Is the Rebound Risky?

“In finance, everything that is agreeable is unsound and everything that is sound is disagreeable.” Winston Churchill

With the S&P 500 Index enjoying a rebound of ~28% from the low of late March it may well feel like the worst of the Covid19 hit to markets is behind us.

But is the rebound reflective of the entire market? At heart, the index is an instrument to reduce risk via diversification. As of today however it is not doing that.

In fact over 50% of investors in the US stock market are passively following the index, through various index funds. Meaning the recent rebound has accelerated concentration and valuation risk.

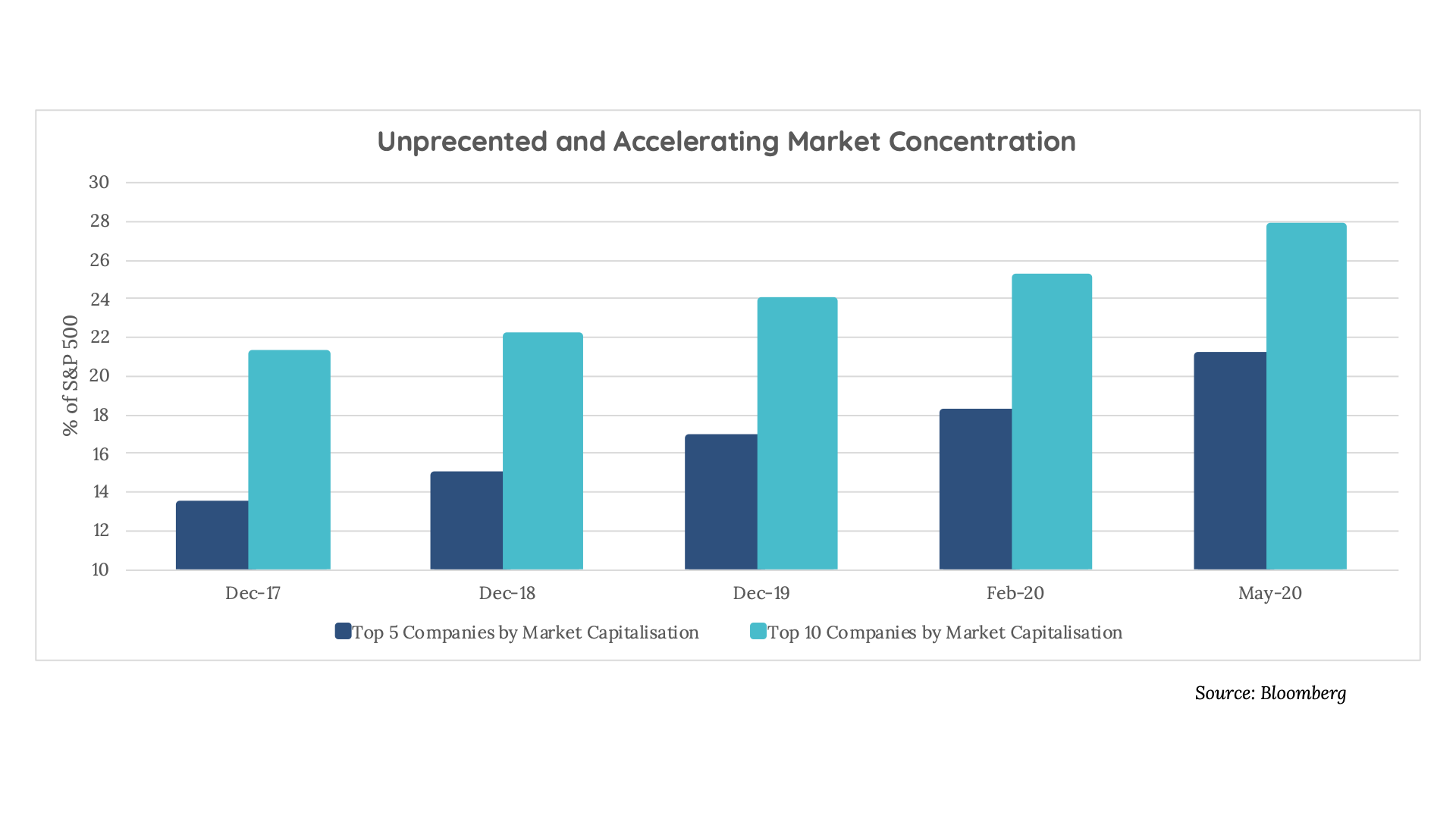

The largest 5 companies now account for over 20% of the index, the top 10, nearly 28%.

