How diversification, infrastructure can offset 'black swan' risks

The turmoil we have seen in markets over the past few weeks has served as a timely reminder of the importance of diversification in portfolios, both across asset classes and within them.

Infrastructure as a sub-sector within equities has outperformed the broader market given that demand for utilities is more inelastic than other sectors.

For example, households need to keep the lights on, and communication networks need to function regardless of how well the economy is performing. Utilities such as water and electricity supply grids represent over 50 per cent of the infrastructure index. Performance across other parts of the infrastructure sector such as transport will be more variable depending on demand.

Listed infrastructure has been a popular asset class for investors over the past decade, largely due to the consistent, stable cash flows that infrastructure assets produce relative to other sectors. However, investing in the listed infrastructure sector comes with its own sector specific risks.

Depending on how infrastructure is defined, companies can have varying exposure to economic cycles and energy prices. Infrastructure companies also typically have high levels of debt, and with large physical assets, can be subject to stock-specific tail risk, or "black swan" event risk. Holding a well-diversified portfolio, and investing only in strictly defined "core" infrastructure companies can mitigate some of these risks.

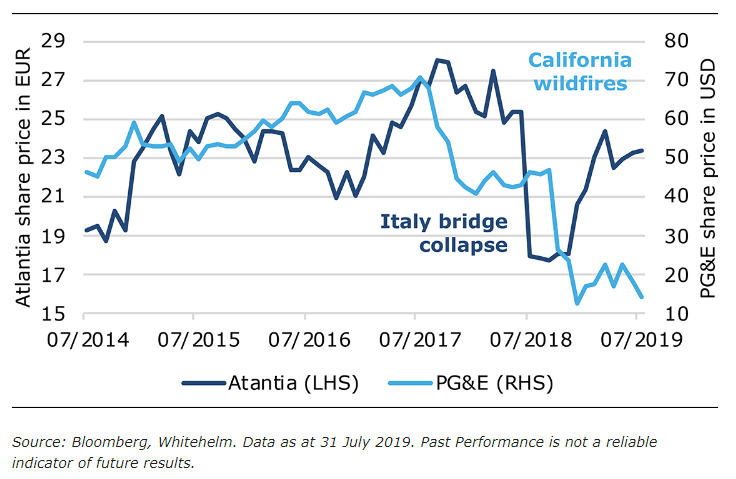

One recent example of black swan risks includes the wildfires in California in late 2018 that eventually forced the regional electric utility company PG&E into Chapter 11 bankruptcy protection.

Another example is the bridge collapse in Genoa, Italy, in 2018. This catastrophe caused a major correction in the shares of Italian infrastructure company Atlantia Spa. The individual stock price moves are displayed in the exhibit below.

Black swans hit Atlantia and PG&E

These event risks show that simply restricting your investments to core infrastructure does not protect the portfolio to a severe event or “tail” risk, often stemming from natural catastrophes like wildfires, earthquakes or windstorms. And no matter how much you analyse a business, if an earthquake hits, the share price will suffer dramatic declines without any warning.

The global COVID-19 pandemic is the latest example of an event risk. Although the pandemic is affecting most company’s share prices due to the economic impact; airports, railroads and other transport assets have been among those hit the hardest as many countries have gone into lockdown.

The impact on share prices in this sector has been severe as the length of the shutdown and effect on earnings is hard to gauge until the crisis resolves. Ultimately those with strong balance sheets, good management and low debt are likely to emerge stronger than their competitors in the aftermath.

Because such “black swans” are unpredictable, one way to mitigate this is to give an equal weight to each stock in a core infrastructure portfolio. This results in a much more diversified portfolio, particularly when compared with the market’s capitalisation weighting. After all, why should a specific catastrophe like a wildfire or a pandemic be more likely to hit a large company than a small company?

An equal-weighted approach to investing means that even if a black swan occurs, there will be no outsize impact on the portfolio from exposure to one stock. In a 40-stock infrastructure portfolio with equal weights, the weight of each stock is about 2.3 per cent to 2.5 per cent.

This means that in August 2018 when the bridge in Genoa collapsed, Atlantia had a weight of 2.4 per cent in the equal-weighted portfolio compared with 4.7% in the S&P Global Infrastructure Index. The subsequent 30 per cent decline in the share price of Atlantia would have detracted only 0.7 per cent from the equal-weighted portfolio and led to fewer losses than the S&P Global Infrastructure Index.

Similarly, the falls in share markets that we have seen in recent weeks highlight the importance of spreading risks across different industries. An equal-weighted approach can help prevent excessive losses in a portfolio of core infrastructure stocks and act as an additional risk management tool in the face of unpredictable risks.

Minimising tail risk

The benefits of an equal-weighted allocation to stocks tend to come to the fore when investors need them the most. In an equal-weighted portfolio large companies do not have an outsized weight and consequently do not drag down the portfolio in case of an unexpected crisis or natural catastrophe.

The diversification benefits of equally weighted stocks minimise the risks of any tail risk event which occurs to any one infrastructure company. This simple balanced approach to allocating capital has served investors well in the past for a portfolio of private infrastructure assets.

Ursula Tonkin head of listed strategies at Whitehelm Capital

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ursula has extensive portfolio management and analytical experience in Australian and global infrastructure equities, with over 18 years industry experience. Prior to joining Patrizia, Ursula was a portfolio manager and senior analyst responsible for covering energy infrastructure, natural gas and renewable energy for an SRI/ethical investment manager.

Featuring

Ursula Tonkin,

PATRIZIA

Ursula has extensive portfolio management and analytical experience in Australian and global infrastructure equities, with over 18 years industry experience. Prior to joining Patrizia, Ursula was a portfolio manager and senior analyst responsible for covering energy infrastructure, natural gas and renewable energy for an SRI/ethical investment manager.

2 topics

Ursula has extensive portfolio management and analytical experience in Australian and global infrastructure equities, with over 18 years industry experience. Prior to joining Patrizia, Ursula was a portfolio manager and senior analyst responsible...

Comments

Comments

Sign In or Join Free to comment