Inflation - still no lift-off, but not all gloom...

Vimal Gor

Pendal Group

Within the latest inflation figures lies some critical data: While the breadth of low inflation items is an ongoing concern, the RBA should be encouraged by higher non-tradable inflation and a few early signs from the housing sector.

Inflation for the September quarter came in marginally lower than expected at 0.6% headline and 0.4% underlying. This leaves annual headline at 1.8% and underlying at 1.9%.

Whilst the headlines were grabbed by the expected sharp increase in Electricity prices (+8.9%) and sharp decline in Vegetables (-10.9%) these are trimmed away in the underlying numbers, where the RBA focuses. Food, beverages and tobacco make up 24% of CPI so the majority of trimming is found in the sub items in these groups, both to the upside and downside. Throw in automotive fuel (3.55% weight) and the other “energy” called utilities (3.6%) and you are at the 30% mark, so we generally end up with the trimmed mean being effectively like the US underlying called “ex food and energy”.

Where could the RBA take some encouragement?

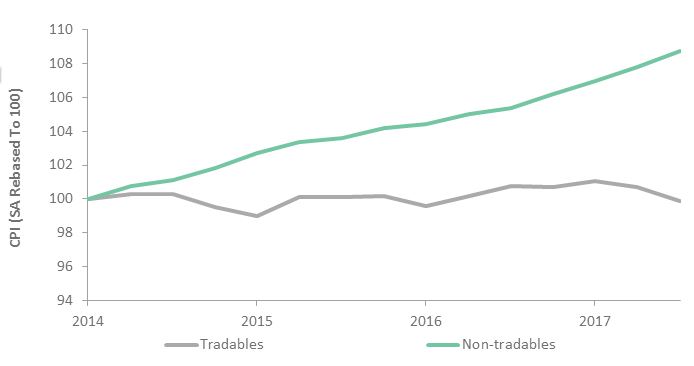

The main area the RBA would take some encouragement is in the performance of non-tradables.

Seasonally adjusted non-tradable inflation was the highest since Q3 2013 at 0.86%. The lower inflation number was again due to tradable deflation being at its lowest since Dec 2014 at -0.78%. In fact tradable inflation has been flat net on net since March 2014. In the same period non-tradable is up 8.7%. The RBA only really influences non-tradable inflation and is a price taker of tradables. Therefore, if there were to be some global inflation generated by the pick-up in global growth this year, it would feed through to Australia’s inflation outlook.

Chart 1: Tradables inflation continues to lag its non-tradables counterpart

Source: ABS

Source: ABS

The second area of encouragement is housing. Of the 70% of CPI which generally makes up underlying inflation, housing dominates. Rents (6.7%), New Dwelling Purchases (8.67%) and Maintenance and Repair (2%) are 17.3% of overall CPI, but therefore usually 25% of underlying. So any big theme in housing should drive underlying inflation. In this regard there are a few early but encouraging signs. New dwelling purchases were up 0.8% q/q and 3.1% y/y, showing ongoing high housing construction numbers are having an impact. Rents remains subdued overall, but vary across major cities. Increases are relatively strong in Sydney, healthy in Melbourne but turning negative in Brisbane as the much talked about oversupply bites. Perth should see some recovery from recent declines. Continuing strong immigration numbers should see rents hold up in general.

Delving deeper into the capital cities, the major drag on inflation has been from Perth and Darwin (less than 1% CPI annually). Brisbane has begun to recover and given recent employment data there are hopes Perth and Darwin may follow. Adelaide and Hobart have largely caught up with Sydney and Melbourne (at around 2%), which highlights reason for hope. Although not a major change, the recovery of the mining states could see inflation settling back in the lower end of the 2-3% band.

What would discourage the RBA?

The breadth of low inflation is the main area of concern. The ANZ Diffusion Index showed only 26% of items had a quarterly annualised price increase of 2.5% or more. The main culprits were again retail-led, with a majority of items experiencing falling prices. The AUD was stronger across the majority of the quarter and is currently weakening but recent experience has shown little currency impact on goods prices. Much has been written about structural changes in retail and the evidence suggests it will continue to weigh on inflation for a number of years yet.

Where does this leave the RBA?

The RBA will remain on a watching brief into 2018. The wage data on 15 November will be the next piece of information and given the minimum wage increase of 3.2% hits the Q3 numbers, it should show an uptick. Whether this feeds into inflation immediately is doubtful, but it would help the narrative of a slow but gradual pick up in prices, which took a hit with the CPI numbers. As there is no January RBA meeting they will have the Q4 CPI numbers (due out 25 January) by their first 2018 meeting and for their February bi-annual Parliamentary Economics Committee Update. They will likely want to open the New Year on a positive note, but the Q4 CPI numbers will hold the key as to whether that positive note may include firmer hints of tighter monetary policy into 2018. With other central banks easing back from monetary stimulus, the RBA would be hoping to follow suit at some point in 2018. We will be watching closely for clues as to when that might be.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

1 topic

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Vimal Gor

Head of Income & Fixed Interest

Pendal Group

Appointed Head of Income & Fixed Interest in June 2010, Vimal is responsible for setting strategy, processes and risk management. He oversees $16.4 billion invested across Income, Composite, Pure Alpha, Global and Australian Government strategies.

Expertise

Comments

Comments

Sign In or Join Free to comment