The S&P 500 has never had this level of concentration.

Or to put it another way, only 2% of companies equate to 28% of the index.

As at 12 May 2020, having 28% of your portfolio concentrated in the largest 10 stocks was insufficient to beat the index. Rather, an investor would likely require concentration of over 40% of their portfolio in these stocks. Such a portfolio would have a very large relative bet on the highest priced stocks - which are majority owned by totally price insensitive passive shareholders.

Clearly benchmarks are rapidly “UNdiversifying.”

The lessons of price insensitive buyers in history - such as those in the 1960’s or the 1990’s Dotcom Bubble are pretty clear – when the market turns there’s nowhere to hide. This can be further amplified if large institutional investors in these stocks all exit at the same time, exacerbating the price decline.

But how likely is this?

Times are still uncertain, so to that end, a lot of things are possible. But what’s likely given an unprecedented shut down of the global economy, record high unemployment levels, slashed dividends and no imminent vaccine is this still has a while to play out.

If the benchmark is your yard stick at this point be sure you’re comfortable not being diversified.

What’s the alternative?

Perhaps index creators will need to cap weightings of stocks in benchmarks - which would be terrible for the index returns and undermine the Federal Reserve’s stated aim of increasing asset prices. Or, the index could simply continue to UnDiversify in which case it needs to be renamed - as it simply isn’t a benchmark for the stock market.

Current consensus expects the top 5 S&P 500 companies to add almost $700bn of additional revenue over 5 years – and $150bn in 2024 alone. This is more than the combined revenue base of Johnson and Johnson, Pfizer, JP Morgan, Caterpillar, Goldman Sachs, American Express, Starbucks, McDonalds, Visa, Kraft Heinz, Coca Cola, General Electrics and Nike. And that is simply the embedded expectation.

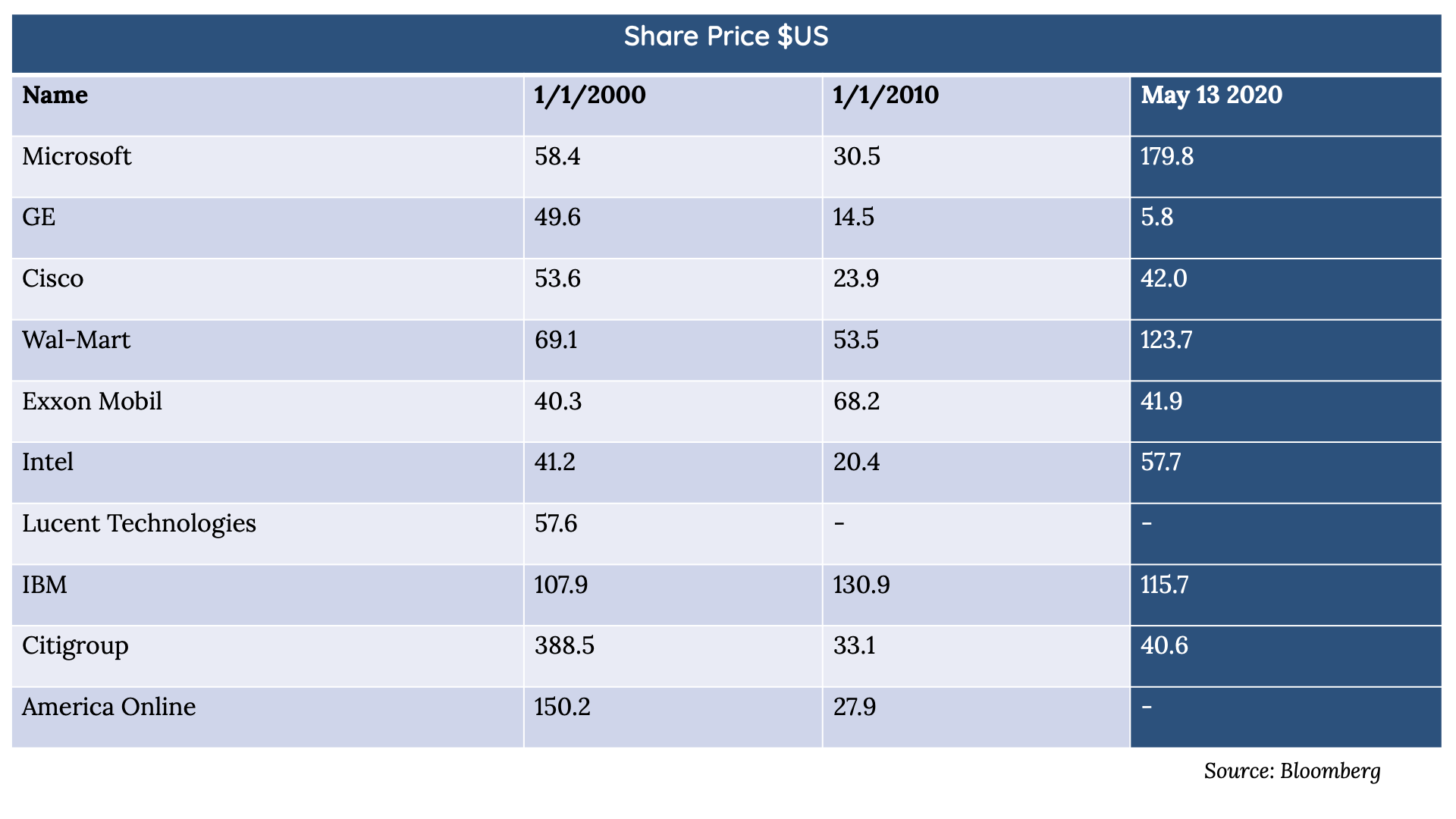

Lack of diversification is a bad thing in many parts of society, including finance. In 2000 the top 10 stocks in the S&P 500 represented 24% of the index... Of those – 8 were lower in absolute terms 10 years later and 5 were lower 20 years later.

That is why the current concentration of a few companies dominating the market is ultimately a bad thing for investors in the market as a whole – creating less diversification and higher prices.

But there are alternatives, including diversifying across sectors and geographies, and favouring active managers over passive index funds.

Especially during uncertain times like these, it pays to diversify.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase the certainty of global equity returns for investors through its:

> Unique and structurally lower-risk investment approach that combines capital growth and income generation to deliver a more consistent return profile (smoothing).

> Portfolio of up to 45 large, globally listed companies.

> Internationally experienced and personally invested leadership team.

www.talariacapital.com.au

........

The information in this article is general information only and is not based on the objectives, financial situation or needs of any particular investor. In deciding whether to acquire, hold or dispose of the product you should obtain a copy of the current Product Disclosure Statement (PDS) for the Fund and consider whether the product is appropriate for you.

Wholesale Units in the Talaria Global Equity Fund (the Fund) are issued by Australian Unity Funds Management Limited ABN 60 071 497 115, AFS Licence No. 234454. Talaria Asset Management Pty Ltd ABN 67 130 534 342, AFS Licence No, 333732 is the investment manager and distributor of the Fund. References to “we” means Talaria Asset Management Pty Ltd, the investment manager. A copy of the PDS is available at australianunity.com.au/wealth or by calling Australian Unity Wealth Investor Services team on 13 29 39. Investment decisions should not be made upon the basis of the Fund’s past performance or distribution rate, or any ratings given by a rating agency, since each of these can vary. In addition, ratings need to be understood in the context of the full report issued by the rating agency itself. The information provided in the document is current at the time of publication.

4 topics

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Chad is the Co-Chief Investment Officer and co-founder of Talaria Asset Management. He has more than 21 years of experience in the financial services industry in the UK, South Africa and Australia. Talaria's investment strategy seeks to increase...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management