How cheap are the major markets?

While absolute valuation has limited use for timing cyclical bull and bear markets, it does provide insights into market sensitivities to challenging (or indeed positive) economic environments. Added to that, relative valuation can be particularly insightful – especially as a key building block for allocating between asset classes and geographies.

There has been significant movement in a wide variety of asset prices over the last quarter (e.g. since April: Shanghai Comp -12.05%, MSCI EM index -4.76%, and FTSE100 +6.96%). That has impacted a number of valuations of key assets and raised a number of valuation questions. We deal with a variety of these in the following paragraphs, starting with China.

Is China Cheap?

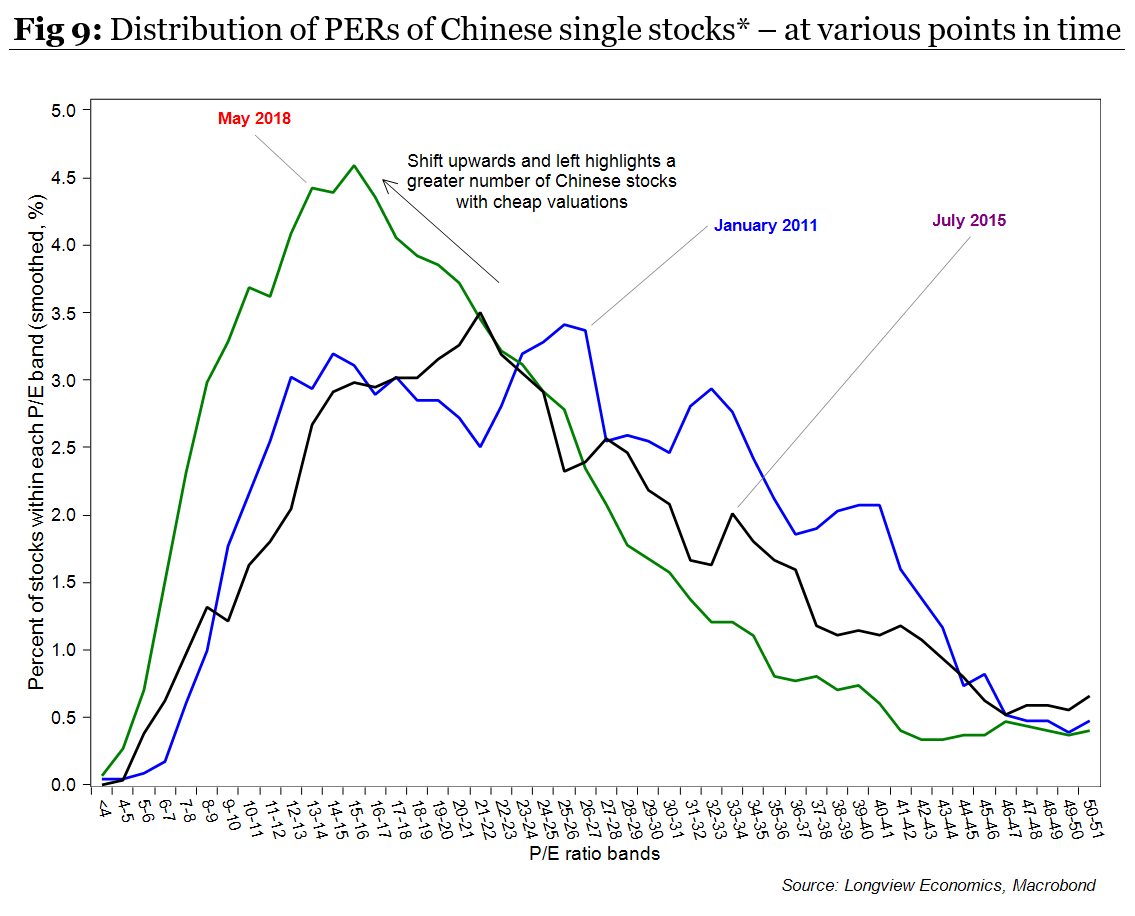

On the surface, and on a number of measures, Chinese equities appear attractively priced. A comparison of the forward PE ratios illustrates the point: The Shanghai Composite is on a forward PER of 11.4x, the S&P500 is on 16.7x. Similarly, China’s median PE ratio is at historically low levels relative to the US median. Over and above those factors, the analysis of the internals of the Chinese market further highlights the recent increasing attractiveness of Chinese equities. The distribution curve of individual stock PERs that make up the Chinese market has shifted to the left and thus, relative to its own history, a broad number of stocks have become cheaper.

In comparison with other regions of the world, though, China’s attractiveness is less clear. The distribution curves of individual stock PERs for different parts of the globe shows that the makeup of the Chinese market is distinctly different: China’s distribution is flatter, with a significant percentage of stocks with greater than ‘normal’ PE ratios.

Is the UK cheap?

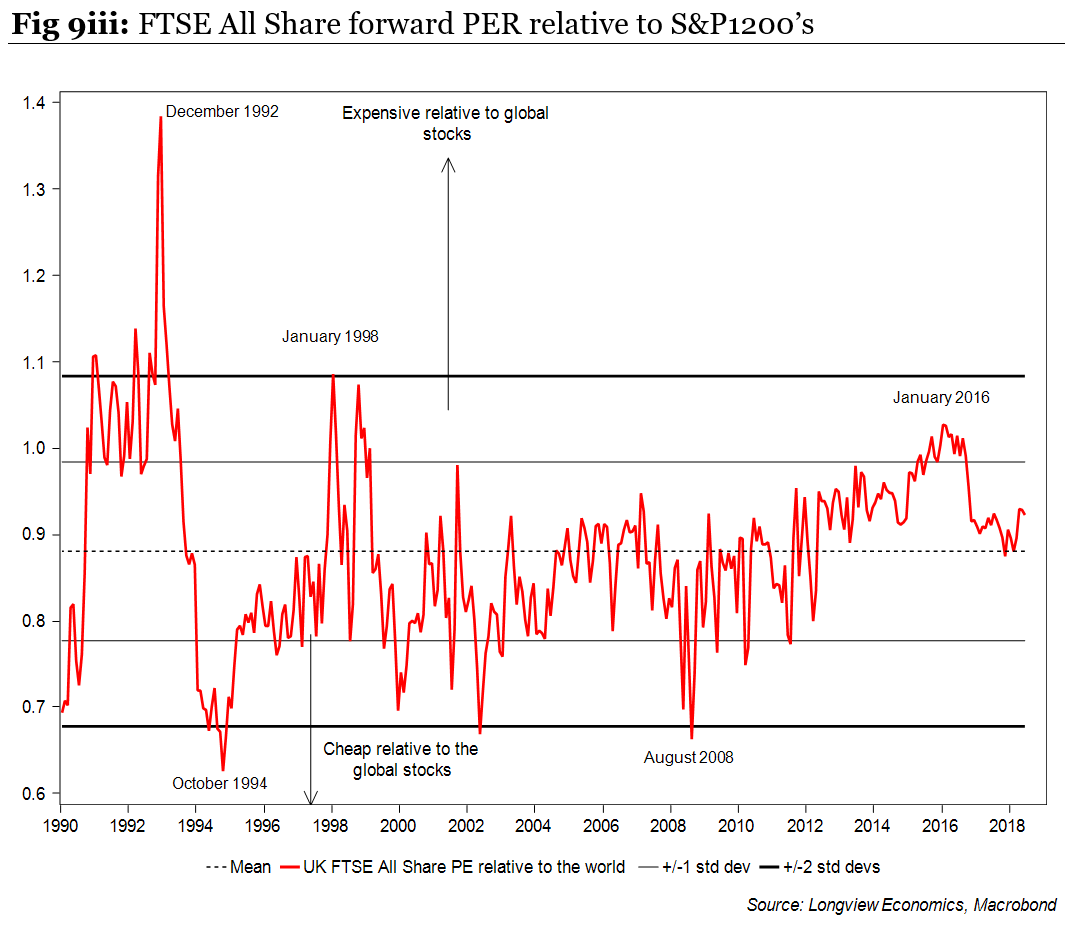

The UK is often cited as a cheap market. On a variety of metrics, though, it’s difficult to make a strong argument that this is currently the case.

Examples of evidence for this include:

- The FTSE All Share’s PER is at its long term mean;

- The distribution of single stock PERs has shifted rightwards, i.e. the percentage of ‘expensive’ stocks (with a PER of over 30x) has increased and the right hand tail has become ‘fatter’;

- Consistent with that, the UK’s median PER has become richer relative to the US median; &

- The UK’s PER relative to global stocks is still above its long term mean.

Against other UK assets, though, UK equities do look more attractive. On an equity risk premium (ERP) basis against real government bond yields, real cash rates, and corporate bond yields, UK equities offers value. The risk premium is the most significant in comparison to corporate bond yields, trading at over 1 standard deviation above its historical mean.

Is the US cheap?

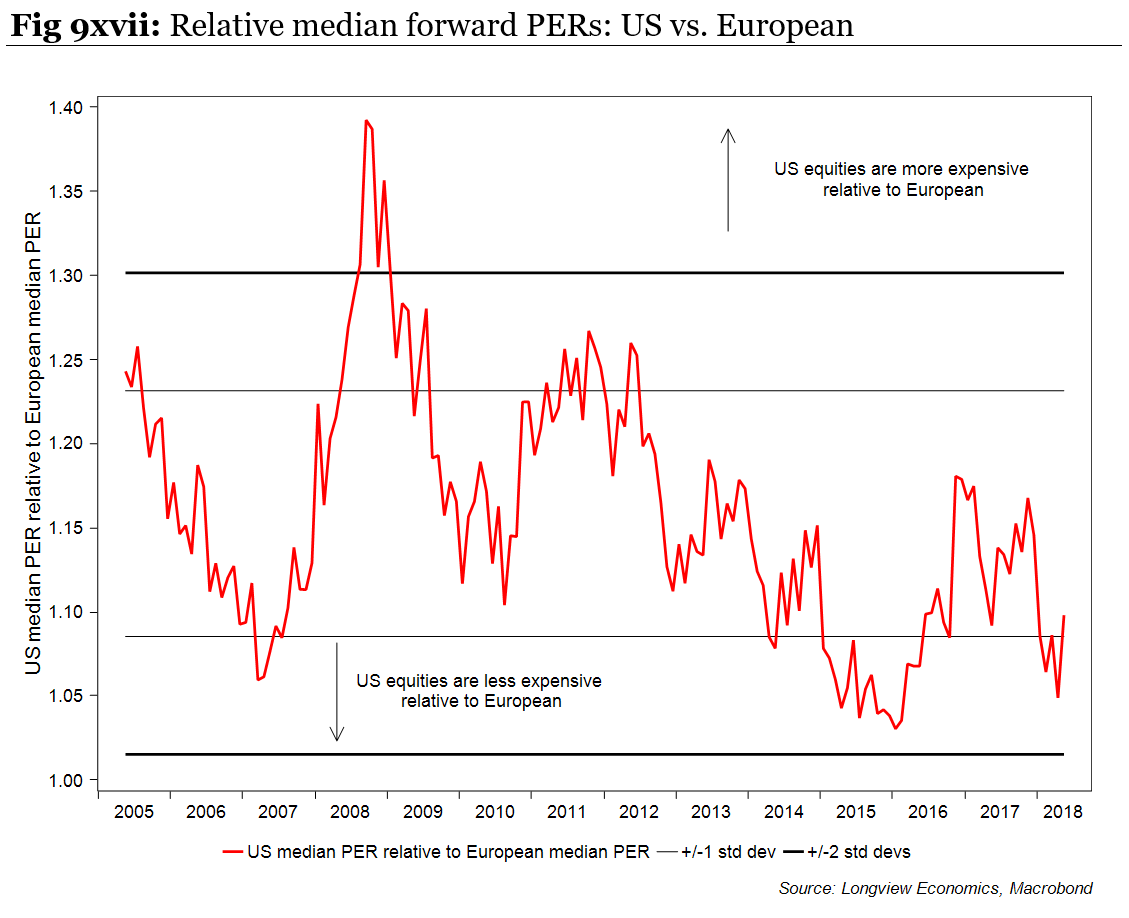

Despite the widely held view that US equities are expensive, they are cheaper than they seem. A comparison of the relative median PER of the US and Europe shows the US to be cheap relative to history.

Using the overall PER of the S&P500 relative to the STOXX600, the relative valuation is currently at its long term mean. In addition, analysis of the internals of the US & European equity markets continues to show that the distribution of single stock PERs remains a broadly similar shape, with a fatter tail accounting for the greater overall PER of the S&P500. Compared to the distribution in January, the US PER distribution’s left tail has become ‘fatter’ while the right hand tail has become ‘thinner’. In other words, a greater number of stocks now have valuations below the average, while fewer are more expensive than average (i.e. stocks present better value). In Europe, in contrast, the curve is little changed from earlier this year.

Using the overall PER of the S&P500 relative to the STOXX600, the relative valuation is currently at its long term mean. In addition, analysis of the internals of the US & European equity markets continues to show that the distribution of single stock PERs remains a broadly similar shape, with a fatter tail accounting for the greater overall PER of the S&P500. Compared to the distribution in January, the US PER distribution’s left tail has become ‘fatter’ while the right hand tail has become ‘thinner’. In other words, a greater number of stocks now have valuations below the average, while fewer are more expensive than average (i.e. stocks present better value). In Europe, in contrast, the curve is little changed from earlier this year.

Valuations elsewhere

Looking across a range of global asset classes, geographies, and valuation metrics, and with regard to what is expensive in other assets, high yield corporate bonds remain a standout, both in the US and in the Eurozone. High yield spreads remain historically tight, albeit have widened modestly recently. In the investment grade sphere, valuations are markedly different with spreads now wider than their historic median.

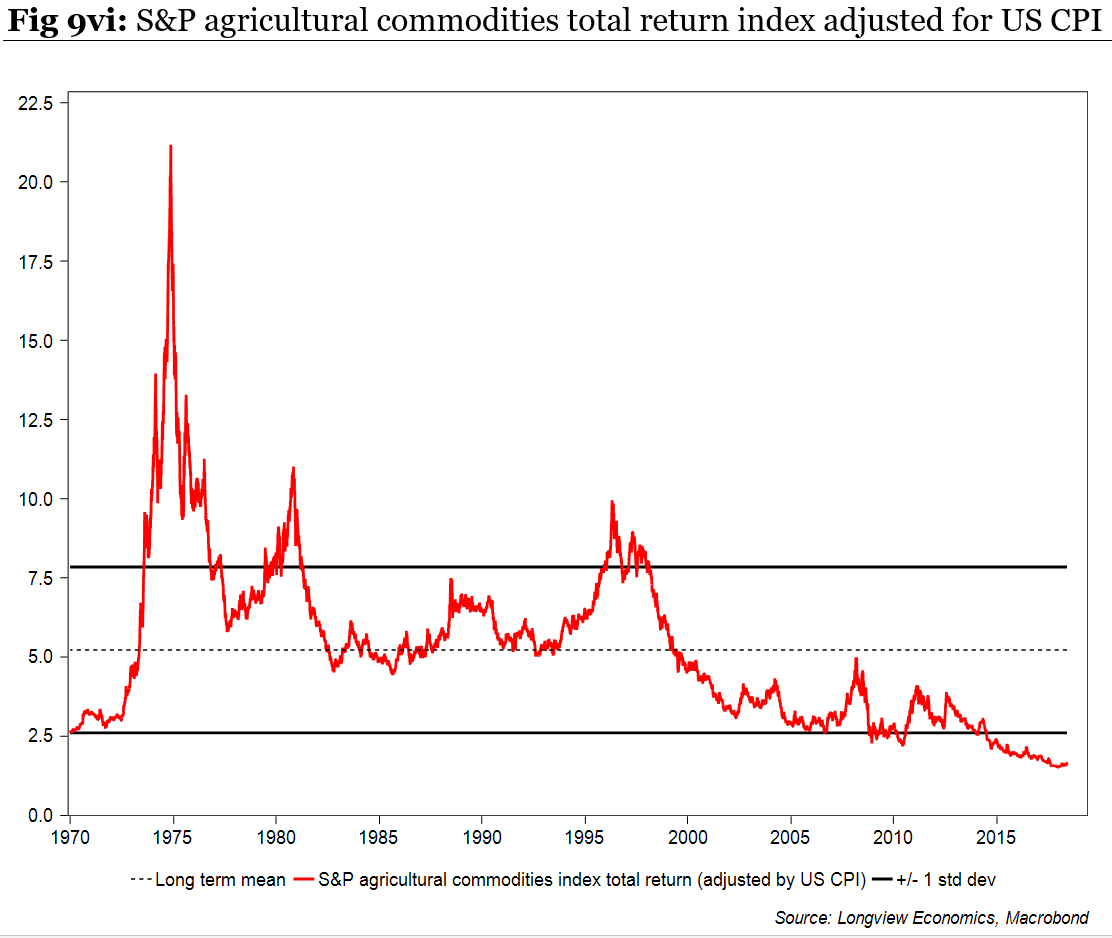

In terms of what is notably cheap, agricultural commodities continue to look attractive. On an inflation adjusted basis, the S&P agricultural commodities total return index is close to its cheapest on record.

Our Quarterly Asset Allocation Valuation Update, including dozen of charts, is available here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation advice; and Global thematic, macro and commodities research.

2 topics

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Longview Economics, founded in 2003 by Chris Watling, is an independent research house based in London, providing three distinct yet interrelated groups of research products: Short and medium term market timing; Long term global asset allocation...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

Ross vs the AI hype: her shocking prediction revisited

Livewire Markets