How to get more from your defensive asset allocation

What exactly is a defensive asset? The answer to this depends very much on who you ask. For some people the priority is liquidity so just holding cash might make sense. For others, it means they have very limited performance volatility so perhaps you could consider a term deposit. And for others, it might mean protecting your portfolio if equities are selling off, which might mean you want a lot of interest rate risk so perhaps buying some longer-dated government bonds might make sense. It would be nice if there was one solution that accomplished all of these goals simultaneously, but that may be hard to find.

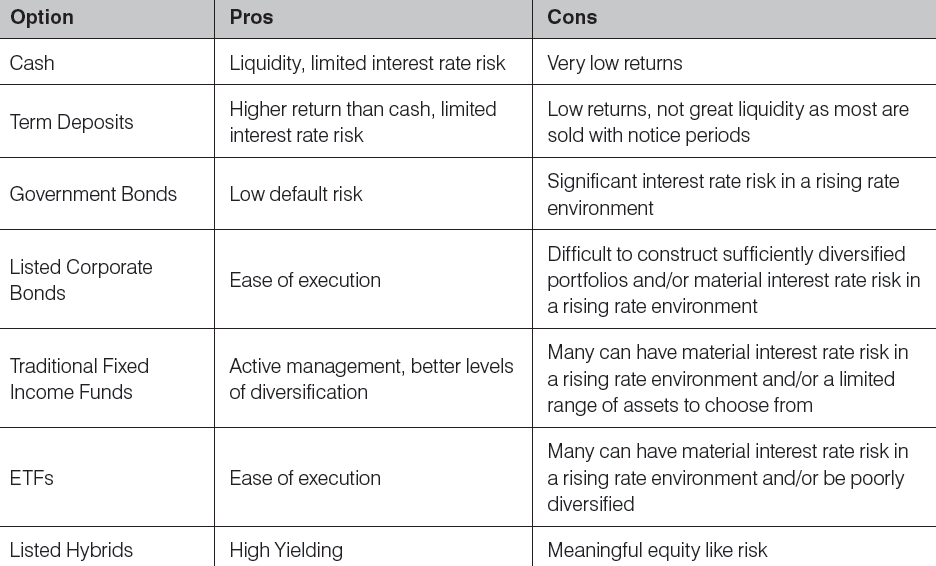

The table below summarizes a few of the more traditional defensive asset allocation (DAA) choices and some of the pros and cons of each:

Another option which may be worth considering in your DAA strategy might be a low duration absolute return bond fund.

These funds try to balance a range of investor objectives. There are a number of these types of products available in Australia. In our opinion, the best ones offer all the following attributes.

12 ideal attributes of a low duration absolute return bond fund

Absolute Return Focus: An absolute return focus means the manager is trying to generate positive returns in most market environments. Contrast this with an approach where a benchmark is provided and the fund outperforms that benchmark but still loses money for investors. That should not be considered a good outcome.

Unconstrained: Many traditional income fixed funds are managed against a stated benchmark. Two of the more common benchmarks are the Bloomberg Ausbond Composite Index and the Barclays Global Aggregate Index. Managers should be held accountable for their performance, so benchmarking them against an index makes intuitive sense. However, all fixed income benchmarks have limitations. The fixed income markets are large and diverse. There is no one index that does a good job of reflecting the range of investment opportunities. In addition, it’s very easy for managers to outperform their index by taking greater credit risk than represented in the underlying index. Unfortunately, that practice is all too common.

Limited Interest Rate Risk: Interest rates remain very close to multiple-century lows. It seems unlikely they will stay there forever. It might be prudent to avoid taking excessive interest rate risk at this point in the cycle. A bond or portfolio of bonds that has interest rate duration greater than two years might be worth reconsidering in the current environment. Many absolute return strategies are often run with a duration of less than a year. However, there are times when a long interest rate duration is appropriate so it’s also worthwhile for the manager to have the flexibility to extend duration when needed. On a related point, long duration bonds are often touted as a good hedge for equity risk, but correlations there are far from reliable and often break down for long periods.

Very high average credit quality: Most funds will disclose an average rating which is usually the weighted average rating of all the securities held in their portfolio. The S&P rating scale is shown in the table below and some examples of entities with each rating.

In our opinion, funds worthy of consideration for your core DAA should have a weighted average rating of at least “A” or better. Anything below that would likely introduce more volatility than would be considered appropriate for a defensive asset class. Another note of caution, be wary of funds that do not disclose their weighted average rating. It could mean they are taking more credit risk than they should boost their returns.

Limited equity-like risk: Absolute return funds do have a modestly positive correlation to equities, but may be able to reduce that correlation during bear markets through various risk mitigation strategies. Listed hybrids, on the other hand, can have meaningfully high correlations with the underlying equity. During the massive correction seen during the global financial crisis in 2008, listed hybrids were highly correlated with listed equities providing little if any downside protection.

Active management: Passive management might make sense in some parts of your portfolio, but it’s our view that it’s not a particularly good option in fixed income. Most passive fixed income strategies either follow an index with meaningful duration risk (which we believe doesn’t make a lot of sense in this environment) or are poorly diversified. Only through active management can managers look for the most attractive assets and make good decision about risks that should be allowed in a portfolio and those that should be hedged away.

Diversification: Most active bond funds have a reasonable level of diversification but not all of them. Any strategy which has less than fifty different issuers in the portfolio is potentially taking too much single issuer risk. While most issuers rated investment grade should be considered safe and have a low chance of defaulting, unforeseen things do occur from time to time. If a portfolio has too much exposure to a name that defaults, it could destroy the performance of the fund for years. Bonds have an asymmetrical risk payoff structure meaning there is very little upside (especially in investment grade bonds) but lots of downside risks. This means diversification in a bond portfolio makes a lot of sense. Running concentrated bond portfolios usually does not.

Liquidity: Liquidity of most bonds funds is generally pretty good. They often offer daily redemptions and you can usually get your money back in 2-3 days. This tends to be much better than term deposits. Nowadays investors usually have to give at least thirty days notice to get their money back and have to invest for long periods of time to get anything resembling a decent return.

Global mandate: The Australian bond market makes up a very small percentage of the global bond market (less than 2%). Australian bond yields are reasonably attractive by global standard, but that may not always be the case. It seems sensible to have the ability to look offshore for attractive assets if valuations are compelling.

High levels of regular income: A good defensive asset should still provide a regular income stream.

Multiple sources of return: Bond funds will generally get most of their returns from their coupon income whether it be government or corporate bonds. However, returns in the short term will be heavily influenced by movements in the levels of interest rates and credit spreads. Absolute return funds usually have the flexibility to generate returns from multiple different sources including coupons, currency and relative value trades.

Low volatility: No matter where the returns come from, the primary focus for any absolute return fund should be on capital preservation and minimizing volatility while still consistently hitting the stated return target.

Absolute return bond funds are not a panacea. They still have a range of risks and require a skilled experienced manager to make use of a large range of investment options while effectively managing the risks. But even if you assume this to be the case, there will still be risk. The question obviously becomes do the benefits outweigh the risks. Asset allocation is never an easy process and there aren’t many free lunches in investing, but given the relative benefits and additional return potential, a low duration absolute return bond fund may warrant consideration for your core defensive asset allocation strategy.

Disclaimer: Please note that these are the views of the writer and not necessarily the views of Daintree. This promotional statement does not take into account your investment objectives, particular needs or financial situation.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Mark Mitchell established Daintree Capital in January 2017 and has over twenty years industry experience both in Australia and the USA, specialising in fixed income securities analysis and portfolio management.

Prior to establishing Daintree Capital, Mark was the Head of Credit and Portfolio Manager for over seven years at Kapstream Capital. There, he was ultimately responsible for the development and implementation of the credit research processes and portfolio management until the time he left in October 2015. Over this time, Kapstream grew to over $10bn in assets under management.

Prior to his time at Kapstream, Mark was a Portfolio Manager/Senior Credit Analyst specialising in global credit securities at Colonial First State Global Asset Management between March 2001 and September 2008.

Before moving to Australia, Mark achieved nearly a decade’s work experience in the USA across a range sectors including high yield, bank loans, commodities, futures and listed equities.

Mark holds a Bachelor of Science (Finance) from the DePaul University (Chicago) and is a CFA Charterholder as well as a Chartered Market Technician (CMT).

.jpg)

1 topic

.jpg)

Mark Mitchell established Daintree Capital in January 2017 and has over twenty years industry experience both in Australia and the USA, specialising in fixed income securities analysis and portfolio management. Prior to establishing Daintree...

Expertise

Mark Mitchell established Daintree Capital in January 2017 and has over twenty years industry experience both in Australia and the USA, specialising in fixed income securities analysis and portfolio management. Prior to establishing Daintree...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The shift toward scarcity: a playbook for a new era of investing

Talaria Asset Management