July Review: Asset Prices and Risk Levels Rising

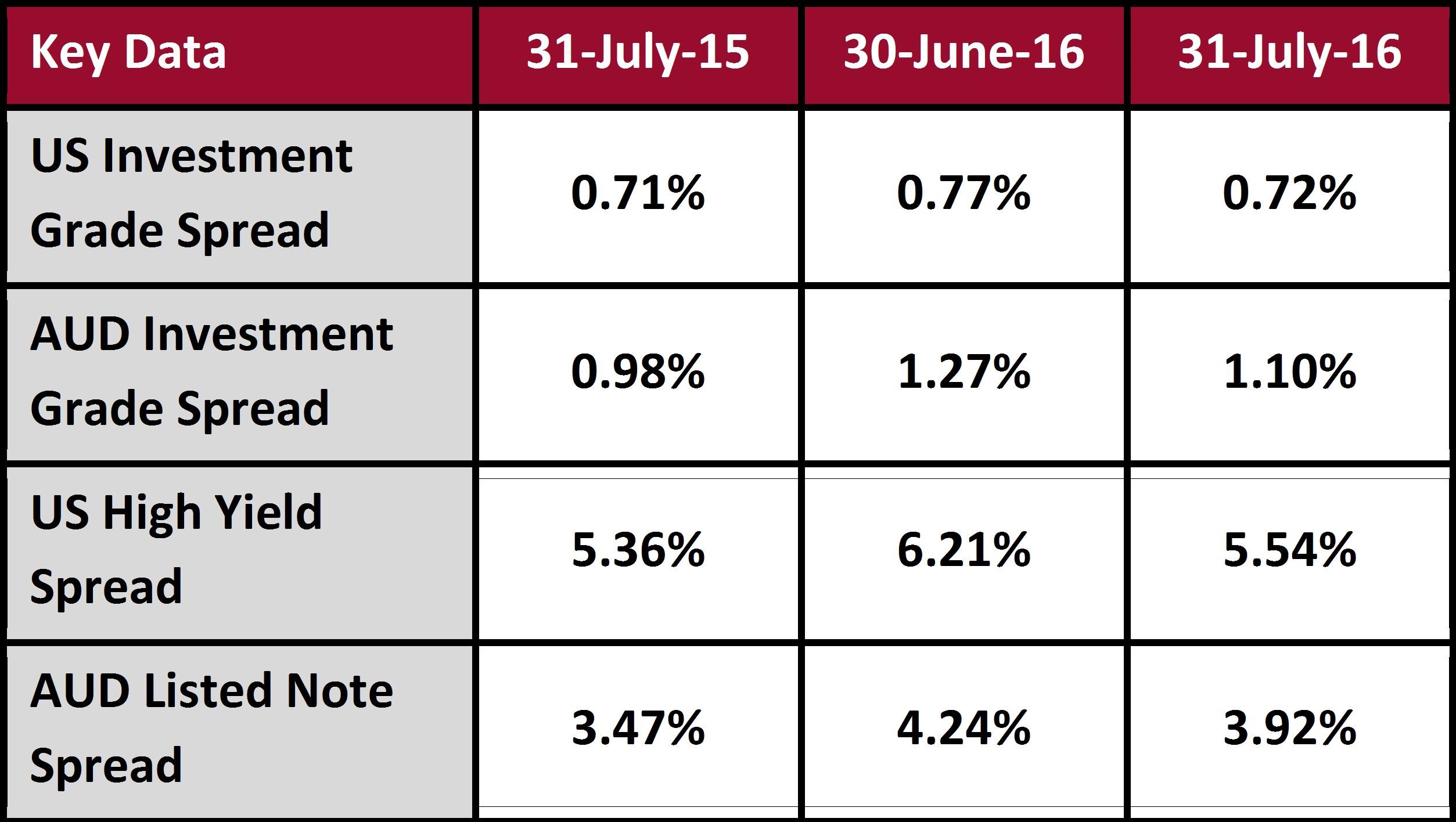

Almost all risk assets rose in July, with strong gains in equities and debt. US equities are back to record highs finishing the month up 3.6% with strong gains in Japan (6.4%), Australia (6.3%), Europe (4.4%) and China (1.6%). Investment grade and high yield recorded very strong gains in the US and Australia. Commodities were a mixed bag with US oil down 14.0% and iron ore up 6.7%. Gold (2.2%), Copper (0.7%) and US natural gas (-1.4%) had smaller moves.

The big question for the month was the dichotomy created by both risk assets and “safe haven” assets rising. When risk assets perform well that usually indicates a strong economy. When bond prices rise (yields fall) that usually indicates a weaker economic outlook and potentially a recession ahead. With both occurring at the same time which one is right? There’s a slew of different answers, but the simplest one is that negative interest rates and quantitative easing are the tide that lifts all boats.

Central banks buy government bonds with the aim of pushing down yields. When investors sell their bonds to a central bank they can either put the money in a bank or go and buy other assets. When cash rates are near zero or negative, cash rates look so bad some say that there is no alternative but to buy riskier assets. We can see this in US investment grade corporate bonds where corporates are struggling to issue enough to meet demand and the new issue premium has collapsed to almost nothing. In markets like this you start to see people arguing about relative overvaluations, for example junk bonds are overpriced but are not as bad as equities and are emerging markets a trap?

I use the term “safe haven” carefully now as supposedly safe assets are becoming crowded and aren’t necessarily safe anymore. The idea that interest rates could increase is almost heresy. The consensus view is that the world is awash with cash and interest rates are going to be lower for longer. Investors are responding by going all in on long bonds. The belief in lower for longer interest rates also underpins gains in equities, property and infrastructure investments in recent years. If the consensus is wrong asset prices could change quickly and dramatically. The reigning bond king Jeffrey Gundlach called it a “world of uber complacency” and recommended investors sell everything.

The three main concerns for US equities are the high P/E ratios, a poor outlook for earnings growth and the quality of earnings issue. The run up in indices this month was primarily P/E expansion as quarterly earnings are showing only 1% year on year growth. Bank of America has 14 out 20 indicators saying that equities are overpriced and energy P/E ratios are literally off the chart. The earnings quality issue continues to grow with 94% of S&P 500 companies now reporting two types of earnings.

Perhaps the only investment sector that fell hard during the month was UK property. At least nine unlisted property funds with total assets of more than £15 billion halted redemptions. There’s been a range of responses, some funds have slashed asset values and then re-opened, whilst one sold a property at a 15% discount to the book value. I wrote about these issues last month so I won’t repeat it all, but this is a warning as what can happen to illiquid assets in open ended funds. US high yield debt is probably the sector that has the biggest risk of this type.

In long term economic indicators there’s five ugly data points this month. Second quarter GDP for the US came in at a measly 1.2%, following on from 0.8% in the first quarter. US consumers are spending up, but businesses ran down bloated inventory levels and pulled back on investments. US restaurant sales are flat year on year, which could be a pre-recession indicator. McDonalds is hoping to grow by stealing market share from competitors, so that will pretty much guarantee margin compression on top of no revenue growth. The US Cass Freight index and global trade levels are both saying economies are stagnant. Lastly, online job ads in the US have plunged this year.

The decline of the oil price this month is troubling for many highly indebted companies and countries. Standard and Poor’s has seen 100 defaults in the first six months of 2016, which is on pace to beat the record number of defaults in 2009. Many of the defaults are from energy companies. Supply is increasing as Canada and Nigeria are coming back on line after recent disruptions. Demand growth is flat as global economic growth is sluggish. Oil and associated products in storage in the US, China, Europe and at sea are at record levels.

Banks

The Italian government is scrambling to put together two programs to support its banks. The banks need help as the pile of non-performing loans is bigger than the bank’s tangible equity and provisions set aside for losses. Following on from the Atlas fund another solvency program is being proposed. This one involves the government using €10 billion of taxpayer money to buy €50 billion of non-performing loans from the banks. A separate liquidity facility would provide up to €150 billion of senior debt if depositors and international lenders rush for the exits.

The most troublesome of the Italian Banks is Monte Dei Paschi. It was the only bank to outright fail the Europe bank “stress” test, which is so weak it should be called a tickle test. A bailout is obviously required and is being patched together. Part one involves dumping €50 billion of non-performing loans onto the Atlas bailout fund. Atlas is expected to receive another €15 billion in order to be able to swallow those loans. Part two is a €5 billion capital raising to be underwritten by eight banks. On face value the numbers for all of this don’t work and a lot more capital will be needed. It’s also not clear who be willing to throw good money after bad in the Atlas fund or Monte Dei Paschi, a taxpayer funded bailout seems the most likely option. An updated business plan is due to be released in September.

European rules require shareholders and subordinated debtors to be wiped out before taxpayer funds are used. Italy is desperate to avoid a by the rules bailout of their banks as retail investors own around half of bank subordinated debt and this was sold to them as an alternative to retail deposits. Italian pension funds are being asked to help bail out the banks. If there is a meltdown in Italian banks the French and to lesser extent the German banks are most exposed. Christine Lagarde has reassured investors that Italy is not Greece. She’s right, Italy is much larger than Greece and is too big to fail and too big to bail.

The problems aren’t limited to Italy with a report by a Deutsche Bank economist having Spain, Portugal and other European nations needing to recapitalise their banks to the tune of €150 billion. I’m not sure how much the author has pencilled in for the German government to provide to his employer. The comparisons between Deutsche Bank and Lehman Brothers continue. Deutsche Bank isn’t the only German bank attracting concern, Commerzbank’s capital ratios are falling but it is still paying dividends. Bremen Landesbank might need a taxpayer bailout.

Regulators

In news about regulators there’s highlights and lowlights this month. The highlight is the Singaporean bank regulator continuing its crackdown on dodgy dealings from the 1MDB scandal. After dealing out the ultimate punishment to one bank, cancelling its licence to operate, Singapore is now seizing assets and heading down the pathway of handing out fines to lessor offenders. Also smart is the New Zealand central bank increasing the deposits required for home loans in order to take the heat out of property prices.

On the what are they thinking end of the spectrum US insurance regulators are considering reducing the amount of capital that needs to be held against sub-investment grade debt. Their timing couldn’t be worse as defaults are increasing and the experts are saying that the asset class is in the extreme overvaluation zone. Insurance companies make around half of their profits from investing, which is predominantly in investment grade debt. The right response to their complaints about falling profits from lower yields is for central banks to return interest rates to normal levels, not for regulators to “help” them by letting them invest in riskier assets. Another dumb regulatory move was Britain reducing the counter-cyclical buffer on banks from 0.5% to 0%. With the uncertainty of Brexit, high growth in consumer debt and property funds locking up as property prices fall now is the time to increase the counter cyclical buffer.

After much talk of “the tough cop on the beat” prior to the election, Australia’s watchpuppy securities regulator ASIC has returned to form. ASIC is doing a decent job of cracking down on small and medium sized financial firms that are engaged in misconduct as well some higher profile insider trading cases. However, when it comes to the big end of town it really is a paradise for corporate crime with only the media to worry about. This month IOOF escaped without a penalty over a laundry list of misconduct including insider trading and sacking a whistleblower who tried to get the issues dealt with. Perhaps ASIC could get a few Singaporean peers to come over on secondment in order the lift the culture at the Australian regulator. Similar to ASIC’s failings, a US government report found that the US Justice Department had a too big to jail policy when it came to misconduct committed by large banks.

Monetary and Fiscal Policy

The practicalities of helicopter money are now being openly discussed with the OECD’s chief economist suggesting that you can’t just put money into bank accounts and expect people to spend it. The alternative is to give people retail vouchers. It’s nice in theory but if that occurs get ready for a black market in retail vouchers, perhaps trading at a 5% discount to face value. Whilst some would spend the voucher on frivolous things, as was reported with Australia’s cash splash in 2009, in the current income strapped environment I suspect many will spend a voucher on essentials like groceries, utilities and fuel for their car. Many take it as a given that helicopter money will stimulate growth, but others claim that the 2008 version in the US was a failure.

The Bank of Japan announced that it would increasing its buying of equities by another ¥3 trillion per annum, in what was considered by many to be a major let down. The Bank of Japan Governor said there is “no need and no possibility for helicopter money” but he gave similar assurances about not using negative interest rates right before he announced negative interest rates. This is an argument of semantics though, the central bank creates money to buy government bonds, which supports the government in running massive budget deficits for fiscal stimulus.

The latest fiscal stimulus package from the Japanese government is equivalent to 6% of GDP. The only difference between this and helicopter money is that the government decides where the money is spent rather than the individuals that receive the cash from helicopter drops. Either scenario sets a country on the pathway to hyperinflation, it is just a matter of time before money leaves to go somewhere that isn’t printing money. One indicator of the problems with existing policies is Japanese banks making 50 year loans for commercial property in a desperate attempt to get some yield from lending.

Perverse outcomes from terrible monetary and fiscal policies aren’t limited to Japan. In Europe negative yields are spilling over into corporate bonds. The ECB has spent €10 billion buying the debt of 43 issuers, including debt issued by Glencore and two sub-investment grade rated companies. The ECB’s buying of government debt is running at three times the pace of governments issuing debt. Essentially the ECB is fast running out of lower risk assets to buy, so there’s speculation that it will start buying equities and/or high yield debt soon. If they do start purchasing equities, they can point to Japan and Switzerland as others already doing it. Deutsche Bank’s economists continue to criticise negative interest rate policies calling them “poison” and noting that they are “doing serious damage”.

China

One article this month pretty much summed up the overbuilding issue in China. In aggregate, Chinese cities are planning for 3.4 billion people in 2030. That’s three times the existing population and forecast population growth is minimal. Peak urbanisation may have arrived for China, the substantial slowdown in wage inflation is a strong indicator that the demand for labour is flat at best. This aligns with recent reports of a substantial increase in the unemployment rate. The city of Tieling is one example of what happens when a construction and manufacturing bubble pops.

Remember that local governments earn most of their revenues from property development activities, which would fall flat if urbanisation stops. A collapse in revenue would make debt servicing problematic, which is particularly concerning as local governments have seen an enormous increase in their debt issuance in 2015 and 2016. This includes continuing to build coal fired power plants when the existing plants are running at low capacity. Local governments are blocking lenders from withdrawing credit in order to protect jobs at zombie companies. 7.5% of companies in China are believed to be economically unviable, with medium and large state owned entities the worst.

Last month I wrote about the first non-performing loan securitisations in China and it looks like this process is ramping up. The Agricultural Bank of China is planning to sell a US$1.6b securitisation of non-performing loans which includes the underlying loans being marked down to 29% of face value. The other big way that banks are planning to clean up their loan books is debt to equity swaps, which are expected to start soon.

There’s plenty to worry about with peer to peer lending and a crackdown is coming for wealth management products. In order to reduce fraud in these areas executives are being given tours of prisons, as a reminder of what might happen to them when investors lose money. Given the concerns with these sectors, investors are increasingly investing overseas or putting their savings in a bank. In a reminder that Chinese investors are still learning the ropes, one article highlighted their love affair with stock splits and stock dividends. If a company is issuing more stock they assume it must be good.

The Chinese regulators are planning to reduce the maximum leverage within managed funds from 70% to 50%. In what might be a sign that the Minsky moment is near, corporate bonds sales are falling as default rates are increasing. Perhaps investors are starting to realise that Chinese ratings agencies can’t be trusted with 56% of AAA rated bonds having sub-investment grade metrics. Chinese asset management firms will have to continue raising capital in order to deal with the expected wave of defaults. Bankruptcy and recovery processes are still problematic with Dongbei Steel going about its business as if nothing has happened three months after it skipped debt repayments.

I suspect iron prices can’t remain at current levels for too much longer as Chinese stocks piles are soaring once again. Chinese iron ore producers are claiming that Australia and Brazil are dumping iron ore into China, the clearest indication yet that they are suffering. The higher prices for iron ore are driven by credit growth that remains strong and investment by state owned entities that has skyrocketed this year, neither of which can last forever. Chinese state owned entities are being loyal to their masters, helping to prop up both the yuan and share prices.

Emerging Markets

Venezuela keeps getting worse as gold reserves are still being sold off to postpone an inevitable default. Big repayments are due in October and November and that’s when a default might occur. McDonalds and Kimberly Clark are the latest businesses to halt production after being unable to obtain key supplies.

Mozambique is set to default soon, with the story of how it fell from Africa’s most promising economy to its current situation an interesting one. Puerto Rico paid $1.1 billion and defaulted on $977 million of repayments in early July.

The Puerto Rican water utility wants to raise $900m in new debt and give existing debtors a 15% haircut. The President of Angola has warned that his country will struggle to pay its debts. Argentina hasn’t defaulted, but with inflation running at 50% per annum and with interest rates at 30% the average citizen might think it has.

Turkey, Russia, China and Brazil all have issues with private sector debt levels. Turkey’s political issues are well known, creating a risk for its banks who rely heavily on external funding. Russia is raiding its sovereign wealth fund to maintain government spending, retail sales are down 5.9% and about 10% of loans at banks are thought to be non-performing. But don’t worry about any of that, emerging market debt is all the rage. Investment refugees from negative interest rate countries need somewhere to put their money. The P/E ratio for emerging market equities is well above long term averages. India’s high yield bonds are also currently sought after. That seems a little odd given its banks are dealing with a mountain of non-performing loans and credit rating downgrades. Indian state banks are set for a $3.4 billion taxpayer recapitalisation but some are saying it won’t be enough.

Politics

Republicans and Democrats both have reintroducing Glass Steagall limitations for bank on their policy platforms. Cynics have suggested that this is just a ploy to get donations from the big banks and then do nothing after the election. Here’s a documentary that makes the case for why Trump can keep calling Clinton crooked. Expect to see more articles like this one – Clinton versus Trump – who’s worse? The US Green party offered Bernie Sanders their leadership role if he was willing to switch allegiances.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

4 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment