TOL - 21st Jan, 2021

Just how big will the iron ore miners’ dividends be?

Reporting season in Australia kicks off very shortly and this (as always) will be important to the market’s future fortunes. One theme that seems very obvious is that miners will pay big dividends, particularly the large caps that are exposed to the freight train which has been Iron Ore. The bulk commodity was trading at $US110 6 months ago, $US94 6 months before that and today sits around $US170/tonne.

Iron Ore Chart

The 3 largest local Iron Ore miners, RIO, Fortescue & BHP have an average cost of production below $US14, FMG the lowest at $US12.94 and RIO highest at $US14.50, so clearly, they are printing considerable amounts of cash at current prices.

- FMG generates 100% of its earnings from Iron Ore.

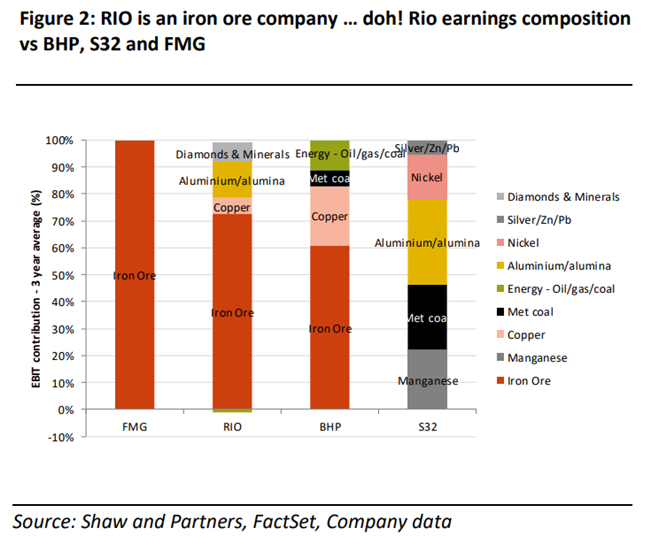

- RIO generates around 70% of its earnings from Iron Ore

- BHP generates around 60% of its earnings from Iron Ore

The chart below from Peter O’Connor at Shaw looks at this composition as an average over 3 years and includes S32 for good measure, which we own in the MM Growth Portfolio but is not that relevant here!

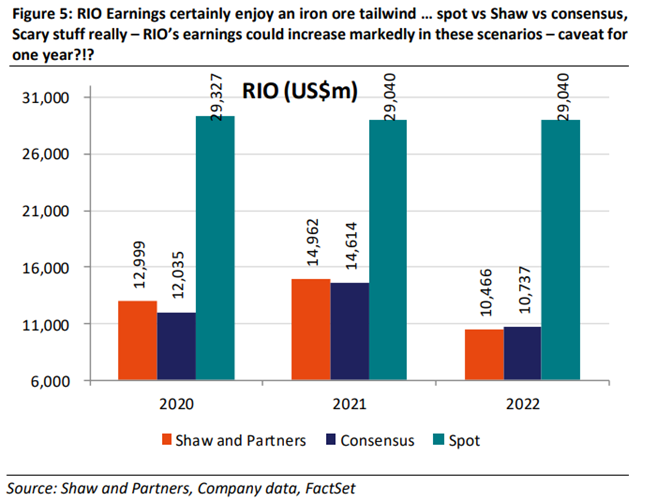

Focussing on RIO for a moment given they reported production numbers yesterday, and again drawing on Rocky’s research, the table below looks at RIO’s earnings using Shaw forecasts (Orange), Consensus forecasts (Blue) and current spot prices (Green). Clearly, the market is not expecting spot prices to be maintained which is the likely scenario, but then again, no analyst that I can see expected Iron Ore to be where it is now.

MM believes we should remain very open-minded with our expectations around Iron Ore this year.

In the MM Income Portfolio, we currently hold BHP & RIO which have been star performers.

BHP kicks off reporting on the 16th February, FMG on the 18th & RIO on the 26th. Dividends here will be watched very closely.

Consensus dividend expectations are as follows:

BHP: US55c fully franked for the half with another US68c in August. That puts BHP on a forecast dividend yield of 3.80% plus franking, or 5.42% grossed.

FMG: 80c fully franked for the half with another $1.05 in August. That puts FMG on a forecast dividend yield of 7.45% plus franking, or 10.64% grossed.

RIO: $3.52 fully franked for the half with another $2.23 in August. That puts RIO on a forecast dividend yield of 4.81% plus franking, or 6.8% grossed.

BHP’s dividend is lower; however, they are investing more heavily in future Iron Ore production. Looking out to FY21, both RIO & FMG’s production will likely be flat YoY while BHP’s production will likely be higher.

MM remains bullish the Iron Ore producer’s medium term.

Rio Tinto (RIO) Chart

Looking further out is always less certain and it’s important to recognise that commodity stocks should never be held solely for income. MM’s view on underlying commodity prices will dictate whether or not we hold resource stocks this year, and for now we remain bullish inflation expectations and global growth, and commodities benefit in this environment. That, however, won’t last forever. Just as the best medicine for low commodity prices is low commodity prices themselves (production gets shelved) ultimately high commodity prices incentivise new production which creates the cyclical nature of resource earnings. For now, however, we think we’re in a rare window where commodity prices will remain firm.

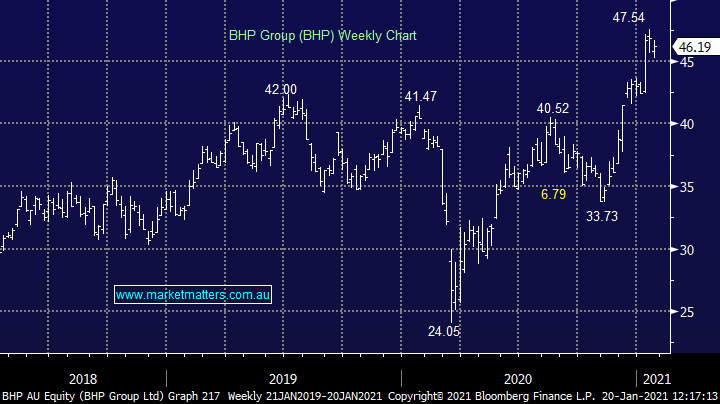

This morning BHP released production numbers that were down quarter on quarter, and in many cases, year on year. The headlines were weak however this was well flagged when they updated the market in September. There were multiple reasons for the weak quarter, however importantly, BHP reconfirmed full-year production targets across the board plus marginally increased their targets for Petroleum.

MM remains bullish BHP.

BHP Billiton (BHP) Chart

Conclusion

We remain bullish resources medium term.

Make informed investment decisions

At Market Matters, we write a straight-talking, concise, twice daily note about our experiences, the stocks we like, the stocks we don’t, the themes that you should be across and the risks as we see them. Click here for your free trial.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

4 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management