Is Telstra’s dividend sustainable?

We added Telstra (TLS) to the Income Portfolio this week and wanted to provide some more detail around the sustainability of the dividend in the first instance, then the scope for improvement in the share price thereafter.

TLS reported FY20 earnings mid-August, they met expectations for the current year however they poured cold water over earnings guidance for FY21. They maintained the dividend at 16c; however this is made up of 10c ordinary and a 6c special which is related to NBN payments. The concern is that the ‘real’ dividend will be closer to 10c than 16c however in MM’s view that’s unlikely.

If we’re right, TLS paying 16c into the future has it on an attractive yield of 5.5% plus franking.

On an earnings basis, the 16c dividend is not sustainable given TLS will likely generate around 14c EPS in FY21 & FY22 before rising from there, however TLS have shifted their dividend focus to be more heavily aligned with free-cashflow (FCF).

In terms of that number, which seems to now be the key for the dividend, it’s expected to be around 23c in FY21 & FY22 and rising from there.

What is free cash flow? Free cash flow (FCF) represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets. Unlike earnings or net income, free cash flow is a measure of profitability that excludes the non-cash expenses of the income statement and includes spending on equipment and assets as well as changes in working capital from the balance sheet.

Given the rhetoric around free-cash-flow that we saw at the recent result, it seems likely that the market is too bearish on the sustainability of the TLS dividend given its being anchored to EPS, not FCF. While earnings are under some pressure, they are expected to improve over the coming years (I know I know – it’s been like this for ever), however worth bearing in mind that TLS have made some tough decisions in recent times to get the business on a better footing to deliver that much anticipated growth.

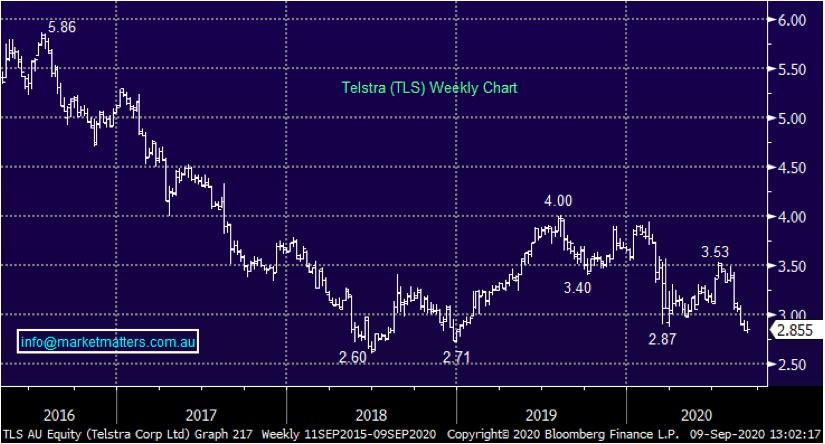

In broad terms, a sustainable dividend we think is enough to support the share price up to about a 4.5% yield which equates to a SP around $3.50, then if earnings can show some growth, we think there is a very plausible path for TLS to trade back up towards $4.00.

MM is bullish Telstra (TLS) for income

Telstra (TLS) Chart

Conclusion

We are confident in the sustainability of Telstra’s yield

Register for a free trial to Market Matters

At Market Matters, we write a straight-talking, concise, twice daily note about our experiences, the stocks we like, the stocks we don’t, the themes that you should be across and the risks as we see them. Click here for your free trial.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

........

Any advice provided is of a general nature only.

1 topic

1 stock mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment