Is the Resource Sector Finally Hotting Up?

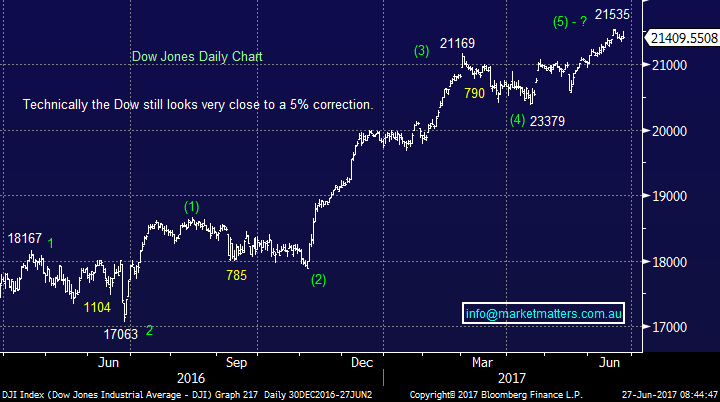

A weak session for the local market yesterday with early optimism fading throughout the day and the market limped into the close. A similar session played out in the US overnight with markets giving back early gains to close fairly flat for the DOW and S&P 500 while the Nasdaq ticked in the red. The DOW closed ~100pts from its high and we continue to think the US market remain vulnerable in the short term, although no sell signals are generated until the DOW breaks below 21000. Expect our market to open flat this morning with BHP up a few pts.

Dow Jones Daily Chart

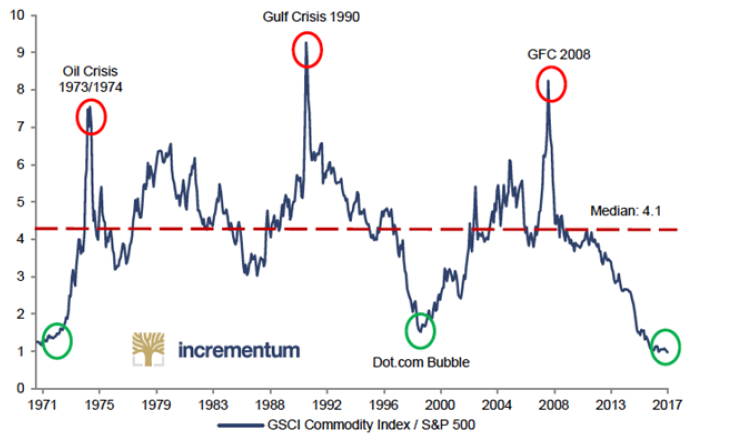

Locally the market continues to underperform with stocks down by 1.01% last week versus the US which was up by 0.30%, however we’re starting to see some interesting trends bubble away in terms of commodities, ahead of what’s a typically strong period for our miners. In early 2016 commodities started a strong bull run as optimism around global growth picked up, Trump won the election and that pushed commodity stocks up into a January 2017 high. Since then, commodity stocks have been under pressure around the globe and the Australian miners have felt the brunt of it, however this period of consolidation / weakness now look done and opportunities are popping up.

According to a number of different measures, commodities are now cheap, in fact they are the cheapest they have been relative to the S&P 500 in history.

Rio Tinto (RIO)

Rio Tinto (RIO) is orchestrating a bidding war for its Hunter valley coal mines, with both Glencore and China’s Yancoal desperate for the assets – so much for Coal being a dead duck! On Friday, Glencore upped its bid to more than $3.5bn trumping Yancoal’s current proposal by around ~$300m, however at the stage RIO is sticking with the Yancoal bid, one of its largest customers. It’s clearly an interesting predicament. Glencore’s bid is largely unconditional, they’ll pay a $225m none refundable deposit and the deal will likely complete, plus RIO would rather sell to a competitor than a customer, given the potential impact on future coal prices (if sold to a customer). Yancoal’s bid is conditional and they may have more difficulty getting regulatory approvals, however if RIO snub them, they’ll upset their biggest customer, not to mention the Chinese Govt.

Whatever the case, the deal will likely be done, the price for RIO will be good and this opens the door for further capital management for the miner. We own RIO and remain comfortable with our 5% holding

Rio Tinto (RIO) Weekly Chart

BHP Billiton (BHP)

A weak Oil price of late has been a drag on the BHP share price as the market has seemingly lost focus on Elliot’s proposal for the big Australian Miner. Elliot first made their views public with a release on the 10th April and the BHP share prices closed just below ~$26 that day. The proposal which included a number of aspects such as a single listing and spinning off some assets, detailed a valuation on BHP assets of around ~$US27, or in Australian Dollar terms around ~$38. Since then BHP has only tracked lower closing yesterday at $22.45. Elliot are a credible outfit and they put their money where their mouth is.

We hold BHP from ~$24, which in hind sight, was a tad early however we remain comfortable with our 7.5% holding.

BHP Billiton (BHP) Weekly Chart

Fortescue (FMG)

Clearly a more volatile proposition, however we’ve had good success with Fortescue over the past few years. The recent high above $7 was a shorting opportunity that we took advantage of and we now see Fortescue as a higher risk buy. Iron Ore prices have obviously been weak and we’ve now see brokers downgrade their earnings assumptions for FMG, however the share price is already down 40% from the highs – we think these downgrades have already been factored in.

We hold FMG from ~$4.66 and remain comfortable with our 5% holding.

Fortescue Metals (FMG) Weekly Chart

Summary

· We remain comfortable holders of BHP, RIO and Fortescue (FMG).

· For those looking for buying opportunities, these 3 stocks look good at current levels.

· July is typically a good time for the miners.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

1 topic

3 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment