Inflation: no room for complacency

The recent uptick in global market volatility has been driven by fears about price pressures and inflation. My colleague, investment director Andy Budden, answers questions about the inflation outlook and reflects on its implications for different asset classes.

We’ve seen greater market volatility of late. What are your views?

Global trade issues aside, two other reasons stand out: higher inflation expectations and shifting monetary policy. Financial markets are coming to terms with the idea that the environment of low inflation and low growth is giving way to one of continued economic growth in many parts of the world and emerging inflationary pressures. That is likely to be good news for investors.

For years, disinflationary pressures have persisted across many economies, largely driven by weak economic growth and softening commodity prices. Central banks have been trying (with limited success) to push inflation back to their targets with unconventional monetary policy. However, monetary policy normalisation is now underway as inflation and economies return to more normal conditions. These are welcome developments for the world economy.

From a long-term investment and portfolio construction perspective, it is important to be aware of this fundamental change in the economic and investment landscape.

What’s behind the rise of inflation and where is this headed?

The gradual increase has been consistent with a broad global economic recovery, as alluded to above. For the first time in a number of years, most of the world’s major economies are experiencing sustained economic growth. China’s growth, for example, should stay above 6% this year. Europe’s economic expansion may have started to slow but is likely to stay moderate. Growth momentum in the US is expected to be healthy in 2018 and into 2019. The Australian economy, too, is forecast to grow above potential over 2018.

These trends are constructive – so long as inflationary pressures and interest rates do not rise too rapidly. They are not expected to. In Australia, short- term inflation expectations have edged up. But they are still within the Reserve Bank of Australia’s annual inflation target of between 2% and 3%. The central bank, having kept interest rates at an all-time low of 1.5% since mid-2016, has indicated that monetary policy is likely to stay unchanged in the near term.

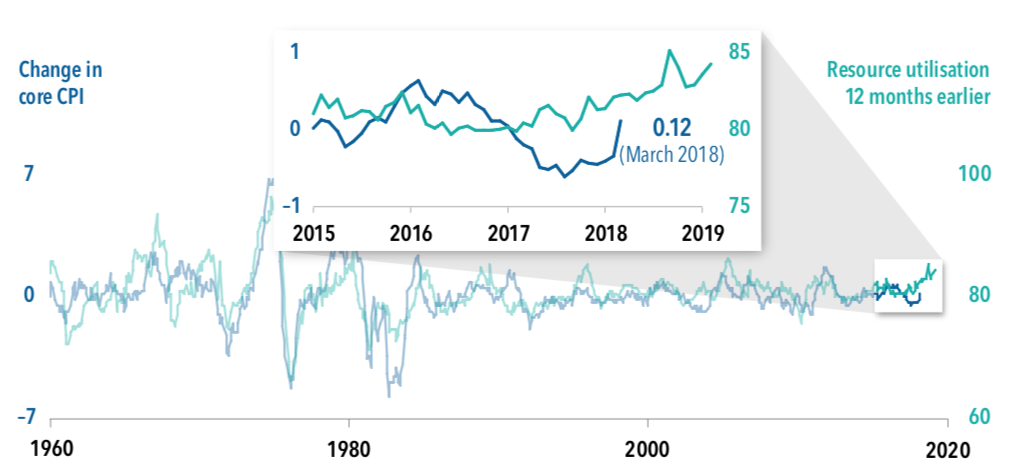

In the US, where inflation concerns have stoked a rise in 10-year Treasury yields, the Federal Reserve (Fed) is on pace to hike interest rates gradually through the end of 2020. That said, data points, such as the resource utilisation rate, suggest that inflation may be increasing and could have an impact on the speed with which the Fed raises interest rates in the next couple of years. The upshot is that investors may have to reassess the trajectory of Fed policy.

All told, there is no room for complacency. For example, US fiscal stimulus via tax cuts and increased spending in an economy operating at capacity could skew inflation risks to the upside. Other developments that are worth watching include oil prices, trade disputes, and the Phillips Curve – which links falling unemployment to higher wages and prices.

Higher resource utilisation could help pull US inflation higher

As at 31 March 2018. Resource utilisation is a weighted average of ISM vendor performance index and the employment rate. Sources: Capital Group, Bureau of Labor Statistics, Institute for Supply Management (ISM), Thomson Reuters

Is it true that inflation is bad for stocks?

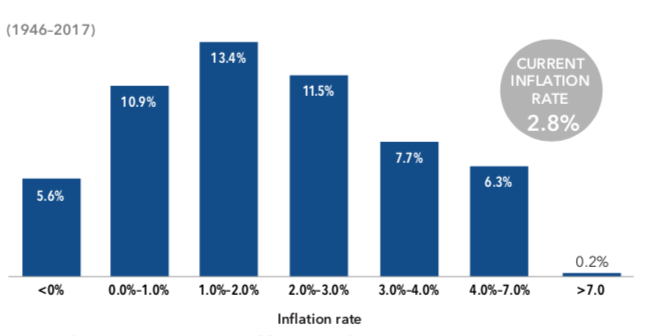

That’s not always the case. An environment of firmer inflation has been good for equities, and could be again. If you look at how stock markets have fared over multiple cycles, you’ll see that, at moderate levels, inflation has tended to be fairly good for equity returns.

For instance, since 1946, the Standard & Poor’s 500 Index has enjoyed double- digit returns in years with inflation between 0% and 3%. In fact, it has even had above-average gains in the majority of years when inflation ranged from 3% to 4%. To be sure, inflation is not the sole driver of market returns. But it’s good to know that a modest rise in inflation has often been consistent with strong investment returns.

In a similar vein, a rising rate environment does not always translate into declines in stock prices. Much depends on why interest rates are moving up. If it is because of healthy economic activity, then stocks can rise alongside higher rates.

Inflation need not act as a drag on equity markets

Average annual S&P 500 price return in various inflation environments

Current inflation rate as at 31 May 2018. Returns are in USD terms. Sources: Capital Group, Bureau of Labor Statistics, RIMES, Standard & Poor’s

But will bonds lose value if rates rise?

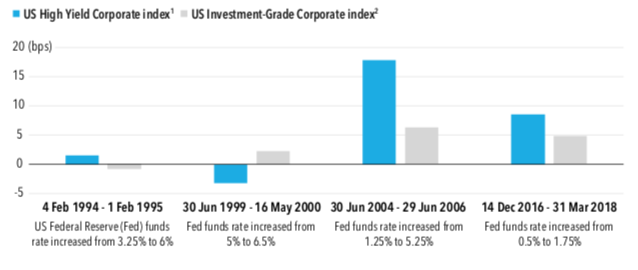

That is somewhat misguided too. Not all bonds are hurt as rates increase, especially if rate rises are gradual and widely anticipated. Price declines can be moderated by interest income. Looking at the past couple of Fed tightening cycles, investment-grade bonds have often delivered positive returns. Corporate high yield has also held up well. And encouragingly, credit fundamentals remain, by and large, stable and default rates are still relatively low.

Emerging market debt is another area that can potentially offer an attractive risk-return trade-off. Having undergone profound changes, economic and monetary cycles in emerging market economies are much less closely tied to the US today than in the past. Many are at the early or middle stages of their economic growth cycle, and have corrected or improved debt imbalances that led to vulnerabilities in previous global sell-offs. Additionally, they have benefited from a growing and more stable domestic investor base. Overall, the asset class has become more liquid and appears well positioned to handle modestly higher US yields.

Myth: bonds have to suffer losses when short-term rates rise

Date as 31 March 2018. Cumulative data based on monthly returns in USD terms. Sources: Bloomberg Barclays, New York Federal Reserve, (VIEW LINK). Bloomberg Barclays US Corporate High Yield 2% Issuer Capped Index. 2. Bloomberg Barclays US Corporate Investment Grade Index.

So how can advisors and end-investors adapt to today’s environment?

Consider allocating to both equity and fixed income, or continue to do so, as part of a long-term, diversified investment strategy. Apart from providing income and capital preservation, bonds can also cushion equity volatility and add balance to a portfolio. That fundamental relationship remains unchanged. On the equity side, ensure portfolios have flexibility to pivot to select areas of opportunity. Importantly, seek good companies that can thrive irrespective of market cycles, low or high inflation environments. Consider, for example, opportunities arising from secular trends, including shifting global trade patterns, digital disruption and the changing global consumer.

Also, be mindful that active strategies are better equipped to cope with changing macro conditions. As the stability of markets gives way to periods of episodic elevated volatility, stock pickers could take advantage of the greater dispersion in stock movements to generate excess returns and protect capital in falling markets. Likewise, selecting fixed income investments based on bottom-up, fundamental research and appropriate risk evaluation can potentially offer greater resilience during volatile periods.

The importance of a long-term horizon cannot be understated. Trying to adjust an investment strategy for every short- term market gyration is not only fraught with danger, it can also be costly. And finally, for advisors, look at the long-term track records of asset managers. Having managed through different types of cycles, be they economic, market, or geopolitical, today’s environment is not new to us. It could be new territory for other asset managers, however. Many of them have limited experience in managing outside a low or declining inflation environment.

© 2018 Capital Group. All rights reserved. CR-327001 AxJ

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Paul Hennessy is managing director, Australia & New Zealand, at Capital Group. As a relationship manager, he is responsible for covering the institutional client base in Australia and New Zealand. He has 33 years of investment industry experience and has been with Capital Group for eight years. Prior to joining Capital, he was head of Australian and New Zealand distribution for Macquarie Bank’s fund management division. Before that, he was global head of relationship management for Macquarie Securities and CIBC World Markets in North America.

2 topics

1 contributor mentioned

Paul Hennessy is managing director, Australia & New Zealand, at Capital Group. As a relationship manager, he is responsible for covering the institutional client base in Australia and New Zealand. He has 33 years of investment industry experience...

Expertise

Paul Hennessy is managing director, Australia & New Zealand, at Capital Group. As a relationship manager, he is responsible for covering the institutional client base in Australia and New Zealand. He has 33 years of investment industry experience...

Expertise

Comments

Comments

Sign In or Join Free to comment