"It's quiet... too quiet" - why feeling comfortable is dangerous

It’s quiet out there. Since the so-called return of volatility at the beginning of the year, financial markets are seemingly benign once again. Perhaps it’s the warm summer in the northern hemisphere, but many investors now feel that investing in equities is less risky than it was just six months ago. Indeed, volatility, as measured by the VIX index, is once again subdued.

It is our firm belief that volatility is not a risk (we define risk as the chance of permanently losing some or all of the money you have invested). Unfortunately, most investors argue the opposite. Evidence of this argument can be found in the crusade to distil risk into a single, all-encompassing stand-alone statistic, such as ‘Value at Risk’ (VaR). This measure of risk is commonly used to estimate how much an investment may lose over a certain time period at a given level of probability. It does this by looking at the historical volatility. As a consequence, VaR shows unequivocally that the higher the volatility, the higher the risk of an investment.

A crude example can shed some light on why we feel such an interpretation is perverse. Imagine a stock falls rapidly from $10 to $2. Any risk measure based on historical returns volatility will show that the stock has instantly become ‘riskier’ at the new, lower price. Say the stock falls further to one cent, according to this interpretation of risk, the stock has become almost infinitely riskier.

While volatility can contain some information about the riskiness of an investment, this example shows that using price history as the sole proxy for assessing the risk of a living, breathing business is both reckless and ill-informed.

That’s because this approach encourages investors to forgo a forensic analysis of a company’s fundamentals in favour of comparing today’s price to yesterday's. Ultimately, risk is inextricably linked to valuation, and it can’t be boxed up into a one-size-fits-all arbitrary number. In Berkshire Hathaway’s 1993 shareholder letter, Warren Buffet argued much the same, referencing Justice Stewart’s 1964 famous test for obscenity. The US Supreme Court Judge argued he couldn’t formulate a test for obscenity, but merely concluded, “I know it when I see it.”

Risk, risk, everywhere

"There can be few fields of human endeavour in which history counts for so little as in the world of finance” - John Kenneth Galbraith

If risk can’t be found in VaR models, where might we find it?

Nine years into an equity bull market and there are signs that the confidence that this has instilled in investors is beginning to breed complacency in some areas. In the Schroder Value Team, we keep a folder of scary charts. Here are a couple to ponder:

Everywhere we look, we see signs of risky behaviour

You don't see this at market troughs

% IPOs with negative earnings

This shows the percentage of IPOs with negative earnings every year since 1980 – and, as you can see, far from historic lows, 2017 is instead tied for second place with 1999 and nearing the historic highs of 2000. Breaking down the 2017 number a little, the data shows 83% of technology company IPOs and no fewer than 97% of biotechnology IPOs had negative earnings.

And while those are the two sectors whose members you might expect to see in the loss-making camp, the data also reveals almost three-fifths (58%) of all other IPOs had earnings of less than zero last year – a record high. With the percentages nudging up towards those last seen in the run-up to the dotcom crash, the implication is that it is easier to IPO a loss-making business towards the end of a market cycle. It is definitely indicative of more risk-taking by investors.

Money is lost when conditions and outlook are good

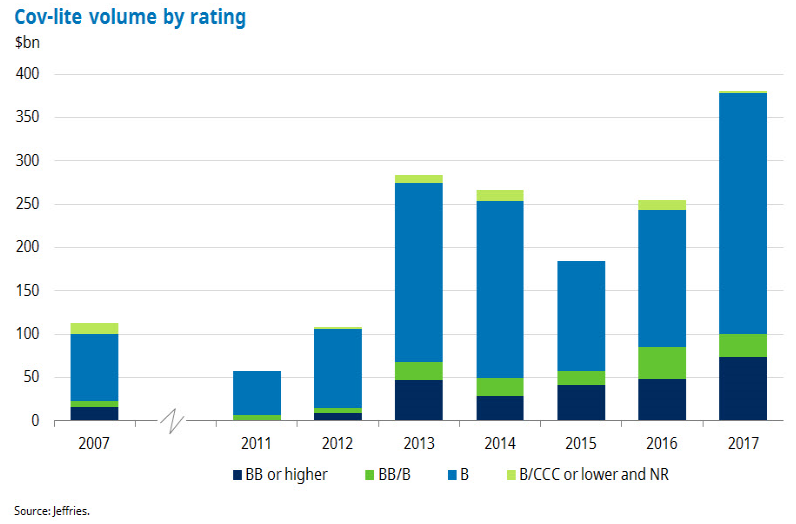

How easily the markets forget...

The chart above shows that ‘covenant-lite loan’ issuance has reached an all-time high. These loans, as the name just about suggests, impose less stringent terms on borrowers. For example, they may choose not to impose a limit on the total amount of debt a company can take on – which of course means they are much riskier for lenders.

What can we take from this anecdotal scariness?

At this time in the cycle, we really don’t want to buy businesses that are nearly cheap enough. It is in this sort of environment when what value investors refer to as ‘margin of safety’ (the difference between the market price of an investment and its true worth, and the cushion that investors have to compensate them for an investment’s risks) becomes harder to come by. When margin of safety is scarce both the upside we can expect from an investment and the insurance we have against its risks are low. Achieving a suitable balance between risk and reward is the foundation of successful long-term investing, and by consistently viewing the stockmarket in these terms investors are much less likely to be distracted by short-term exuberance.

These are dangerous times precisely because they feel so comfortable. Traditional principles such as patience, prudence and a focus on valuation and balance sheet metrics can start to appear outmoded and unexciting. The temptation to lower standards, or even abandon them in pursuit of the apparently immediate gains on offer can be strong. By the same token, the risk of overpaying for investments is also higher and, as valuations drive long-term investment returns, the seeds of future capital loss can very easily be sown.

This focus on the fundamentals rather than the froth may not be rewarded in the short-term, but in the long-run this is the surest way to safeguard capital and to ensure that full advantage can be taken when margin of safety, and hence investment opportunity, becomes abundant once again.

Further insights

You can access more analysis from the team at Schroders here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nick is co-head of the Global Value team and co-manager for the Schroder Global Recovery Fund. He seeks to identify and exploit deeply out of favour investment opportunities. Nick has a degree in Aeronautical Engineering and is a CFA charterholder.

Nick is co-head of the Global Value team and co-manager for the Schroder Global Recovery Fund. He seeks to identify and exploit deeply out of favour investment opportunities. Nick has a degree in Aeronautical Engineering and is a CFA charterholder.

Expertise

Nick is co-head of the Global Value team and co-manager for the Schroder Global Recovery Fund. He seeks to identify and exploit deeply out of favour investment opportunities. Nick has a degree in Aeronautical Engineering and is a CFA charterholder.

Expertise

Comments

Comments

Sign In or Join Free to comment