 hitting a very strong 77% based on 503 auctions captured by CoreLogic (see table below).

Although there is no evidence of a real boom yet---the recovery thus far has been gradual---Coolabah has since March 2020 forecast strong dwelling price appreciation following a modest six-month correction, with total capital gains of at least 10% to 20% expected over the next few years. Put differently, we do think that a sustainable housing boom will emerge over time. When prices were still drifting lower back in April 2019 we projected that a boom would emerge after the RBA cut rates, which is what we got with house prices increasing by about 10% (care of multiple RBA rate cuts) over the next year prior to the temporary COVID-19-induced interruption. On our figuring, we are still owed at least another 10% to 20% worth of price appreciation. The boom should really grip once property investors flood back into the market in 2021 to capitalise on the advent of "positive gearing" (ie, where gross rental yields are above the cost of servicing mortgage debt).

Since bank credit standards are arguably the toughest they have ever been, we are not concerned about bubbles or financial stability risks at this juncture. One area to watch, however, will be the relatively unregulated non-bank market, which will try to compete with banks through offering borrowers much looser terms and conditions. One potential mitigant will be APRA, which does have the ability regulate non-banks if they present a threat to financial stability.

The Australian housing market is highly seasonal and typically slows-down sharply over December and January. We expect this to manifest in the form of lower clearance rates and slower price growth as we put 2020 behind us.

*Note that CoreLogic does not publish daily index data for non-metro "regional" markets, which is only released on a monthly basis. These regions have, however, outperformed metro markets during the COVID-19 shock.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Enjoy this wire? Hit the like button to let us know.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Investment Disclaimer

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer

This presentation contains some forward-looking information. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Although forward-looking statements contained in this presentation are based upon what Coolabah Capital Investments Pty Ltd believes are reasonable assumptions, there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management