Is it time to buy resources stocks?

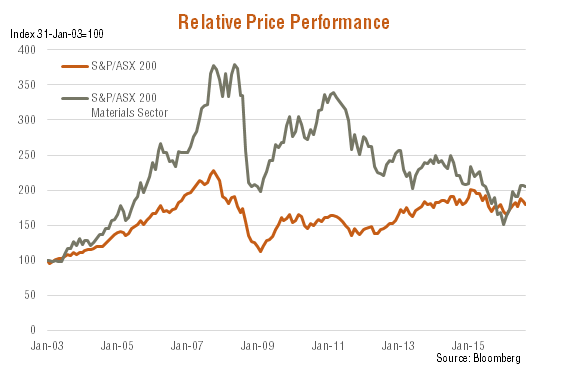

The Australian materials sector (largely comprising our major miners) has performed relatively well so far this year due to firmer commodity prices and a relatively benign United States interest rate outlook. Although valuations in the sector appear high, they might be justified if commodity prices hold up near current levels and miners are able to keep a tight rein on costs. As seen in the chart below, the materials sector has had a tumultuous ride over the past decade thanks to the boom and bust in the commodity price cycle. As has already been evident several times over recent years, the sector has attempted another feisty comeback so far this year. From end January to latest data on 20 September, the materials sector is up around 35% in price terms, compared to a gain of only 5.8% for the S&P/ASX 200 Index.

Past performance is not an indicator of future performance

Valuations Are Already High

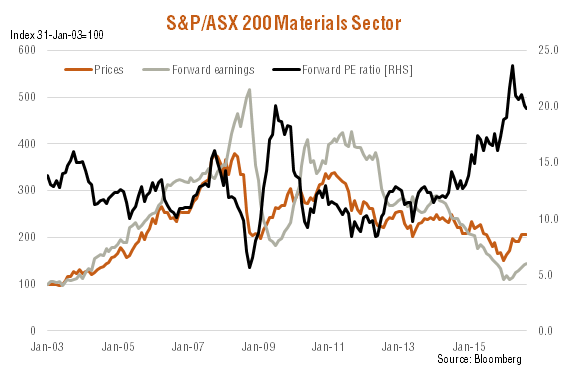

Having reached a low of only 8.5 times forward earnings in mid-2012, valuations in the materials sector have been rising consistently in recent years, with sector prices refusing to fall as fast as the commodity-price driven decline in forward earnings. The rebound in prices earlier this year only pushed valuations even higher, with the forward PE ratio reaching an end-month peak of 23.7 at end-April 2016 – compared to an average since the start of 2003 of only 13. That said, valuations have since edged down, as the recent rebound in forward earnings has outstripped the growth in share prices. Given still high valuations, however, whether price gains in the sector can continue will crucially depend on whether forward earnings can continue to grow.

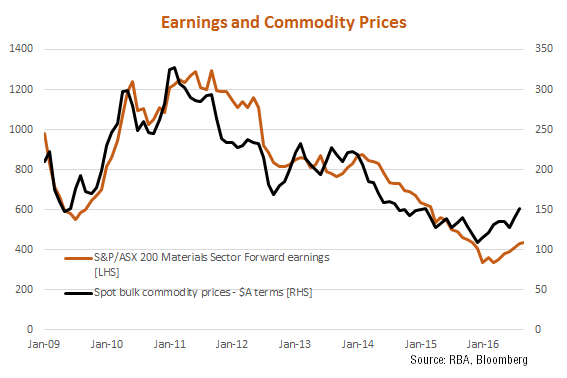

On this score, it’s worth considering the link between forward earnings and commodity prices. As seen in the chart below, there has been a reasonably strong correlation between spot bulk commodity prices in $A terms (largely coal and iron ore prices) and material sector forward earnings. If the recent rebound in commodity prices is sustained, and especially if they rise further, there would seem scope for further “catch-up” gains in forward earnings.

Can commodity prices hold up? A major factor supporting commodity prices of late has been cut backs in high priced Chinese iron ore production. What’s more, China is continuing to support infrastructure and housing developments, given the weakness in its once strong export sector. Against this, however, supply from major exporting nations such as Australia and Brazil continues to rise. It also remains the case that China is suffering from excess industrial capacity, and at best steel production seems likely to level out (if not fall) rather than continue to rise strongly.

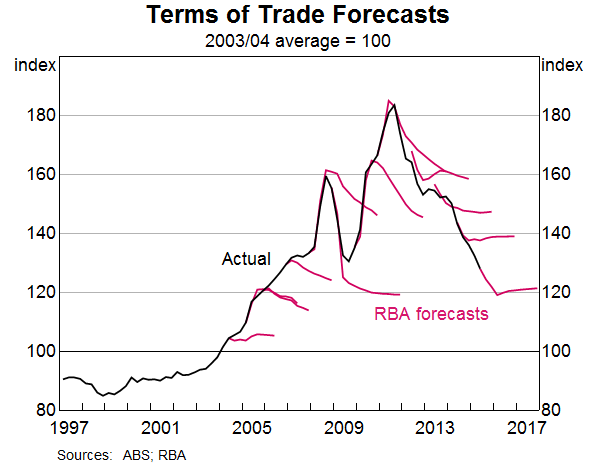

According to the RBA’s latest forecasts, Australia’s terms of trade (price of exports relative to imports) are now close to bottoming out. While that’s a positive first step, it’s still not consistent with a resumption of the commodity bull market enjoyed earlier last decade. What’s more, the RBA’s track record in forecasting the terms of trade in recent years has been just as bad as most other forecasters.

As and when the US Federal Reserve resumes its policy of raising interest rates, moreover, this could also place upward pressure on the US dollar, and in turn further downward pressure on commodity prices.

All up, high materials sector valuations, rising commodity supply, Chinese industrial overcapacity, and the threat of higher US interest rates still suggest some caution is warranted with regard to the Australian materials sector. That said, it is true that commodity prices have been rising so far this year, and at current levels, there remains scope for further gains in forward earnings which could still also be consistent with further gains in the materials sector.

Contributed by BetaShares: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

1 topic

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment