Economic and market impacts of the upcoming election

Australia heads to the polls this year for a federal election, most likely on 11 or 18 May. While voting intentions tend to narrow and tilt toward the incumbent as polling day draws closer, current voting intentions suggest there will be a change in government this year from the Liberal National Coalition (LNP) to the Australian Labor Party (ALP).

Importantly for investors, the opposition party (the ALP) has a policy agenda that has the potential to significantly impact both the economy and markets. Moreover, the details around the party’s key flagship policies are materially better formed, in some cases in draft policy format, which has not often been the case for opposition parties.

The make-up of the Senate, which will also need to pass new policy, as always, remains uncertain ahead of polling day. Finally, a number of the ALP’s key policies arguably require a financial year start, with the May 2019 timing of the election suggesting these policies are unlikely to come into force, if legislated, until mid-2020.

Are we likely to see a change in government?

When will the election take place?

The latest possible date the election can take place for the Senate and House of Representatives is 18 May. Given the ruling LNP government has scheduled the 2019-2020 Federal Budget release to occur on 2 April, together with the later- than-usual timing of Easter holidays (19-22 April), consensus considers the most likely election date will be 11 or 18 May.

What do the polls say?

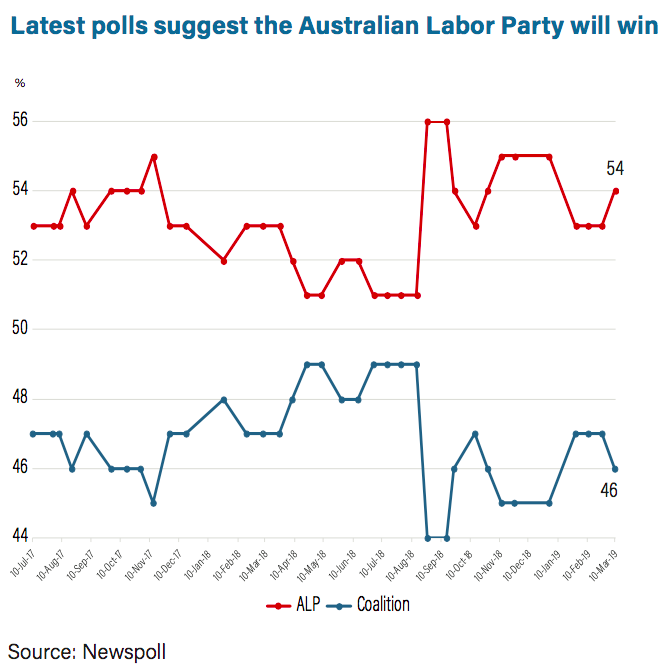

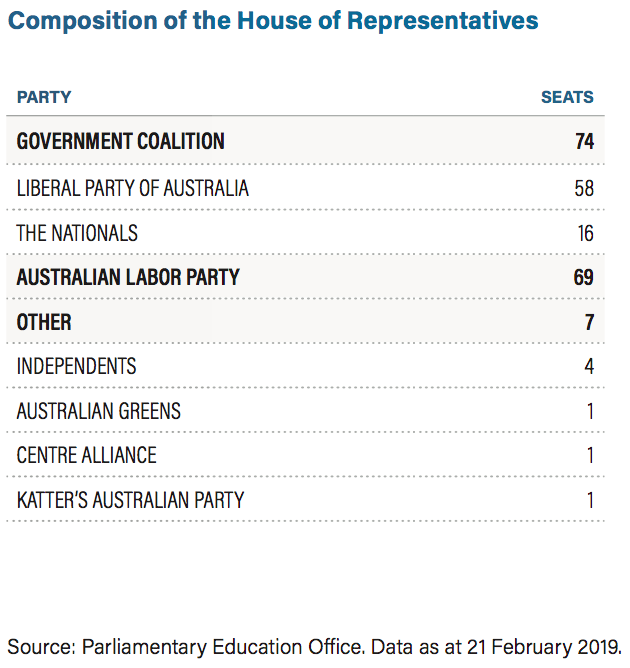

Latest polling points to a defeat for the current LNP government led by Scott Morrison. This reflects a combination of two factors. Firstly, as can be seen in the table below, the current LNP is a minority government (i.e. it does not hold a majority of lower house seats). Secondly, latest two-party preferred polling suggests a significant swing against the LNP, as shown in the chart below.

According to Newspoll, the ALP leads the LNP on a two-party preferred basis by 54% to 46%, while the gap is narrower at 49/51% in the latest Ipsos poll. History shows that voting intentions tend to narrow and lean toward the incumbent as the election draws nearer. However, if current intentions were reflected in May, the LNP would likely lose 15 to 20 seats. This is despite LNP leader, Scott Morrison, consistently polling as the preferred prime minister compared to ALP leader Bill Shorten according to Newspoll (43% to 36%).

Why does the Senate matter?

In terms of assessing any potential change in government, there is the added uncertainty about whether a number of the ALP’s flagship tax reform policies will pass Australia’s Senate. As highlighted in the Australian Financial Review, “an incoming Labor government will struggle to legislate its key tax increases with almost the entire Senate crossbench opposed to its plans to abolish cash refunds for excess franking credits, and none prepared to support the limiting of future negative gearing to newly constructed homes”.

The make-up of the Senate is subject to change following the upcoming half Senate election. In addition, the process of negotiation almost certainly limits the chance of the excess franking credits or negative gearing policy being legislated early enough to start in the 2019-2020 financial year. Finally, the relatively controversial nature of these policies raises the potential for such policies to be altered as parties negotiate changes.

Australian Labor party policy shifts

Materially, the ALP arguably has a longer list of potential policy shifts than previous opposition parties, which are briefly outlined below.

Franking credit refunds

Remove cash refunds for excess franking credits (i.e. franking credits that are not used to offset other tax obligations), with exclusions for charities and pensioners. This is widely viewed to benefit industry and retail superannuation funds over SMSFs. According to Geo Warren from Australian National University, this will reduce the return on an equity portfolio by 1.3-1.4% out of an expected long-run return of 7-8%. According to UBS, this makes the return of excess franking balances via special dividends attractive for investors prior to a possible mid-2020 start.

Capital gains tax discount

Reduce capital gains tax (CGT) discount for future asset purposes from 50% to 25% where investors have held assets for more than one year, reducing the after-tax return on investing.

Minimum 30% tax on trusts

The ALP plans to introduce a minimum 30% tax rate for discretionary trust distributions that occur from 1 July 2019 for beneficiaries over the age of 18.

Negative gearing

The position currently is that an investor can deduct the aggregate of all of his or her investment-related net losses against all other income. The ALP’s proposal to limit negative gearing to purchases of newly-constructed housing could potentially reduce the attractiveness of investing in rental housing and focus investors’ attention on ‘new’ housing stock. At the same time,

it could reduce the attractiveness of geared investments (margin lending) more generally. Policy also includes ceasing depreciation on grandfathered existing dwellings.

Personal income tax

Reintroduce the 2% deficit repair levy for the highest income earners, and permanently reintroduce the 0.5% Medicare levy increase for middle to high-income earners. There is some likelihood the ALP will match LNP tax cuts, potentially re-targeting them to lower income earners. (The LNP’s previously announced tax cuts include reducing middle to lower-income tax obligations by removing an income tax bracket and lifting the thresholds for a number of brackets and increasing low-income tax offsets.)

Low-wage income

Restore weekend penalty rates and potentially increase the minimum wage over time from its ‘safety net’ level to a national ‘living wage.’ Collective bargaining may also be reintroduced in industries with a fragmented (or small) structure, and the casualisation of the labour force may be unwound. These changes could negatively impact businesses with tight profit margins and high wage shares of revenue—although they could also support the economy via higher consumer spending.

Energy

Establish a long-term energy policy with a greater reliance on renewables and more challenging emission reduction targets, as well as new pipeline and processing infrastructure spending.

What does this mean for the economy?

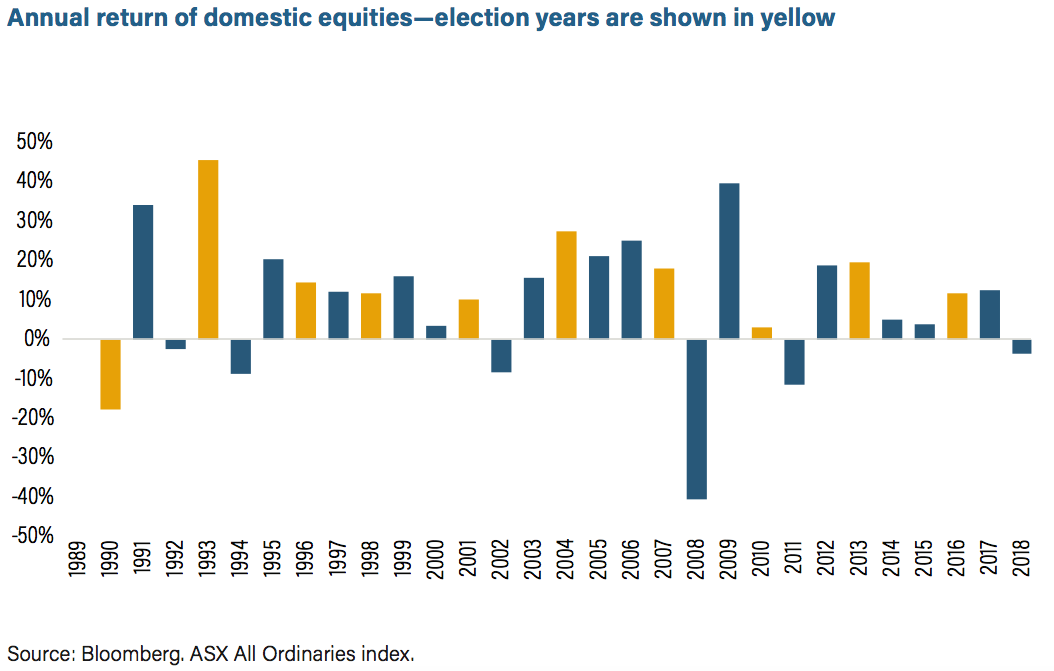

Elections invariably create investor uncertainty, particularly in the lead up to election day. Since the early 1990s, which was the last time Australia was in recession, there have been 10 federal elections. However, despite regular changes between governments of different political persuasions, Australia has enjoyed 27 years of uninterrupted economic growth. Over that period, the domestic equity market has risen, on average, 10% per annum, delivering only seven ‘down’ years. However, only one of these was in an election year (the early 1990s recession). Three of the seven down years occurred in the year following an election, although one of these was the 2008 GFC.

Nonetheless, shifting politics can generate different outcomes for different sectors of the economy—and these differences are not necessarily consistent across decades. A current example may be the likelihood of increased spending for renewables if the ALP were elected this year.

One thing that is reasonably consistent is that elections typically involve additional government spending related to pre-election promises. This can be in the form of consumer tax cuts, infrastructure projects or increased spending on health and education. This election is no different, and we anticipate the economy may well gather some support in the year ahead as the recently improved fiscal war chest is opened by both sides of politics to garner votes. Consumer tax cuts and new infrastructure spending are most likely candidates this election. In addition, according to Credit Suisse research, “history tells us that ALP governments have tended to run larger fiscal deficits on average than their LNP counterparts”. This has been particularly reflected in labour income, often supporting private consumption.

According to Credit Suisse, the ALP is likely to focus more on infrastructure spending targeted at road, high-speed rail and the national broadband network. It has also proposed a 2% cap on health insurance premiums (following rises of more than 4% in recent years) and a taskforce to ensure all the Banking Royal Commission recommendations are enforced quickly. It has also announced an enquiry into after-pay type firms, and there has been speculation that it may, at some point, increase the bank transactions tax levy. Interestingly, although the ALP has traditionally been the party focused on limiting migration, the LNP has announced plans to cap migration flows temporarily.

What does this mean for markets?

Domestic equities

A federal election victory by the ALP could have significant ramifications for several sectors. ALP policies targeting the housing market have gathered the most attention, but there are other policies that have the potential to shape the future direction of sectors and the economy at large. Already, we have seen companies in the advertising sector, such as Seven West Media and HT&E, express that the uncertainty created by the upcoming election could have an impact on volumes and buying decisions. The ALP has already proposed a bank levy of $640 million to fund consumer compensation.

The pledge by ALP leader, Bill Shorten, to make the May election a ‘referendum on wages’ includes several proposals that would have widespread implications across the economy with regards to cost, income, employment, inflation and interest rates. These proposals include restoring weekend penalty rates, moving toward a ‘living wage’ at 60% of the median wage (as proposed by the Australian Council of Trade Unions), and re-introducing some industry-wide bargaining.

Although the economic implications of the above changes are multi-dimensional and difficult to quantify, specific policies targeting particular industries are easier to model. We have outlined these on the following page. Changes to negative gearing and CGT discounts are likely to be the largest and most contentious of the proposed changes.

Opportunities in domestic equities

Broadly speaking, although the impact of these policy changes would only be truly realised in hindsight, there are a number of key thematic opportunities that investors should consider:

Globally-focused companies

Globally-focused companies would be comparative safe-havens relative to domestic-orientated businesses, with little election impact. They receive the dual benefit of no regulatory overhang depressing valuations as well as having largely offshore cost bases (i.e. wages) and less domestically-exposed revenue sources.

Wage inflation

Rising labour costs have already been cited as a factor by corporates. Relatively full employment and a more worker or union-friendly ALP government would likely keep pressure on wages, with the impacts felt most across more unionised sectors of the economy—retail, construction, healthcare, mining, utilities and manufacturing.

Franking balance

The ALP’s plan to abolish cash refunds for excess franking credits would likely see companies respond by releasing credits ahead of reform, either through buybacks or dividends. During the February reporting season, a net 21% of companies surprised relative to expectations suggesting that there could be further releases ahead of any potential changes to legislation. In the near term, investors would likely reward companies with large franking balances and an ability to release them, over those that have more sustainable dividend trajectories. Over the longer term, we favour dividend growers over dividend payers.

Which equity sectors are likely to be affected?

Retail

The restoration of weekend penalty rates and potential introduction of a ‘living wage’ would likely impact unionised and casual workforces the most. To this extent, the retail sector is at risk of a cost impost due to higher wages, as are other unionised workforces, such as construction, healthcare, mining, utilities and manufacturing. Potential election incentives, such as tax cuts or family/low-income subsidies, may provide an offset to this.

Energy—retailing and infrastructure

Although both sides of politics have recently moved closer on matters such as default market offers, differences remain regarding renewables targets and emission reductions. Broadly speaking, the ALP has pledged lower energy prices. Coupled with more renewables generation, this is a likely earnings headwind for energy retailers. The ALP has outlined a $15 billion plan for new pipeline and processing infrastructure spending which could benefit upstream producers.

Builders and developers

If negative gearing and CGT changes impact re-sale values, there is a risk that new dwelling construction would be impacted, leading to a volume impact on companies exposed to residential construction. If the ALP’s negative gearing policy results in more limited supply, it could make the build-to-rent offering more viable.

A potential offset, however, are commitments from both parties to continue to fund major infrastructure projects. This would mean that non-residential construction may offset any weakness in residential.

Banks

This is arguably the most impacted sector of changes to negative gearing, CGT and franking credits. Although the current government’s acceptance of the Banking Royal Commission recommendations reduces some potential risk, the ALP’s planned introduction of a $640 million bank levy (and the Australian Greens’ call to triple it) highlights the sector’s vulnerability.

Health insurance

The ALP plans to implement 2% average price caps on the health insurance industry from 1 April 2020 till 31 March 2022. With margins in the low single digits, capping premium rate increases at a time of rising costs is expected to lead to a continued and renewed focus on costs. This may be through the adoption of artificial intelligence and other processing efficiencies.

A-REITS

Changes to negative gearing and CGT would significantly impact after-tax returns of investment property, as well as the residential construction, developer and banking sectors. Although the magnitude of the impact on residential pricing and construction is unclear, apartments and property trusts exposed to investors are likely to be most affected.

Diversified financials

The ALP may look to more strictly enforce the Banking Royal Commission recommendations on retail superannuation funds given its preference toward industry super funds.

Fixed Income

The uncertainty of a new government could create volatility in equity markets and risk assets, creating a bid tone to investment-grade and sovereign bonds. If the ALP were to remove negative gearing, a potentially weak housing market could continue, keeping short-term interest rates low and fuelling a bid tone to duration. However, fiscal stimulus and an increase in infrastructure spending could see government bond issuance at the longer end of the curve increase, which would steepen the yield curve. We recommend a position in investment-grade credit in the mid part of the curve (i.e. out to five years), which would help to protect capital with a steady income stream.

Basel 3 compliant mandatory convertible securities (hybrids) issued by banks have already come under pressure. The widening of credit margins in 2018 from low 3% to 4% was arguably driven by concerns regarding the Banking Royal Commission and the announcement from the ALP to abolish excess franking credits. However, since the release of the Banking Royal Commission’s recommendations, credit margins remain elevated. We believe, therefore, that ALP policy around franking credits is now all but priced in by the market, and those accounts that would be a ected have likely already acted. Any further widening in credit margins on a new issue would only benefit the majority of accounts that still pay taxes—and such yield-hungry accounts would quickly absorb the new supply in a low interest environment.

This wire is an extract of Crestone's Federal Election 2019 - Preparing for Change/ March 2019. To read the full article please click here.

Never miss an update

Stay up to date with the latest news from Crestone by hitting the 'follow' button below and you'll be notified every time we post a wire.

Want to learn more about Crestone Wealth Management? Hit the 'contact' button below to get in touch with us or head to our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

2 topics

LGT Crestone

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

LGT Crestone

Private wealth advice for high-net-worth and ultra-high-net-worth families, family offices, and for-purpose organisations.

Comments

Comments

Sign In or Join Free to comment