How bad is Australia’s mortgage stress?

The level of household financial stress in Australia is a key issue. This is because a significant pull-back in the financial position of households would have flow-on effects across the economy. So, the recent data released by the nation’s largest lenders provides an important reading of future trends.

With the half yearly earnings reporting season upon us again, the market is provided with an update on household stress levels in the form of bank and insurer results. CBA and NAB have just released numbers, as has the largest mortgage insurer in Australia, Genworth.

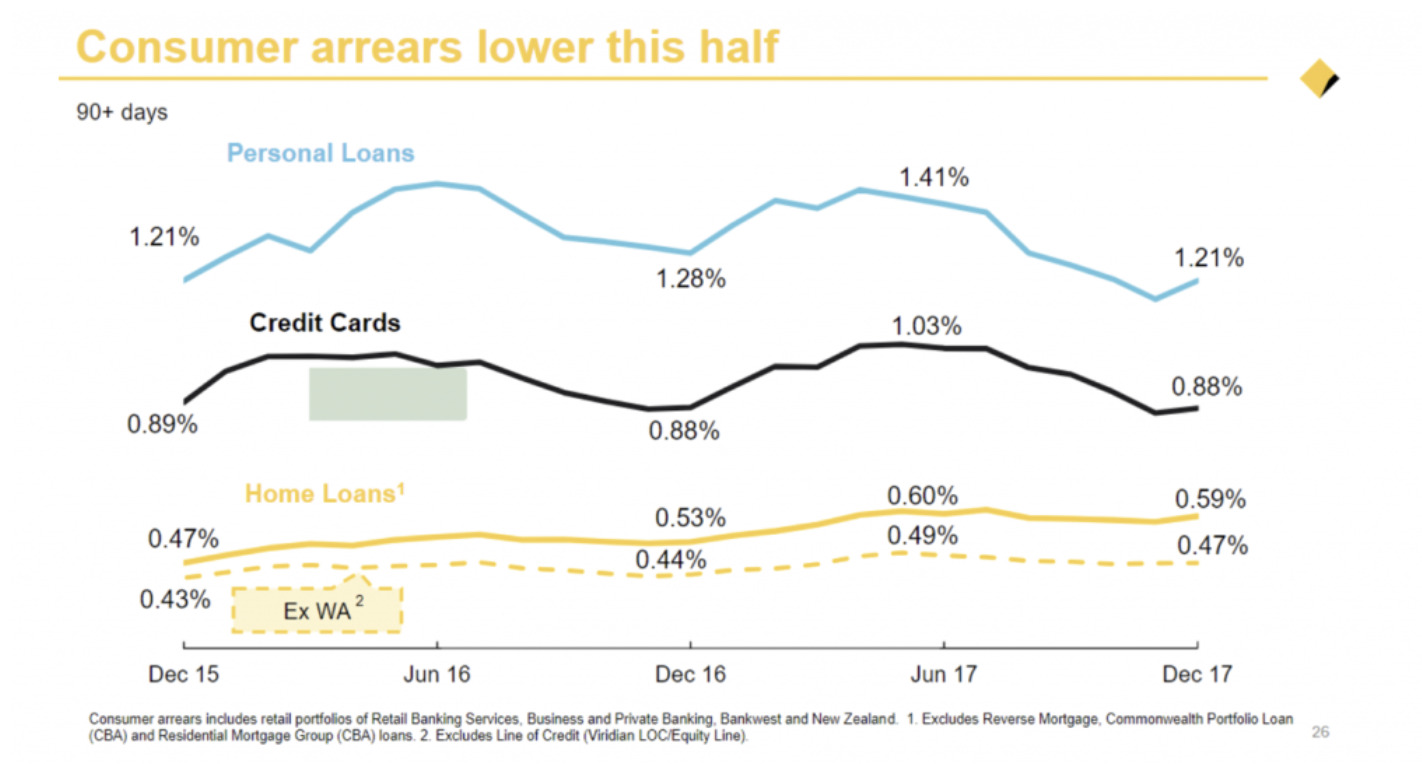

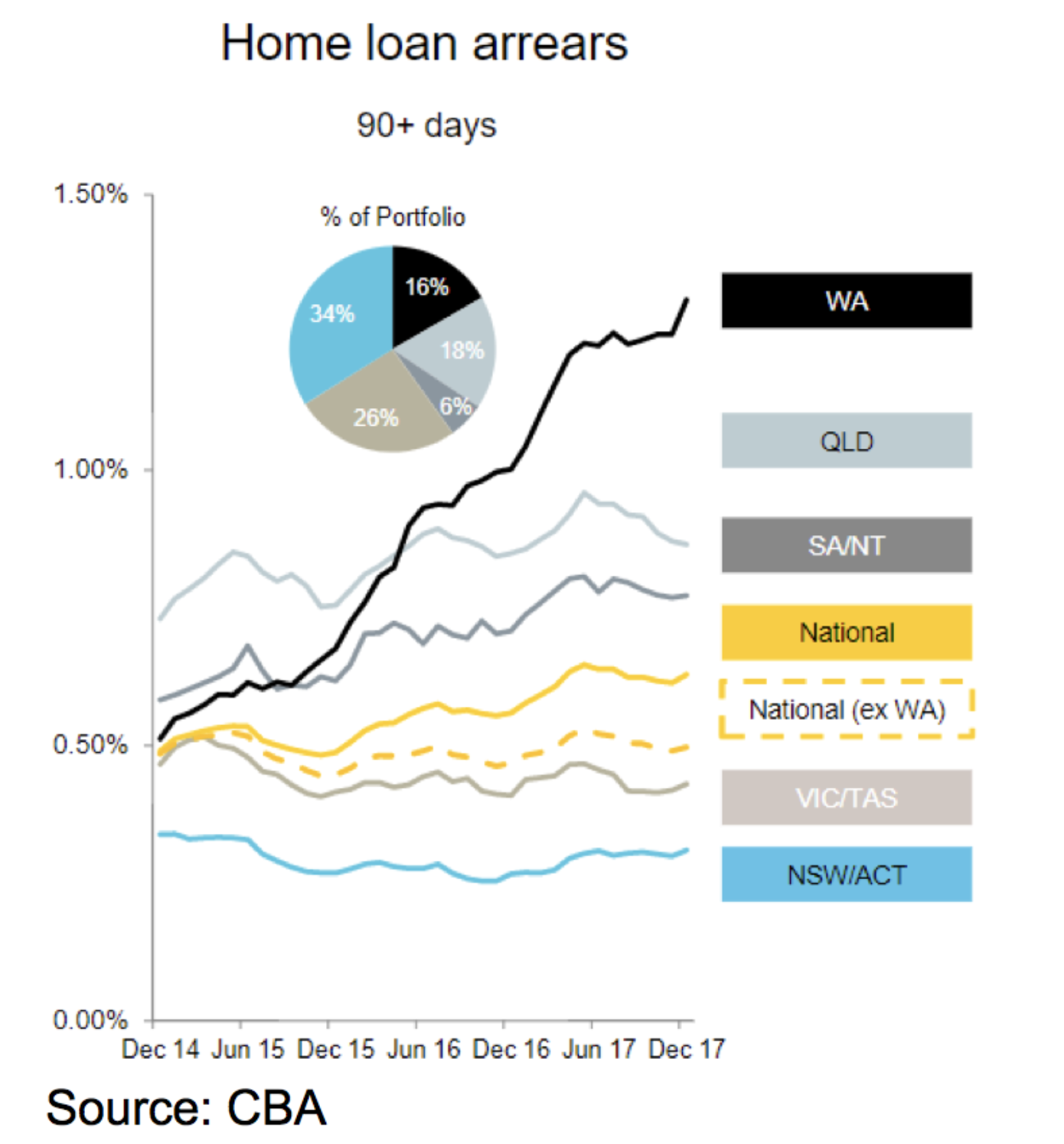

Interestingly, CBA reported declining levels of arrears in its personal and unsecured consumer loan book. In its mortgage book, arrears increased marginally, but only because of the ongoing deterioration in Western Australia.

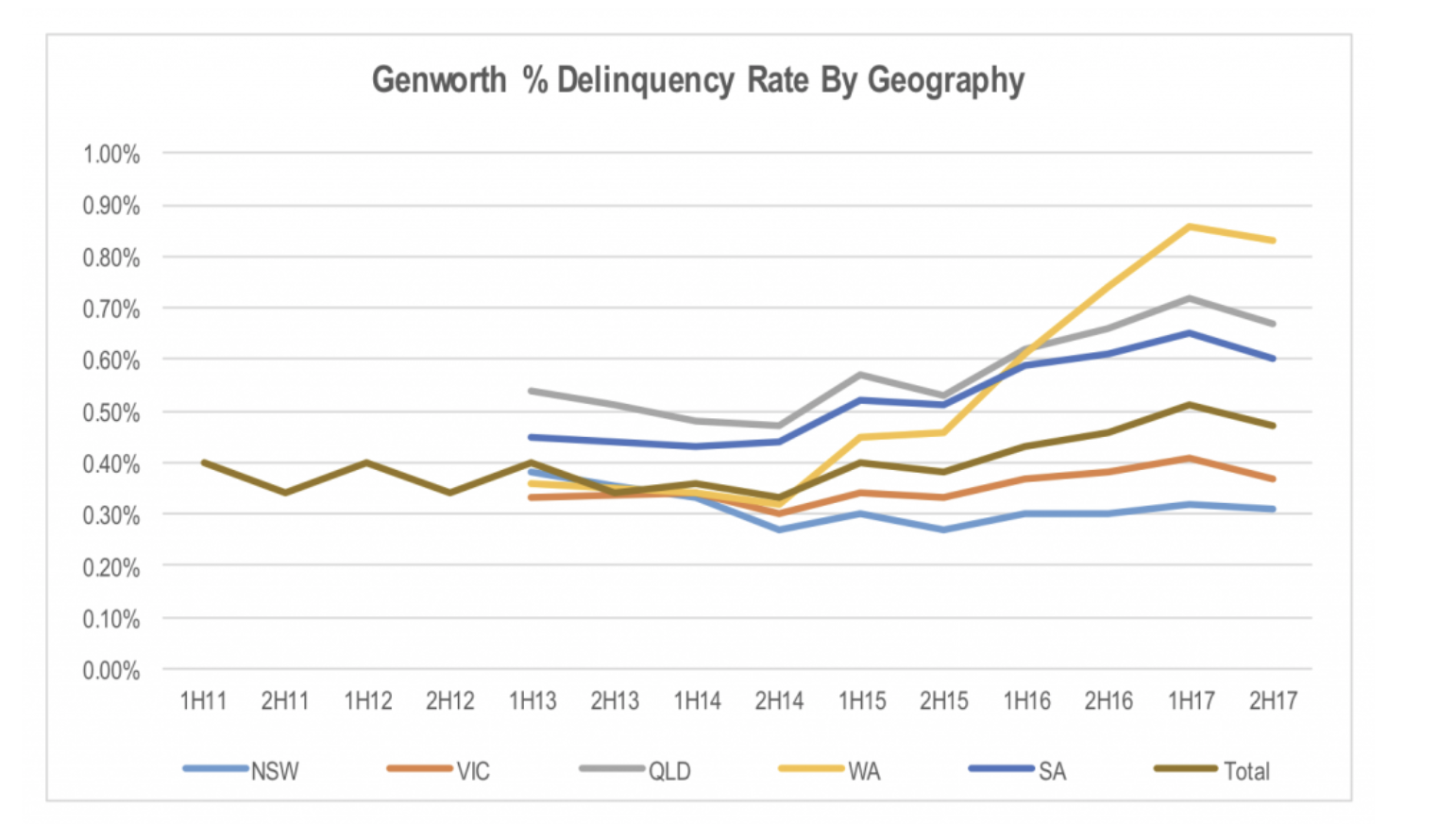

Genworth also reported a slight reduction in its mortgage delinquencies in the six months to December 2017.

This points to a slight improvement in household financial conditions, flying in the face of dire forecasts from a number of economists and strategists in financial markets. So why is this occurring?

One explanation is the strong employment data over the last six months. The increased number of people employed results in increased household income. While wage growth has remained weak, the volume effect of increased employment still provides a positive stimulus for household income.

The other factor is the availability of finance. Macro-prudential controls imposed on the banks has resulted in tighter lending policies being implemented by the majors. This is in the form of both higher interest rates being imposed in perceived problem areas of the market (investment property loans, interest only loans), as well as tightened serviceability and loan to value (LVR) hurdles in the approval process. This was the intended outcome of the policy restrictions. This should have increased household non-discretionary costs, increasing stress to some extent.

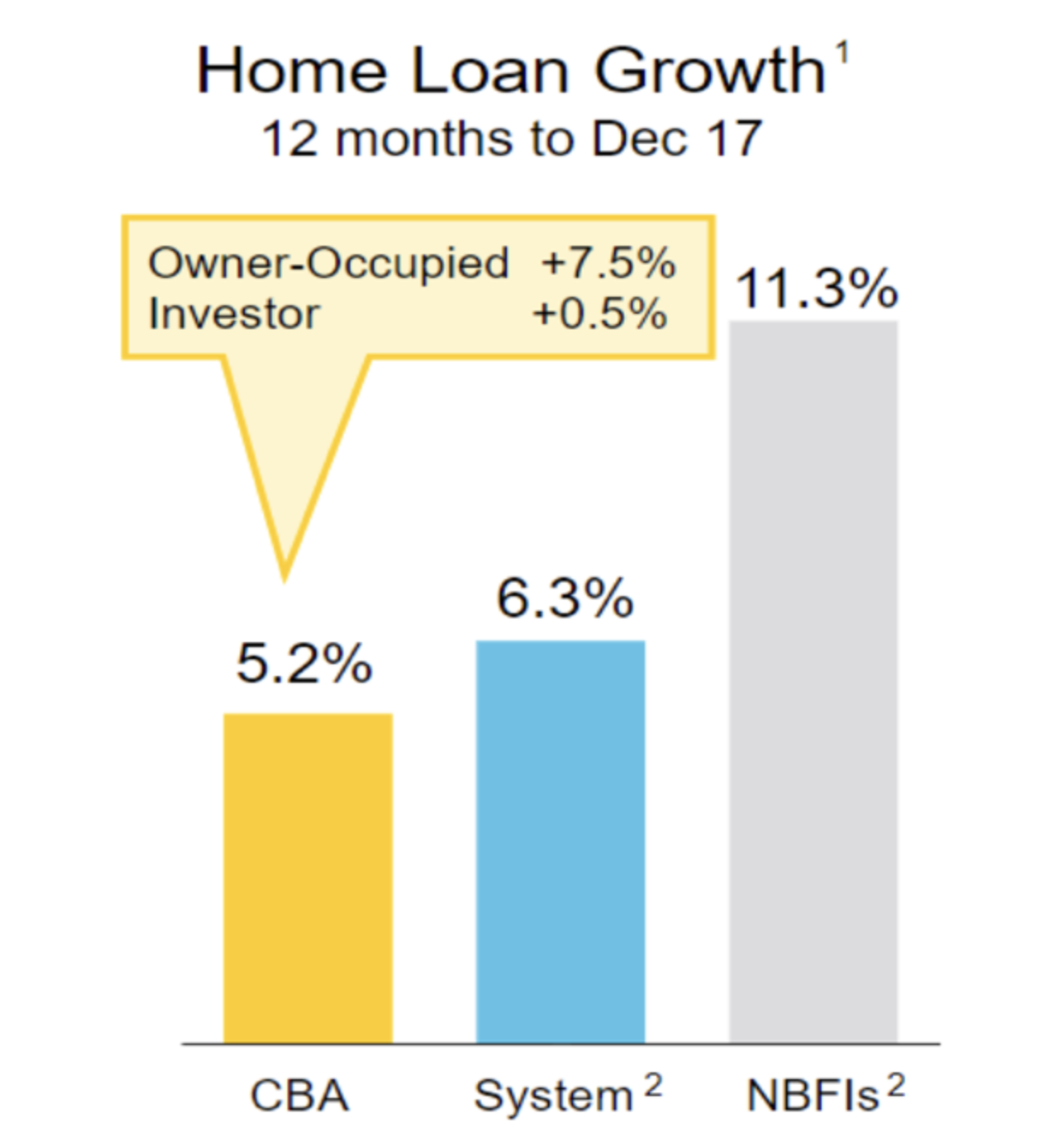

However, as CBA’s result presentation highlighted, while major bank consumer lending growth has slowed materially, non-bank financial institution (NBFI) lending appears to have taken up the slack. The NBFIs offer households a way to avoid the heightened stress that would come from the increase in costs flowing from the macro-prudential restrictions placed on bank interest only and investment property mortgages through refinancing.

Of course, this is not great news for the banks because either the macro-prudential restrictions put them at a competitive disadvantage to the NBFIs, resulting in ongoing reductions in market share, or the risks to the financial system that the macro-prudential regulations are intended to fix are not addressed due to the shift in lending demand to NBFIs.

Going forward, stalled or reversing residential property prices will make it more difficult for households to maintain their spending in the face of rising non-discretionary costs, as they will not be able to increase their debt levels on the back of revalued property asset holdings.

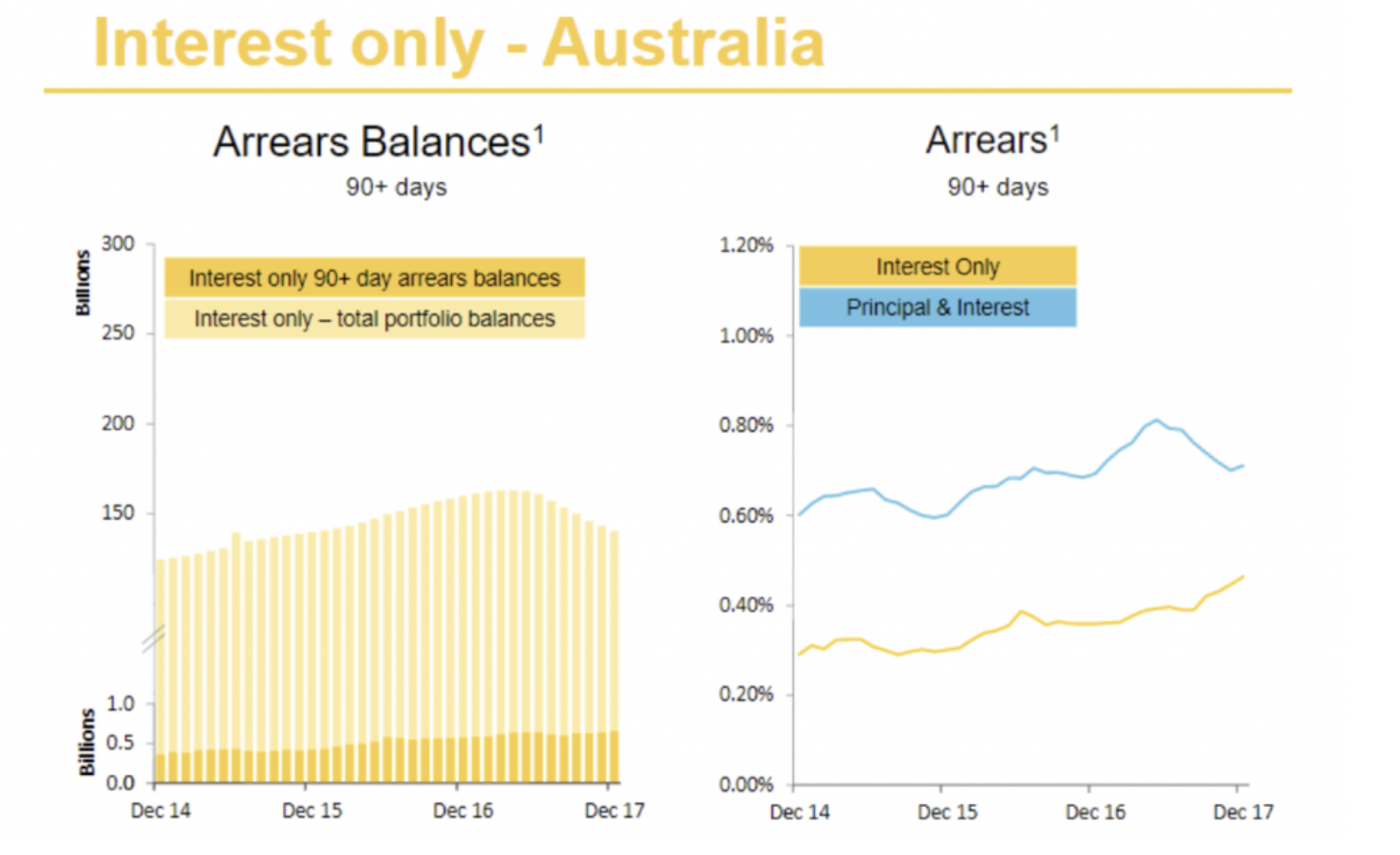

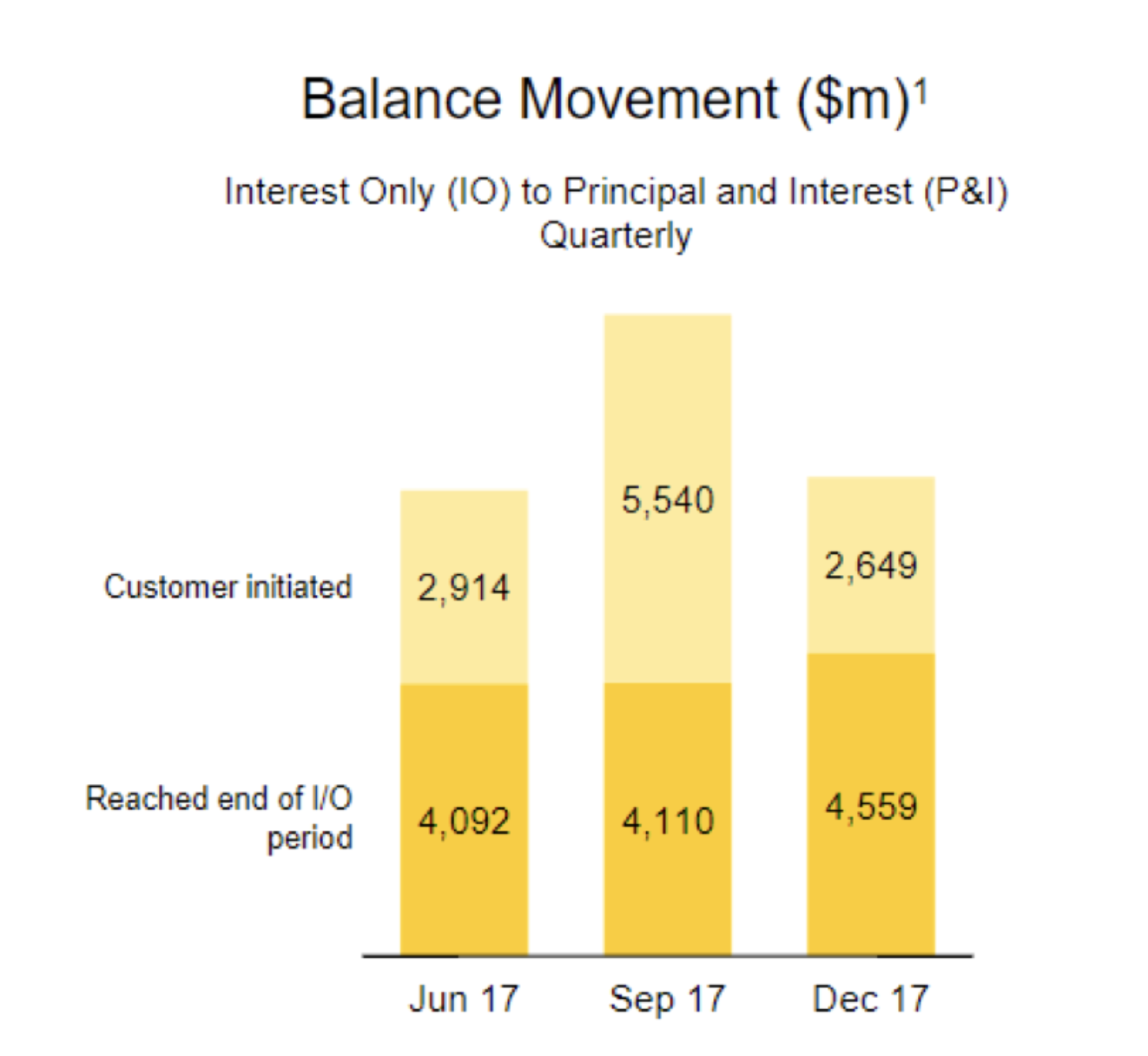

The other point of interest regarding household stress in the CBA result was the slides looking at the bank’s interest only mortgage portfolio. CBA noted that its arrears rate on the interest only book has been increasing steadily over the last three years. However, it commented that this is mainly due to a denominator effect with the size of the loan book having shrunk materially in the second half of the year. This is shown in the following charts.

While the reduction in the size of the overall interest only mortgage book mathematically drove the increase in arrears rate, the book has shrunk as a result of a combination of voluntary switching to principle and interest repayments by borrowers and existing loans rolling off the 5 years interest only period and converting automatically to principle and interest.

In the case of customers voluntarily switching to reduce the interest rate paid, these customers are unlikely at risk of becoming stressed by the increase in repayments (otherwise they wouldn’t switch). Those that reached the end of their interest only period would no longer be counted in the interest only arrears if the 30-40 per cent increase in monthly repayments when moving to principle and interest caused them to fall behind on their repayments. The stress caused by the increased repayments would count them as principle and interest arrears.

Despite this, the volume of interest only mortgages that are in arrears by more than 90 days has been steadily rising over the last 3 years.

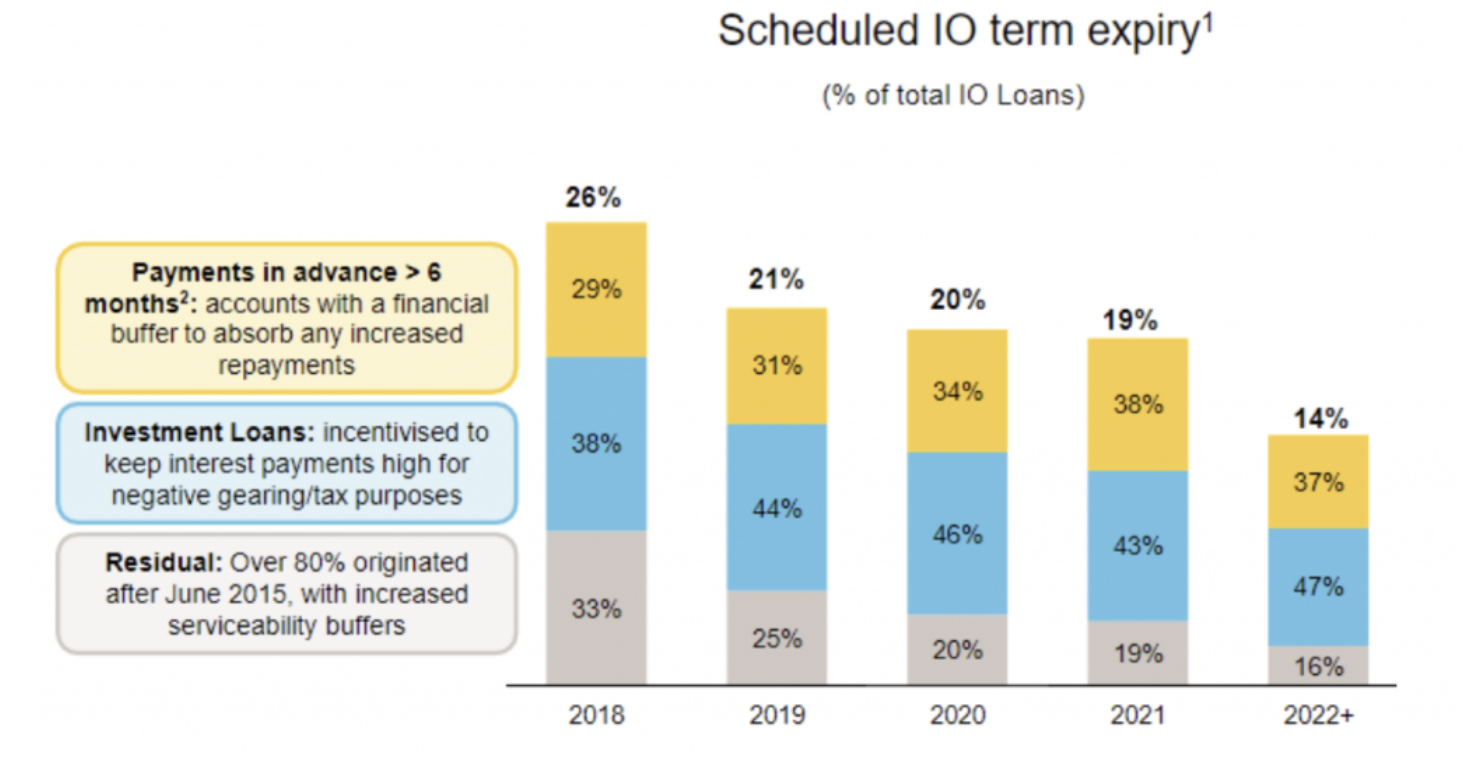

The other point of note was the chart indicating that the rate at which the interest only period expires on the current interest only mortgage book. Using a 5 year lag on the APRA mortgage origination data suggests that the rate of conversion of interest only loans to principle and interest will continue to rise through to the second half of 2019. CBA’s data suggests its rate of conversion peaks this year.

This chart suggests that the peak of the pressure on this portion of CBA’s customer base is likely to occur over the next year or two. The problems for other lenders might take longer to play out, unless employment growth or an acceleration in wages growth comes to the rescue.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

4 topics

Senior Analyst and Portfolio Manager

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Expertise

Senior Analyst and Portfolio Manager

Prior to his departure in August 2022, Stuart was employed by Montgomery Investment Management for over seven years as a Senior Analyst and Portfolio Manager of The Montgomery [Private] Fund.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management