Learnings from a crisis (to date)

2020 to date has been a series of local and global events which have tested process, conviction, and stamina of every small and emerging company investor. It is only the end of May and investors have had to assess the impact of fires, floods, pandemics, and prolific monetary and fiscal stimulus to offset the worst economic data in recent memory, on their portfolio. One can be forgiven for having headline fatigue after the simple narrative of all-time market highs dominating 2019. So where to now?

With S&P 500 2021 EPS estimates as wide as my arm, strategists the world over are divided as to the duration of the virus, the letter of choice to characterise the shape of the economy and the pace of the recovery.

Rather than pontificate on the potential outcomes, we reflect on our 4 key learnings from the past 5 months to better position for opportunities that present themselves in the months ahead.

Sometimes you cannot see the wood for the trees

The past 5 months have been some of the most volatile markets in recent memory. Uncertainty continues to persist as markets grapple with pricing small companies with no revenue or significantly reduced earning profiles as a result of the coronavirus and the associated economic shutdown.

What is most interesting is how global markets seemingly ignored the warning signs for the first 7 weeks of the year. Monday 13 January marked the return to work for many Australians after their obligatory annual holiday break. The Australian newspaper that morning touted a headline ‘PM signals climate shift, deeper cuts’ after months of bushfires.

Close to 46 million acres of bush had been burnt or in some cases were still burning and the policy debate between climate scientists, environmentalists, deniers, and politicians was once again back on the front page. Masks in Sydney’s CBD were not an uncommon sight in January, as lunchtime runs, and commuting became a potential health hazard.

Source: The Australian, 13 January 2020

International news was not ignored completely that morning, a small by-line ‘Taiwan victory a headache for Xi’ made the front page after the Democratic Progressive Party took office in a landslide in elections over the weekend. The fact that China had announced its first death a day earlier from a strange virus that the World Health Organisation had likened to SARS the previous week, was ominously missing from the front pages.

A week later the fallout from the bushfires continued. Consumption had taken a hit. Retailers like Super Retail & Noni B said sales were paralysed in January, as Australian’s stayed at home to avoid the smoke and the heat. The same day, China reported a 3rd death, more than 200 infections, and Thailand its first case from this mysterious virus, and this news again was seemingly absent. The Small Ordinaries Index continued its march north ahead of the Australia Day Weekend (+5.4% MTD) tracking the US market gains, but something wasn’t right in China - the Shanghai Composite lurching 400 points lower in the 3 days leading into the Lunar New Year Holiday.

The Recency Effect

Hermann Ebbinghaus was a German psychologist who introduced the experimental study of memory. He is credited with discovering the ‘serial position effect’ whereby the ability to accurately recall items from a list was dependent upon the location of the item on that list.

Items found at the end of the list that are learned most recently are recalled best (the recency effect). Much has been written as to the effect of recency bias and its effect on investor behaviour. Typically, it's most pronounced during periods of uncertainty and volatility when we are faced with making decisions without the appropriate time to process information. But it can also be a dangerous phenomenon when all appears calm.

The Chicago Board of Exchange Volatilty Index (the VIX) is a real-time market index that represents the market's expectation of 30-day forward-looking volatility. It is compiled from price inputs of the S&P 500 index options and typically is used to measure risk appetite and investor sentiment. In late January, the VIX fluctuated in the mid teen’s very close to its 5-year trend, despite the WHO declaring the coronavirus a global emergency, 7711 cases of the virus were confirmed in China and 170 deaths were recorded.

Source: Bloomberg

The benefit of hindsight is a wonderful thing

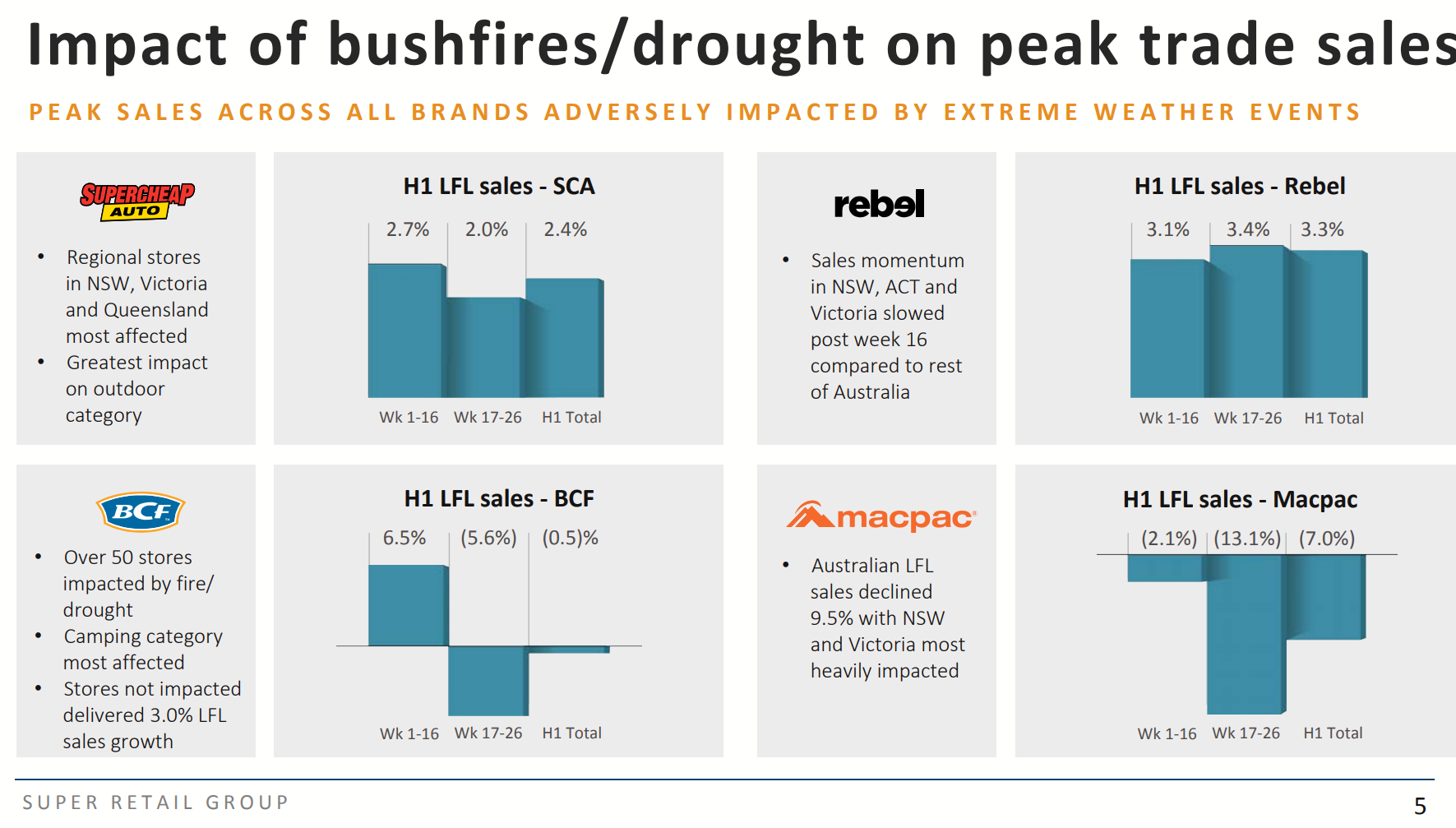

Australians were rightly focused on their immediate frame of reference after a traumatic summer that had seen lives and livelihoods destroyed by fire. Global markets continued to make new highs and the narrative at the time was this virus is a China phenomenon. January trading updates had no mention of potential supply chain disruptions from our biggest trading partner, it was all about a lack of demand locally as consumers sat on their hands. Investors braced for a reporting season dominated by commentary highlighting disruption from the fires and investing in fossil fuels was once again a contentious issue for the fund management community.

Source: Super Retail Group, 1H20 Investor Presentation

As February rolled around, the obligatory coronavirus impact slide was hastily included in investor packs. For brands such as Nick Scali, one of the first to report half-yearly earnings, the supply chain impacts at that stage were not significant, with an extension to Chinese New Year Holidays likely to delay order fulfilment by 1 to 2 weeks. While the question as to whether a global pandemic could spread to Australia in earnest and impact confidence did arise on the earnings call, on my count it was Question 26 before a journalist from The Age sought to clarify management’s comments as to a potential impact. Not surprisingly, the market’s attention at the time was firmly on the recent impact from the bushfires and how Nick Scali stores had traded through the key January trading period.

The above point is not meant to criticize but purely illustrate an example of how easy it is to lose sight of the big picture in small cap investing. Granted Australian cases were in the low double digits, however by Feb 9, 3 days post the NCK result, the death toll in China surpassed that of the 2002-03 SARS epidemic, with 811 deaths recorded and 37,198 infections. At the same time, the Small Ordinaries was within 3% and 10 days of its eventual high this cycle.

It is hard to fight the tape

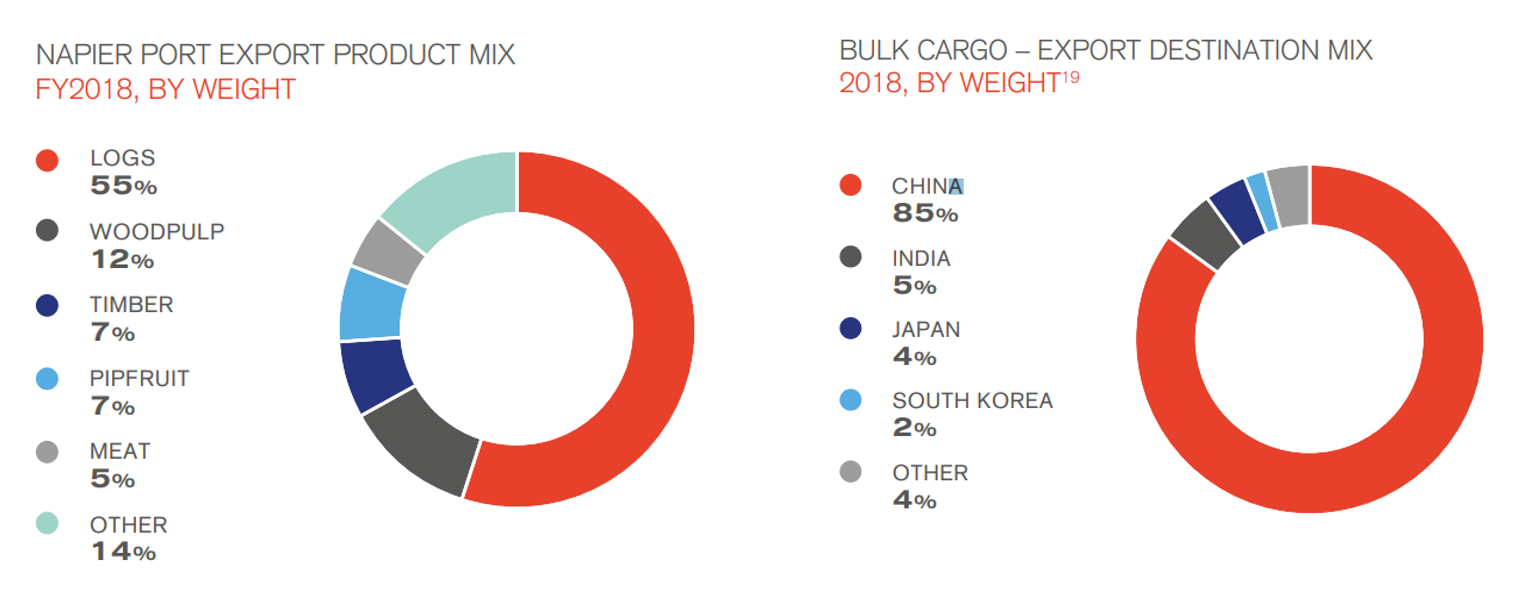

As the days rolled on, the warning signs that things were not ok in China began to flash amber. Some of our 2019 portfolio winners had significant China exposure. Napier Port Holdings – a large East Coast New Zealand Port IPO’d in mid-2019, with a sell down from the local council repaying debt and accessing capital for a wharf expansion. With logs to China its key export activity, and a nationwide lockdown looming, reducing exposure to this name was a priority.

Source: Napier Port Holdings Product Disclosure Statement

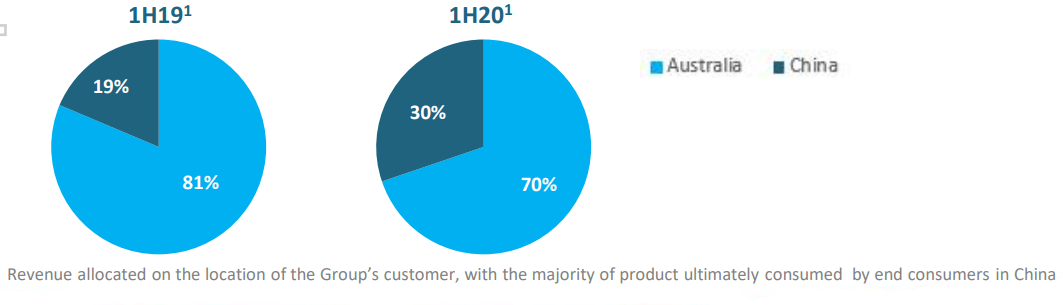

Likewise, goat based infant formula IPO Nuchev was one of the better performing deals of 2019, relied almost solely on Chinese consumption and trade. With the market largely ignoring the risk of potential disruption to global supply chains, making the decision to remove risks from the portfolio at that stage was difficult, and arguably cost some short-term alpha, as the Australian market powered to this cycle’s highs in mid-February.

Source: Nuchev Limited, 1H20 Investor Presentation

Making the call to sell your winners because you are presented with information that has fundamentally changed your investment thesis, should be a relatively easy decision. But every day that the stock contributes performance to your portfolio, and the market seemingly discounts your concerns, can make appropriate risk management seem like a grind. As a manager of money in an asset class that is further up the risk tolerance curve for many investors, making prudent decisions to protect capital, will undoubtedly be rewarded over the long term.

Taking time to research new ideas

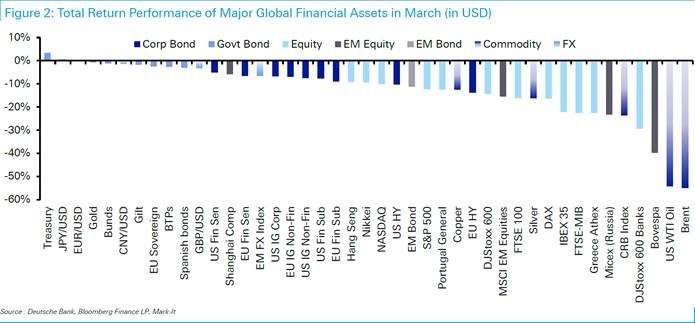

From February 20 to March 23, the S&P 500 recorded the fastest bear market in history. Panic was evident across markets as the world began to appreciate the significance of a global pandemic and the potential economic implications that come with it. As PM Scott Morrison began to grace our TV screens every evening with another alarming statistic and removal of a societal practice as we know it, the following morning the ASX newswires team were busy managing the race to withdraw guidance issued (at last count 157), in some cases less than 4 weeks before. Reflecting on that time some months later in an environment where peak volatility has somewhat subsided, the virus is still very much alive and well, and the true economic impact is yet to reveal itself, the approach to those 4 weeks can be characterised as defence.

Source: Deutsche Bank

Small and emerging company portfolios are typically constructed over time, with core holdings occupying the pointy end that align with a long-term investment thesis. Management teams are backed to generate superior returns on equity capital and take advantage of structural growth opportunities. Our process focuses on a qualitative and quantitative assessment that ultimately generates an abundance of ideas. Having to pandemic test your portfolio daily is something that we hadn’t foreseen but became the norm during the early days of the virus where an information vacuum emerged.

Many CEOs are on record as saying, “Don’t waste a good crisis”. The same can be said for investors, as valuations have been reset, structural trends have accelerated (i.e the adoption rate of online shopping) and new winners have emerged. Despite the stunning rally from the low, it is our view investors should balance caution with nimbleness and stay open-minded to the economic outlook.

For students of technical analysis, it is no coincidence that the ASX200 and XSO retraced rapidly to an area of significant support. In fact, an aged support line emanating from the 1993 lows captured price action spectacularly, as it had done back in March 2009. Essentially this signalled the low was, in all probability, in place for the local bourse.

Source: Laurence Balanco, CLSA

With so much yet to play out in the months ahead, as pharma companies race for vaccines, governments grasp with the withdrawal of fiscal support, and trade tensions once again re-emerging, it is almost certain volatility will return to markets. However, in this period of ‘relative’ calm, fundamental research can once again resume focus. While embarking on understanding the latest software-defined network, or the inner machinations of a carbon fibre wheel can seem daunting, research can be very rewarding.

Kicking the tyres

In the small end of the market, investors are spoilt for choice with hundreds of potential companies not blessed with significant sell-side analyst research coverage. Much of the insights are garnered from trawling through past investor presentations, store visits and calls with offshore peers or competitors.

Without wanting to oversimplify the process, a grasp on the past, the present and the future is the default framework we look to before beginning any research project.

The past is often the easy bit. Company secretaries spend weeks and months on an annual report of 100+ pages that can answer - The Five W’s (What, When, Who, Where, Why) & one ‘H’ (How) questions about any business. Director reports are a good starting point for understanding the fundamentals, but a lot of the value can be found in the notes to the accounts. A rationale for an acquisition, a capitalization policy (that potentially could inflate earnings) or an insight from the Chair as to whether he or she is singing from the same hymn book as the management are some of the important insights that a publicly available annual report can share.

The present is all about interpreting new information. Between 8am & 10am most days the ASX newswires light up like a council Christmas tree, as companies of all shapes and sizes rush to get out their story of the day ahead of market open. Concurrently daily newspapers and blogs provide profiles into how local businesses are pursuing growth initiatives, restructures, or potential acquisitions, while offshore peers can shed light on the global effects on any one industry. There is no shortage of information at hand, the challenge for investors is the filter process.

Finding the next Megaport, Afterpay or A2 Milk, early on in its journey is not an easy task, but taking the time to research structural growth trends, understand the potential winners and losers and the emerging companies that are set to benefit can be very rewarding. The concept of non-bovine milk supply was foreign to most mothers in 2016, but in 2020 is one of the fastest-growing categories in infant formula.

Likewise, sales enablement was an unfamiliar term to most boardrooms 4 years ago, which is strange given sales have been around almost as long as the human race, but a recent survey found 61% of organisations have a sales enablement function, and are looking at technologies to support them.

Never assume anything?

A wise investor once shared with me that a financial model is only as good as the assumptions that go into it. Insights gained from the past and present can be used to attempt to predict the future and ultimately to form the basis of the assumptions about potential growth rates, cost inflation, Capex profiles and a path to profitability. The past 5 months have challenged investor’s assumptions in every single way as the pace of change and the ramifications from a global pandemic, have made even the most basic assumption questionable.

Isaac Asimov, a famous scientist and science fiction writer, once wrote - ‘Your assumptions are your windows on the world. Scrub them off every once in a while, or the light won't come in’.

There is nothing like a global pandemic to insight a cleaning frenzy and give a new perspective to all assumptions.

The definition of defensive has changed

In the early days of March and the ensuing correction, many of the rules of investing were challenged. One could say the coronavirus forced investors to continually re-evaluate what businesses were deemed safe, essential, defensive or were in a relatively better position than other stocks in the market.

Traditional ‘safety trades’ such as utilities, REITs and infrastructure were no longer immune from a pandemic induced market correction. At the conclusion of the February reporting season, there were no questions from analysts to property owners as to whether the coronavirus was likely to result in mass rent deferrals or whether New Zealand’s electricity demand was likely to see double-digit declines as a result of a lockdown. Infrastructure assets such as Auckland Airport with a defensive earnings stream, were suddenly staring down the likelihood of less than 5% of air traffic in the coming months. Assumptions in a pre-virus world were no longer appropriate for these markets.

As the pandemic took hold and markets reacted violently, the assumptions made at the beginning of March, were no longer valid some 2-3 weeks later. When indiscriminate selling took hold and liquidity was king, fundamental ‘safety trades’ were not immune. As the gold price fell 12.5% from peak to trough in March, the stocks followed suit. The inflation hedge was questioned post the emergency rate cuts but was back in vogue post the Fed committing to unlimited QE & corporate bond buying.

At the stock level, assumptions were even harder to make. If you lockdown a society for an indefinite period, what does that do to consumption, Capex and cost bases? For some businesses, it was clear cut. There would be zero revenue because of an enforced government shutdown. The question then turned to ‘for how long?’ Kathmandu signalled July as part of their capital raising for the re-opening of stores, while Event flagged closure of their cinemas till at least the end of May and are yet to provide a further update.

Complicating matters was massive fiscal stimulus measures announced almost daily which saw some employers receive compensation for keeping employees on the books and industry-specific assistance was handed out to those in need. For those in the travel industry assumptions had to be made as to the duration of border closures, while emergency capital raisings were based upon a depressed revenue and earnings picture for the best part of 12-18 months.

As we close out May the number of ASX announcements that mention re-opening in the headline, outweigh the balance of negative news-flow at the beginning of every day. Undoubtedly the assumptions made by many during the midst of the pandemic will prove incorrect. Some in the case of retail may be too conservative. While the impact on earnings across emerging companies will only become apparent as the final touches on FY20 earnings are put together come July.

Test, Test & Retest

Once again investors will be forced to retest their assumptions and start focusing on how companies can regain lost earnings, and the time it will take to recover to FY19 levels. How the market values these fundamental earning streams will also normalise in time when the uncertainty subsides.

For now, the time is best spent validating your current assumptions regularly and being open-minded to what lays ahead.

Access Australia's most compelling small and emerging companies

Eley Griffiths Group is a specialist at focusing on small and emerging companies in Australia. Our investment process and team have delivered consistent out performance through all market conditions for 16 years. Visit our website to find out how.

Hit the 'follow' button below to receive future articles about investing in small and emerging companies on he ASX.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nick joined Eley Griffiths in September 2016 after 6 years at the global equity research house CLSA, in both analytical and research sales roles in the US & Australia. Prior to financial markets Nick spent 4 years as a practicing lawyer.

Featuring

Nick Guidera,

Eley Griffiths Group

Nick joined Eley Griffiths in September 2016 after 6 years at the global equity research house CLSA, in both analytical and research sales roles in the US & Australia. Prior to financial markets Nick spent 4 years as a practicing lawyer.

6 stocks mentioned

Nick joined Eley Griffiths in September 2016 after 6 years at the global equity research house CLSA, in both analytical and research sales roles in the US & Australia. Prior to financial markets Nick spent 4 years as a practicing lawyer.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets