How should investors allocate to government bonds today?

The increase in borrowing by governments around the world because of COVID-19 will push budget deficits to well above peak levels during the financial crisis and into the realms last seen during World War 2, according to the International Monetary Fund.

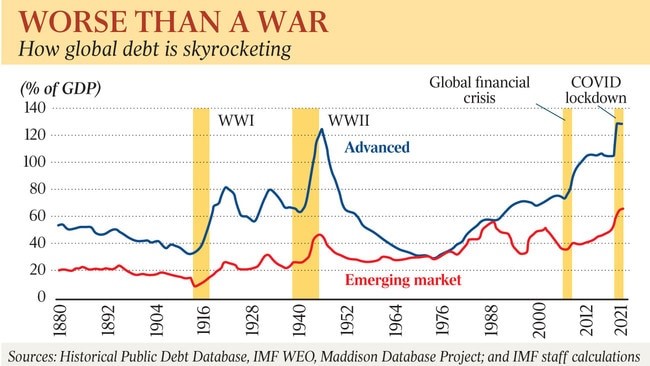

In fact, the chart on the left shows that advanced economies are reaching all-time record debt/GDP levels courtesy of massive economic stimulus packages. And while the velocity of debt is soaring, economic growth is going the other way. According to World Bank forecasts, the global economy will shrink by 5.2% this year.

That would represent the deepest recession since World War 2. As such, bond yields are expected to remain low for an extended period so that governments can continue to service their debts. It's astounding to think that ~30% of all bonds traded globally have negative yields, while even 100 basis points is now becoming too much to ask in Australia and comparable economies (see chart on the right).

Yet Australian government debt is flying out the door, with Bloomberg reporting a record $66 billion of bids last week for 1% paper maturing in November 2031 (the final sale amount was $21 billion). That followed July's $15 billion sale of 31-year bonds at 1.94%. The trend is similar overseas, with the U.S. Treasury Department reportedly preparing a record US$112 billion bond sale whilst tilting issuance toward longer-dated securities.

On the one hand, investors buying these instruments seem willing to accept less than the usual rate of inflation for extended periods. On the other hand, government bonds possess other characteristics such as stability, liquidity, and certainty of income, which are highly valued in times of uncertainty. However, with debt levels and yields where they are, how should investors approach investing in this asset class within portfolios today?

To shed light on some of these issues and to discuss the role of government bonds in a portfolio we've asked two of our contributors with strong views on the asset class to produce bull versus bear reports, exclusively for Livewire readers.

- The bull case is written by Darren Langer of Nikko AM in his wire titled "The case for owning government bonds".

"A known return in an uncertain world, where returns on all asset classes are likely to be lower than the past, might just be a good thing to have in a portfolio. This is particularly true given the large cohort of baby boomers heading to retirement who may not have five or 10 years to recover from another major shock to risk assets."

The bear case is written by Alex Pikoulas from Lipman Burgon & Partners, who advocates avoiding government bonds in his piece "The world’s biggest hussle".

"Current anaemically low nominal interest rates of sub 1%, and negative real interest rates, mean that long term government bond holdings are certain to destroy real value. There is no place for this sort of asset in any portfolio whose objective is to protect and grow long term wealth."

FOLLOW the managers to get their reports first

If you want to be the first to read their reports, click on each of the managers you want to hear from, and then click FOLLOW on their profiles. This way you will receive the report directly by email soon after it goes live. I hope you find them useful.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Featuring

Darren Langer,

Yarra Capital Management

Darren is highly regarded in the fixed income industry and is regularly featured in the press. He is also co-host of the popular Australian podcast series The Rate Debate. He has more than 30 years’ experience in fixed income markets and 25 years managing multi-sector fixed income portfolios. Prior to his role at Yarra Capital Management, he was Head of Fixed Income at Nikko AM (Nikko AM was acquired by Yarra Capital Management in April 2021), and a Senior Portfolio Manager at Perpetual, where he held the position for 12 years. Darren has co-responsibility for the Australian Fixed Income team at Yarra Capital Management and is co-portfolio manager of the highly-rated Nikko AM Australian Bond Fund and the Nikko AM insurance mandates.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

2 topics

1 contributor mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment