How will Australia weather the virus and the fires?

Dr Philip Lowe, Governor of the Reserve Bank of Australia (RBA), believes the economy has been experiencing a gentle turn up through the last quarter of 2019 and early 2020. Data on housing and consumer spending broadly support this claim, with the de-escalation in geo-political tensions and stabilisation in global activity data underpinning an improving global backdrop. Indeed, the RBA left its forecasts for end-2020 growth unchanged at 2.7% in early February against expectations it would downgrade its near-term outlook.

But that outlook for improving growth is now challenged by Australia’s recent bushfires, the ongoing drought, and the impact of China’s sharp slowing in early 2020 on the back of the coronavirus outbreak. Can we still expect better growth through 2020? Could fiscal policy add to the stimulus from last year’s interest rate cuts? And how will the domestic equity market weather the combination of high valuations, a relatively soft earnings outlook and increasingly risk-off global markets?

The second half of 2019 started with a more positive flavour

Australia’s growth and inflation performance through H1 2019 evolved in a similar fashion to much of the rest of the world. Growth slowed mid-year to a post GFC low of 1.4%, less than half it’s 3.1% pace a year earlier, while inflation fell to 1.6% (below the RBA’s 2-3% target) from 2.1% a year earlier.

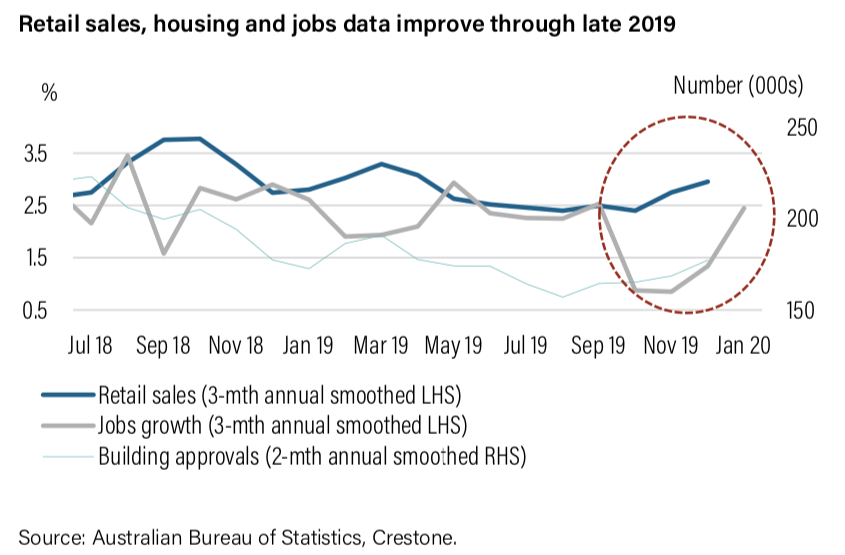

However, the second half of 2019 started with a more positive flavour. Across June and July, the RBA cut interest rates by 0.5%, the regulator eased some lending criteria to support a weakening housing sector, and the Coalition’s tax package passed the Senate, providing some modest income support to middle- and low-income households. By Q4 2019, a range of indicators were proving firmer, leading the RBA governor to contend that Australia was experiencing “a gentle turning point” for the economy.

In particular, Australia’s housing sector showed a much sharper-than-usual recovery through late 2019. Sentiment toward housing investment recovered strongly, as did auction clearance rates, where home prices rebounded at a record pace, rising 11% from their trough in May 2019. After a decline of 30% over the past year or so, building approvals have recovered 6% through Q4, while home lending has risen 21% through the last seven months of the year.

Elsewhere, retail sales improved through Q4, helped by strong Black Friday sales, with volumes rising at their fastest pace in over a year. Unemployment remained steady at a little over 5%, but employment growth remained above trend at around 2.5% into early 2020, with solid gains into January 2020.

New challenges have now emerged for Australia

On the back of the modest uplift through Q3, better data during late 2019 have driven expectations of a return to 2% growth in Q4 (from mid-year’s 1.4% pace). Indeed, the RBA in February retained its forecast for growth to continue accelerating to 2.7% by the end of 2020.

However, despite easier policy and the better global backdrop as we entered 2020, new challenges have now emerged. The devastating bushfires through the summer, and the material shock to China’s growth and global supply chains from the outbreak of the coronavirus, present challenges for Australia in the year ahead. What are the likely impacts from these developments, and can we still expect improving growth through 2020?

Bushfires are expected to reduce growth in Q4 and Q1

Prior to February 2020’s record rainfall across the eastern seaboard—that damped fires and re-stocked dams—fires ravaged many parts of Australia’s rural communities through late 2019 and early 2020. The ferocity of the fires was exacerbated by drought conditions (since early 2017) which, similar to previous droughts, have driven farm output down by about 30%. 2019 was both the warmest and driest year on record for Australia.

Judging the impact of these events on the economy is difficult. As noted by UBS, the direct impact of the bushfires has largely been outside capital cities and limited to regional areas. But the indirect impact of smoke haze on overall consumer confidence has been felt in the largest cities, such as Sydney and Melbourne. Sectors most likely to be impacted include retail (due to smoke haze and people staying indoors), agriculture (due to crops being destroyed), tourism (from lost forward bookings) and construction activity.

According to the RBA, “the direct effects of the recent bushfires are expected to reduce growth across the December 2019 and March 2020 quarters by around 0.2%”. Early evidence of the impact was revealed in December’s retail data where there was particular weakness in the NSW ‘eating out’ category.

There are some clear channels through which the coronavirus could impact Australian growth

The outbreak of the coronavirus (officially called 2019-nCov) remains uncontained at the end of February, with heightened concern in recent weeks that the spread of the virus is accelerating to other regions, namely Italy, Iran and South Korea. Over the past week there has been increasing evidence of containment in China (which still incorporates over 90% of all cases), but there have been few signs that outbreaks elsewhere in the world are slowing.

Our base case remains that the virus’ impact will be largely contained to Q1 2020. UBS research suggests factories are resuming production in late February, albeit well below full capacity. Still, given China’s growing share of world output (18% in 2019, up from 4% in 2003 at the time of the SARS outbreak), weaker Q1 growth in China will have a negative impact on global activity, where the data is likely to be sharply weaker in coming months.

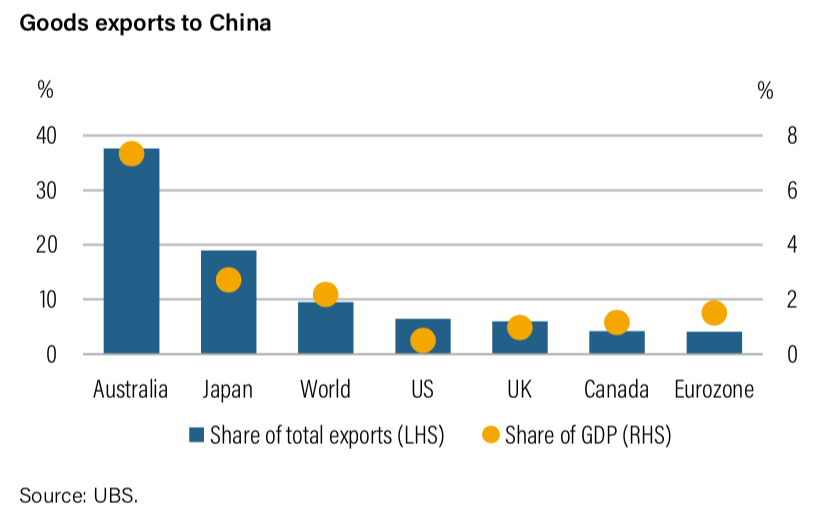

The UBS chart below shows that Australia is one of the most exposed economies to a weakening outlook for China, with more than 30% of total exports going to China, and with China driving about 9% of Australian growth via exports (compared to 1-3% for most other countries).

As CBA highlights, there are some clear channels through which the virus’ outbreak will impact Australian growth via reduced global sentiment and a sharp Q1 correction in China. This would most likely occur in H1 2020:

- Tourism is likely to be the most impacted sector at 3% of Australia’s output and with 15% of foreign tourists from China. Tourism is likely to be sharply curtailed from February through to early Q2. Inbound travel bans for China and Iran are also now in place. Retail sectors particularly targeting tourism will face significantly reduced activity in Q1.

- The education sector is also likely to be negatively impacted, with almost a quarter of foreign students each year coming from China (and education exports worth 2% of output). While this is likely to be temporary, an extended reduction in students could be followed by reduced staffing at major universities.

- The retail sector is also likely to be negatively impacted, as media attention on the virus could lead to consumers being more cautious about social interaction. An associated decline in consumer confidence could also dent households’ willingness to spend. There are obvious implications for the entertainment, gaming and ‘eating out’ sectors.

- Business confidence may also be impacted, as uncertainty about the global outlook weighs on corporate investment, spending and hiring decisions. The interruption to global supply chains could also hamper domestic production and cash flows for Australian companies.

There is a range of offsets to these potential hits to growth

For the tourism and retail sectors, more Australians are likely to holiday at home (with research around the 2002-2003 SARS event showing around 80% of lost tourism was recouped at home). CBA also highlights that the choice of education destination is limited by the tight supply of rated institutions, limiting the medium-term impact of the outbreak. A lower Australian dollar has the potential to offset some of the lost commodity income from lower prices, while additional stimulus in China will add to future growth in China. Data from the Organisation for Economic Co-operation and Development also shows that, excluding mining, Australia has one of the lowest exposures to global supply chains.

How will Australia’s growth unfold through 2020?

Early estimates of the impact of the coronavirus outbreak are now being reflected in modest downward revisions to global growth for 2020. Despite the likely sharp slowing in Q1, most analysts expect prior forecasts for better activity in 2020—post the easing of geo-political tension and stabilising industrial data in late 2019—to now be re-distributed between a weaker H1 but stronger H2 recovery. China forecasts have been cut more meaningfully, with both UBS and CBA reducing their outlooks (from 5.8% to 5.4% and 5.5% respectively). UBS forecasts Q1 growth to slump to just 3.8% in Q1.

For Australia, the combined impact of the bushfires and coronavirus outbreak will likely see growth stall near 0% in Q1 after an expected 0.5% gain in Q4 2019. However, assuming the virus outbreak is contained during Q1, growth should rebound strongly in Q2, potentially by as much as 1.0%. This would see Australia’s annual growth (currently 1.7% in Q3 2019) recover to around 2% mid-2020 and strengthen to 2.0-2.5% in H2 2020.

Australia should benefit from a recovery in the global economy, led by a rebound in activity in China. Global growth is expected to be further supported by 2019’s central bank interest rate easing—the most since the GFC—while governments around the world (including Australia) are now rushing to add fiscal support to their economies (with recent announcements coming from Australia, China, Hong Kong, Malaysia and Singapore). A likely rebound in some commodity prices will help, while Australia’s latest capex survey paints a more upbeat picture for future business investment.

Under this scenario, while the RBA may choose to cut interest rates one final time (0.75% to 0.50%), there is a risk it may hold fire if there are signs the virus is being contained, as well as the combined stimulus of an Australian dollar in the mid-USD 0.60s and likely additional fiscal easing. We expect stronger growth in H2 2020, together with a recovery in global growth, to lift the Australian dollar into the USD 0.70s by the end of 2020. CBA expects the dollar to rise to USD 0.71 by early 2021, while UBS sees the dollar at USD 0.74 by the end of 2021.

How we have positioned portfolios for Australia

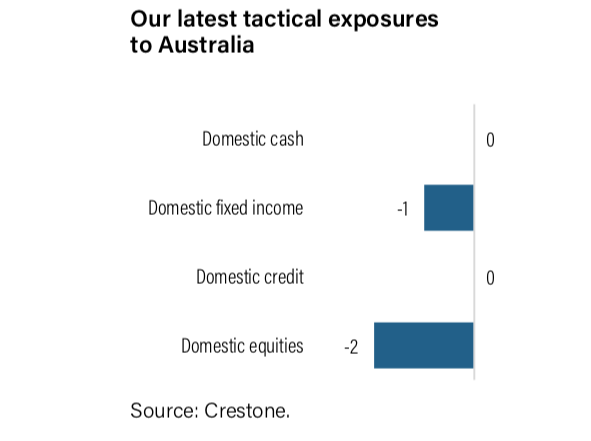

On balance, although we have a relatively constructive view for improving domestic economic growth through 2020, we remain less attracted tactically to both domestic equities and government bonds. Indeed, domestic equities remain our largest underweight within our neutral overall equity position, while we are also moderately underweight domestic government bonds.

Equities–expensive with poor earnings relative to peers

In Australia, the half-year reporting season is largely complete. Despite the virus-led risk-off backdrop over the final week, share price reactions to results throughout the reporting season remained positive. Earnings expectations were also revised only modestly lower by 0.7% to 2.3% for the 2020 financial year, with growth led by industrials and resources, and strong results dominated by large cap companies. Dividends were also solid, though less so than through the prior reporting season.

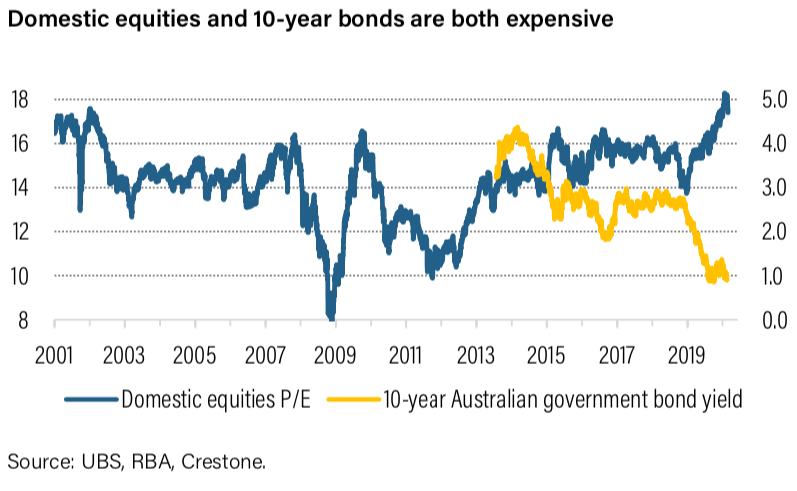

Despite this, we remain underweight domestic equities. Offshore markets are, to varying degrees, fully valued (supporting our neutral, but not overweight, position). But while forward price/earnings (P/E) ratios in the US, UK, Europe and emerging markets are either below or near two-year highs, in Australia, valuations recently breached a 15-year high. Moreover, international markets are better supported by earnings expectations over the coming year of 8-15%. In contrast, the earnings outlook for Australia is a relatively tepid 2-3%.

Fixed income–long-term yields to rise over time

Domestic bonds have rallied to record low yields, tracking international yields lower in the wake of last year’s global growth slowdown, rising geo-political tensions and this year’s coronavirus outbreak. The RBA’s cash rate is at record lows, and the market is pricing for a further two rate cuts in the year ahead, catalysing the expensive pricing for domestic bonds.

In line with international bonds, our central case for a H2 recovery in growth and return to a less risk-off sentiment, should encourage a rising trend for yields by the end of 2020. The focus by central banks on over-achieving inflation targets after years of underperformance also supports an extended period of low policy rates and steepening curves as growth recovers.

We remain neutral domestic corporate credit. Spreads have been relatively tight and unlikely to tighten further. Still, in a sustained low rate environment, where default rates are low, supply pipeline below average and an underlying economy improving, we expect credit to deliver solid risk-adjusted returns.

Learn what Crestone can do for your portfolio

With access to an unrivalled network of strategic partners and specialist investment managers, Crestone Wealth Management offer one of the most comprehensive and global product and service offerings in Australian wealth management. Click 'contact' below to find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment