TOL - 11th Jan, 2021

Levered housing equity to generate large returns in 2021...

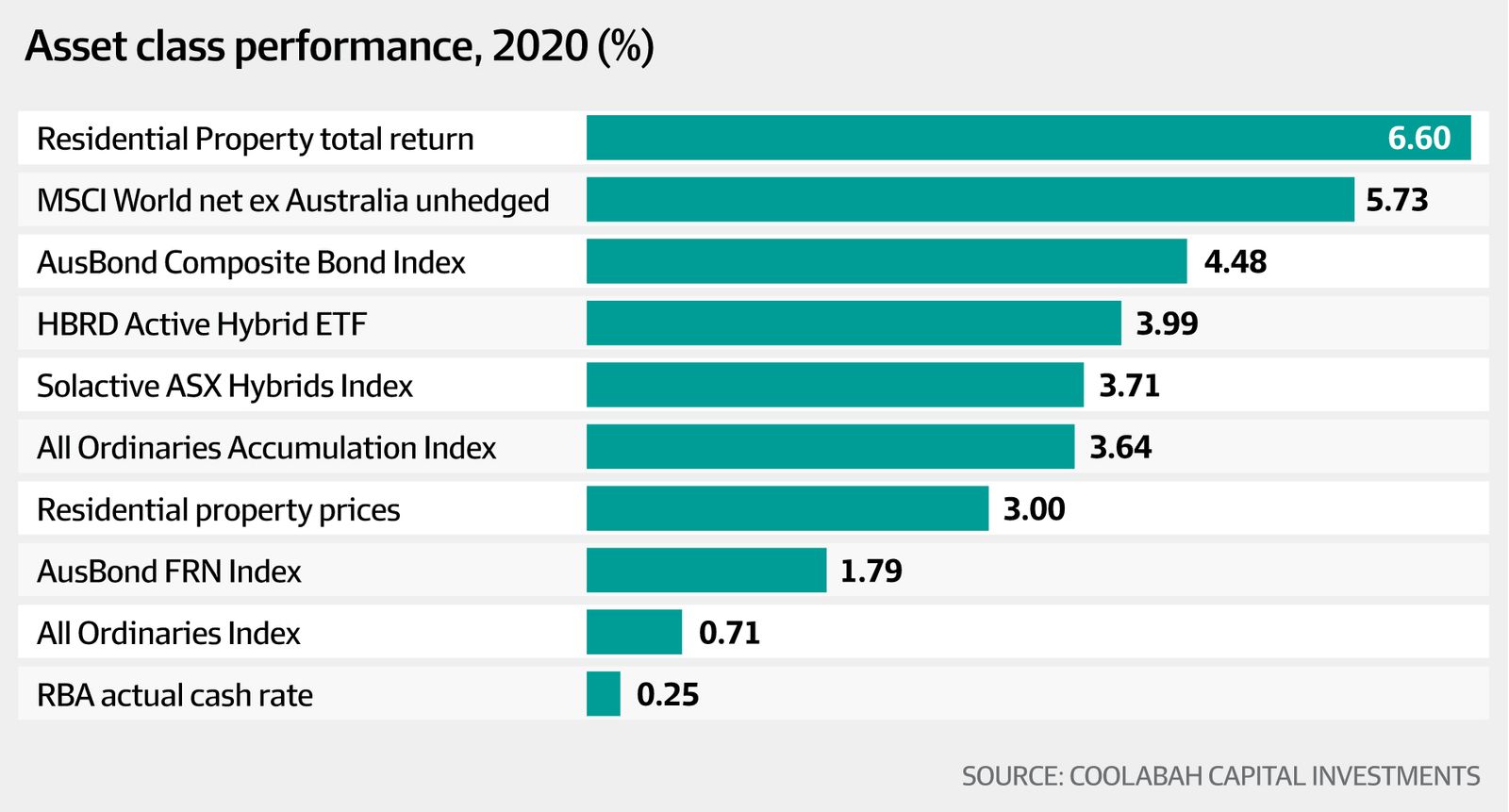

Setting side Bitcoin, what was the best performing asset-class for Aussie investors in 2020? In the AFR today I write that as it turned out, residential real estate trumped the alternatives (excuse the pun). Excerpt only:

Across all metro and non-metro (regional) markets, Aussie home values appreciated 3.0 per cent in 2020. If you then add-in the national gross rental yield, you get an impressive total return of 6.60 per cent for the year.

This was presumably a huge surprise to all the analysts, economists and fund managers who predicted that house prices would fall 10 per cent, 15 per cent, 20 per cent or even 30 per cent. The good news for property punters is that the returns will be even better in 2021—in fact, more than double the 2020 results.

Back in April 2020, a billionaire, whom I call “the Rabbi”, assembled his top fund managers globally for a virtual round-table on their best investment ideas. My offering was very simple: you are going to get more than a 100 per cent return on your equity in 10 times levered, well-located Aussie housing. That forecast is playing out and should be comfortably realised within 12 months.

Interestingly, the next best performing asset-class was unhedged global equities on a net total return basis (ex Australia), which delivered a decent 5.7 per cent payoff. This was followed by Aussie fixed-rate bonds (4.5 per cent), ASX floating-rate hybrids (4.0 per cent), and Aussie equities (3.6 per cent).

Notwithstanding the extreme turbulence in 2020, it was therefore possible to capture decent returns. But you had to be incredibly active—and this in turn requires one to focus on liquid assets that are tradeable in all market conditions. In our own portfolios, we bought and sold more than $25 billion of bonds in 2020, which was split between about $15 billion of trades in (primarily) liquid bank and, more rarely, corporate bonds, combined with another $10 billion of transactions in government securities. Even in the extremely stressed month of March, where liquidity was the thinnest it has ever been on some days, we still traded about $1 billion in bank paper.

While 2021 is bound to be bumpy, there are grounds to believe the global economy can embark on a robust recovery. Highly effective vaccines are now being rolled out, which should assist in normalising activity. A much more predictable US president is in power with the ability to rapidly execute plans given the Democrats now control both the house and the senate, which is positive for growth in the world’s largest economy and global geo-political stability.

The challenge for investors is finding attractive returns without assuming excessive liquidity risk, credit default risk, and/or interest rate risk.

At the start of 2020, the RBA’s target cash rate was 0.75 per cent. It finished 2020 at an all-time low of just 0.10 per cent. In January last year, the average term deposit rate was 1.05 per cent: by December it had slumped to merely 0.35 per cent. Along similar lines, the yield on a 3-year Aussie government bond fell from 0.90 per cent to a record low of 0.10 per cent over 2020, where it is set to remain for years if the Reserve Bank of Australia’s explicit forward guidance proves accurate.

Australian savers have never had to confront TD rates below 0.5 per cent, or at-call rates and 3-year government bond yields sitting near the zero per cent lower-bound. For many this will undermine the value of deposits and government bonds as an asset-class, forcing them to look for superior yields elsewhere. We have already observed the inception of this process, which is compressing spreads on high-yielding assets.

At the start of 2020, 5-year major bank senior bond spreads were at 0.71 per cent (or 71 basis points) above the quarterly bank bill swap rate. As a result of the search for yield and the arrival of the RBA’s $200 billion Term Funding Facility, which has obviated the need for banks to issue senior bonds, these spreads have contracted to just 0.31 per cent above bank bills. This is well inside the post-GFC “tights” at around 0.60 per cent.

We don’t see much upside left in senior bank paper, and have taken profits on about $2.3 billion of holdings that we added to materially during the March shock when 5-year major bank senior spreads blew as wide as 1.7 per cent (170 basis points) above bank bills.

In 2020, 5-year major bank Tier 2 bond spreads declined modestly from 1.75 per cent to 1.57 per cent above the quarterly bank bill swap rate on a point-to-point basis. This was of course punctuated by a record blow-out in Tier 2 credit spreads to around 4.0 per cent (or 400 basis points) above bank bills in March.

The post-GFC tights for Tier 2 spreads are 1.35 per cent, and, subject to the prevailing supply-side technicals, we think that major bank paper could test this level before too long. This week we have seen strong demand for longer-term major bank Tier 2 paper in US dollars that makes the Aussie dollar levels look cheap.

It’s noteworthy that in the pre-GFC period, major bank Tier 2 traded at circa 0.35 per cent (35 basis points) above bank bills. For a range of reasons, these spreads could continue to compress subject to the fact that the banks have to issue a lot of Tier 2 paper to meet certain regulatory requirements.

Perhaps the best value in the banks’ capital structure is in the hybrid space where 5-year major bank spreads are still wide of where they were at the start of 2020. In January last year, 5-year major bank hybrid spreads were sitting at 2.81 per cent (281 basis points) above the bank bill swap rate. Today they are at about 2.98 per cent. Yes, they blew-out to around 8.4 per cent (840 basis points) above bank bills in March (we picked up over $300 million in that month alone). But the post-GFC “tights” are much lower at 2.35 per cent above bank bills with pre-GFC levels sitting lower again at 1.25 per cent.

It is important to caveat that there are key contractual differences between Tier 2 bonds and hybrids today compared to the securities that were issued before the GFC, which imply that they should trade on wider spreads. The counter-argument is that bank balance-sheet leverage has fallen dramatically since 2007, which, coupled with the post-GFC emergence of government guarantees of bank liquidity and much greater regulatory risk-aversion, means default risks on these securities have fallen, suggesting their spreads should be tighter.

Another way to think about Tier 2 and hybrid valuations is through the multiple of their spreads over equivalent-tenor senior paper that sits higher up the capital structure, which is a heuristic commonly employed by institutional investors. Since the application of the Basel 3 banking rules in January 2013, 5-year major bank Tier 2 bonds have typically traded on a spread that is 2.15 times 5-year major bank senior bond spreads. Today that Tier 2/senior multiple has expanded to an unprecedented 5.04 times. Five-year major bank hybrid spreads have historically traded at about 4 times 5-year major bank senior bond spreads. That multiple has likewise jumped to a never-before-seen 9.56 times. Both these measures indicate that there is remaining upside.

One key to the Aussie economy will be the housing market’s performance. Understanding housing—and accurately predicting its trajectory—is immensely important if one wants to have any hope of divining wider economic, and hence financial market, outcomes. Beyond being the single most valuable household asset, housing is also the banking system's largest exposure. My experience has been that those who get the housing market wrong tend to also misfire when it comes to hitting other macro targets and portfolio construction more generally.

Click on this link to read my full AFR column.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

........

Investment Disclaimer

Past performance does not assure future returns. All investments carry risks, including that the value of investments may vary, future returns may differ from past returns, and that your capital is not guaranteed. This information has been prepared by Coolabah Capital Investments Pty Ltd (ACN 153 327 872). It is general information only and is not intended to provide you with financial advice. You should not rely on any information herein in making any investment decisions. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The Product Disclosure Statement (PDS) for the funds should be considered before deciding whether to acquire or hold units in it. A PDS for these products can be obtained by visiting www.coolabahcapital.com. Neither Coolabah Capital Investments Pty Ltd, EQT Responsible Entity Services Ltd (ACN 101 103 011), Equity Trustees Ltd (ACN 004 031 298) nor their respective shareholders, directors and associated businesses assume any liability to investors in connection with any investment in the funds, or guarantees the performance of any obligations to investors, the performance of the funds or any particular rate of return. The repayment of capital is not guaranteed. Investments in the funds are not deposits or liabilities of any of the above-mentioned parties, nor of any Authorised Deposit-taking Institution. The funds are subject to investment risks, which could include delays in repayment and/or loss of income and capital invested. Past performance is not an indicator of nor assures any future returns or risks. Coolabah Capital Institutional Investments Pty Ltd holds Australian Financial Services Licence No. 482238 and is an authorised representative #001277030 of EQT Responsible Entity Services Ltd that holds Australian Financial Services Licence No. 223271. Equity Trustees Ltd that holds Australian Financial Services Licence No. 240975.

Forward-Looking Disclaimer

This presentation contains some forward-looking information. These statements are not guarantees of future performance and undue reliance should not be placed on them. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such forward-looking statements. Although forward-looking statements contained in this presentation are based upon what Coolabah Capital Investments Pty Ltd believes are reasonable assumptions, there can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Coolabah Capital Investments Pty Ltd undertakes no obligation to update forward-looking statements if circumstances or management’s estimates or opinions should change except as required by applicable securities laws. The reader is cautioned not to place undue reliance on forward-looking statements.

2 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment