It’s getting harder to be a Viva believer

Viva Energy has had a horrid start to public life. It is getting harder to be a believer. But for the time being, we are hanging on – just!

Firstly the refining margin collapsed and when it did recover, Viva experienced an abnormal power outage at the Geelong refinery. Then Viva got caught up in a well-publicised spat with their biggest retail client Coles. And finally this week, we see that the general fuel market has been softer than forecast, driven by the unpleasant combination of a rising oil price and a declining currency.

This situation reminds me of a company we invested in several years ago which experienced problem after problem for nearly 18 months. Management was exceptionally proficient at explaining each problem and why it wasn’t their fault. Finally with our investment looking a whole lot slimmer than when we commenced, I phoned the CEO and said ‘you are either incompetent or exceptionally unlucky, but in either case, we can no longer invest in your company!’

With Viva, whether it’s a question of competence or coincidence, only time will tell. But there is one key tenant we continue to arrive at: our assessment that – to date - the hits to earnings are cyclical not structural, and therefore in the fullness of time will revert.

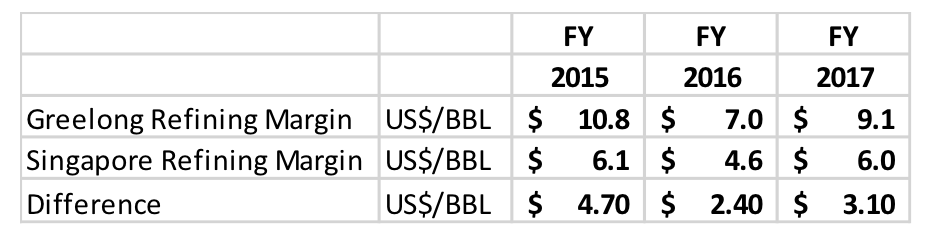

At the heart of this is, of course, Viva’s refining margin. Going into the investment, we were aware that this could be highly volatile and hence impact short-term earnings. The prospectus for example provided ample evidence of past volatility, indicating that over the preceding 3 years the average annual refining margin had been as lows as US$7/barrel and as high as US$10.8/barrel - a range of more than 50%. And individual months had been up to two times as volatile.

But this time around, part of the problem appears to be a breakdown in the gasoline cracking spread, which indicates the difference between the price of crude oil and the price of products made from the crude oil. In June and again October when the Singapore Reference Margin was already low, the narrowing of the cracking spread further exacerbated the fall in the Geelong Refining Margin.

The result was that underlying EBITDA for the Refining Division was wound back from a prospectus forecast of $216.7m to a revised figure of $150m – a substantial reduction. Yes, this was compounded by lower annual throughput, but the bulk can be explained by the (cyclical) refining margin.

To see this in context, we should note that the refining division earnt $276m in the 2017FY, $144m in the 2016FY and a very sizeable $326m in the 2015FY. So across these 3 years, the division contributed on average $249m – versus the revised number of $150m for this FY.

For this reason, we have chosen to hold our nerve and our position.

We are of the view that the refining margin will recover and drag earnings along with it. But we are not wedded to this view, and if signs emerge that there is a structural deterioration in any component of the Geelong Refinery Margin, then we will be required to re-think our position.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

.jpg)

1 stock mentioned

.jpg)

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

Expertise

Katana Asset Management was founded in September 2003 as a boutique investment management firm. Katana employs an all opportunity investment mandate being style, sector and market cap agnostic.

Expertise

Comments

Comments

Sign In or Join Free to comment